Anatomy of Korea's +241% Stock Market Rally

IN-DEPTH ANALYSISSTOCKKOREA

5/14/202621 min read

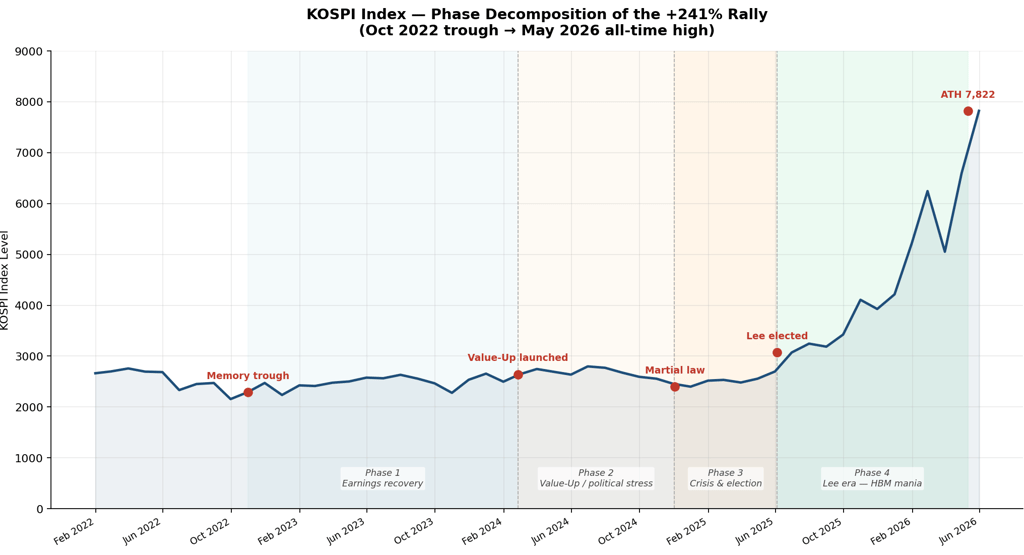

The Korean equity market breached the record high KRW 7,822 for the Korean index KOSPI. This represents a +241% price move from the 2,294 trough in October 2022. The combined KOSPI and KOSDAQ market capitalisation has surpassed KRW 7,000 trillion (USD 4.75 trillion) for the first time.

The KOSPI is Korea’s flagship equity benchmark made up of 800-900 large and mid-cap securities on the Korea Stock Exchange (KRX) with a total market capitalisation of approximately KRW 6,400 trillion. The market is mostly dominated by technology and semiconductor stocks where Samsung Electronics various shares listings and SK Hynix historically have represented 35-50% of the index. The remaining composition includes Hyundai Motor and other auto supply chain companies, LG Energy Solution and chemicals, varied financials, shipbuilding, defense, power equipment and some biopharma names. The smaller, KOSDAQ, market is a tech and venture oriented index of 1,800 smaller cap companies perceived to be growth or speculative in nature and represented mostly by IT, biotech, pharmaceuticals and entertainment.

Samsung Electronics and SK Hynix have both reached all-time highs, with SK Hynix returning over 2,200% from trough to peak as seen with its price moving from ca. KRW 80,000 in the depths of the 2022 memory downcycle to KRW 1.88 million.

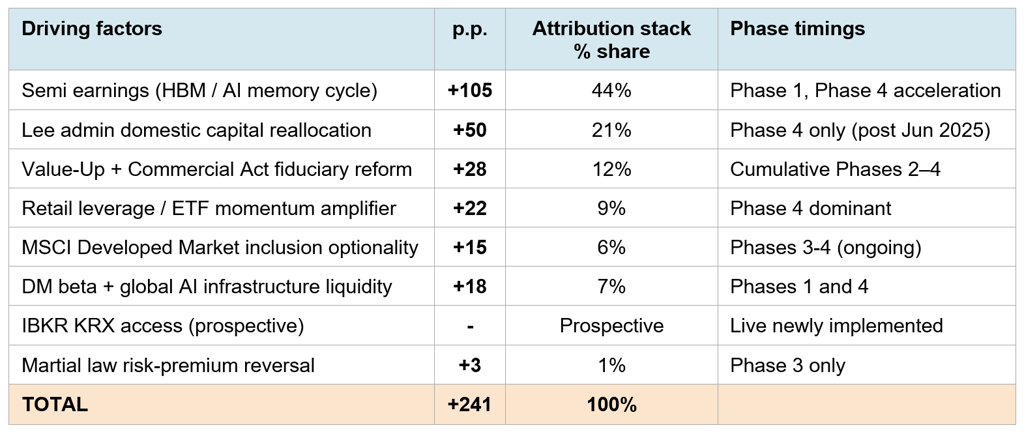

This article tries to break down the KOSPI aggregate price action into eight structural and cyclical drivers. The thesis is that the move is neither pure fundamentals nor pure Korea FOMO. It is an orchestra of different instruments playing conveniently at the same time: a genuine earnings supercycle (HBM), a structural domestic capital reallocation from Lee Jae-myung government policy stack, a governance re-rating (Value-Up plus Commercial Act), new index inclusion optionality (MSCI Developed Markets) and a set of liquidity and market access expansions.

Context as introduction, price-to-earnings (PE) multiples have not expanded during this rally. The KOSPI 12-month forward P/E currently stands at approximately 7.3x, below the COVID-19 pandemic low of 7.5x, and well below Asia Pacific peers at 15.4x. This confirms the move is overwhelmingly earnings-driven and fundamentally justified to a far greater degree than mere multiple-expansion. More importantly, the rally has greater structural durability than a unilateral multiple-expansion story would show.

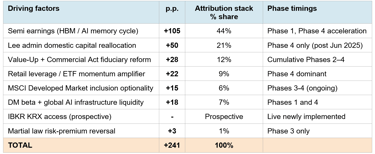

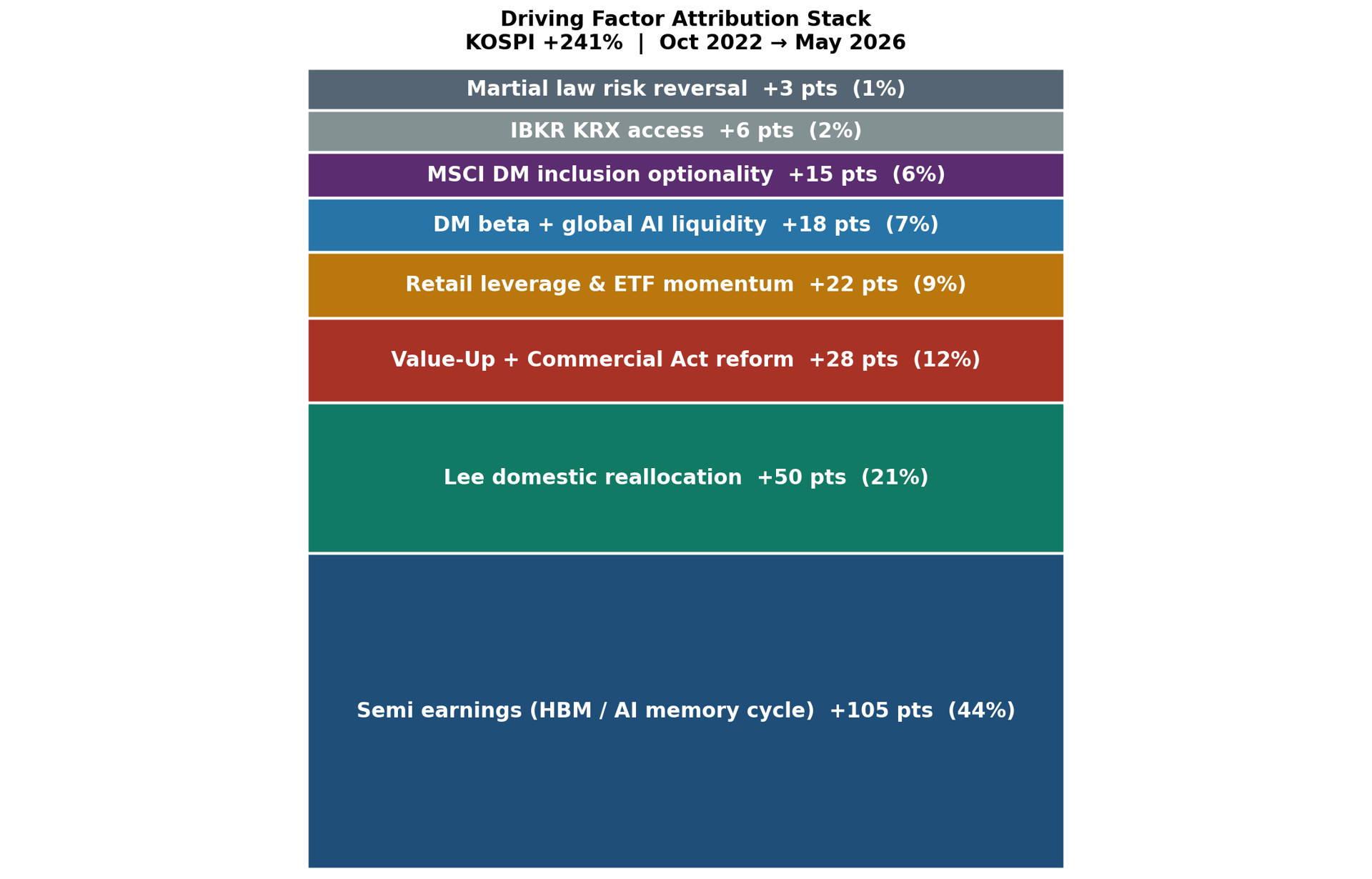

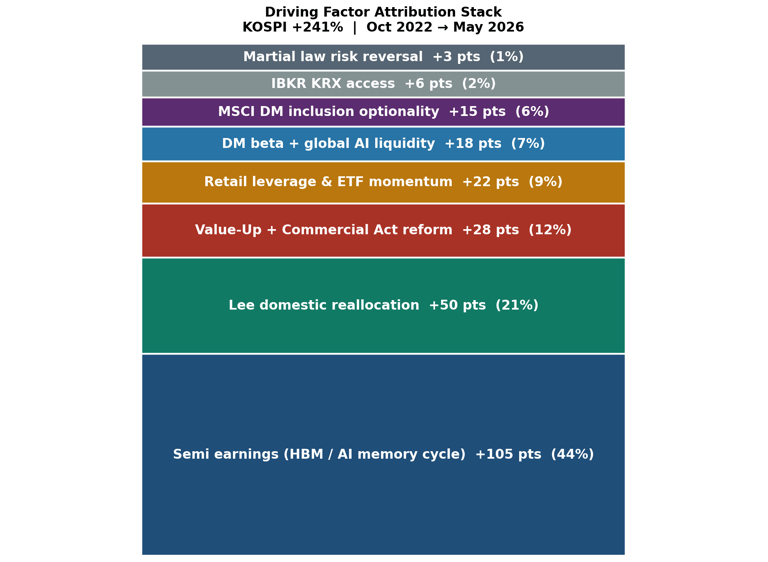

Headline attribution: semiconductor earnings explain ~44% of the +241 pts; Lee administration resulting in a Korean capital reallocation to domestic equities ~21%; Value-Up plus Commercial Act governance reform ~12%; retail investors use of leverage through margin and single-name 2x levered ETFs ~9%; MSCI Developed Market inclusion optionality ~6%; Developed markets beta and global AI infrastructure liquidity ~7%; Interactive Brokers (IBKR) Korea stock market (KRX) access: negligible to date but incoming; and previous martial law risk-premium reversal ~1%.

This remains the single largest driver and the one most defensible on first principles. Samsung Electronics and SK Hynix together represent roughly 50% of KOSPI market capitalisation, with that weight having grown materially as both names dramatically outperformed the index. JPMorgan estimates that memory stocks drove approximately 70% of KOSPI gains in 2025, and those two names alone account for roughly three-fifths of YTD 2026 gains.

The product driving these earnings is High Bandwidth Memory (HBM), a specialised chip that sits directly on top of AI accelerators made by Nvidia, AMD and the major cloud providers. The HBM variants relevant here, HBM3 and HBM3E, sell for five to eight times the price of standard DRAM and are sold under multi-year supply contracts rather than on the spot market.

The multiple compression finding and its implications

SK Hynix was first to volume production of HBM3E and has held that lead. Korea's chip exports surged 139% year-on-year in Q1 2026, and the first ten days of May 2026 alone saw USD 8.54 billion in chip shipments; a monthly record run-rate. Goldman Sachs has revised Korea's 2026 EPS forecast upward three times this year, reaching +130% for MSCI Korea, the strongest in Asia outside the 1999 post-crisis recovery.

Interested in in-depth analysis of the semiconductor industry? Check out our extended research on the innerworkings of the semiconductor world: its history, technology and key players in this market, here.

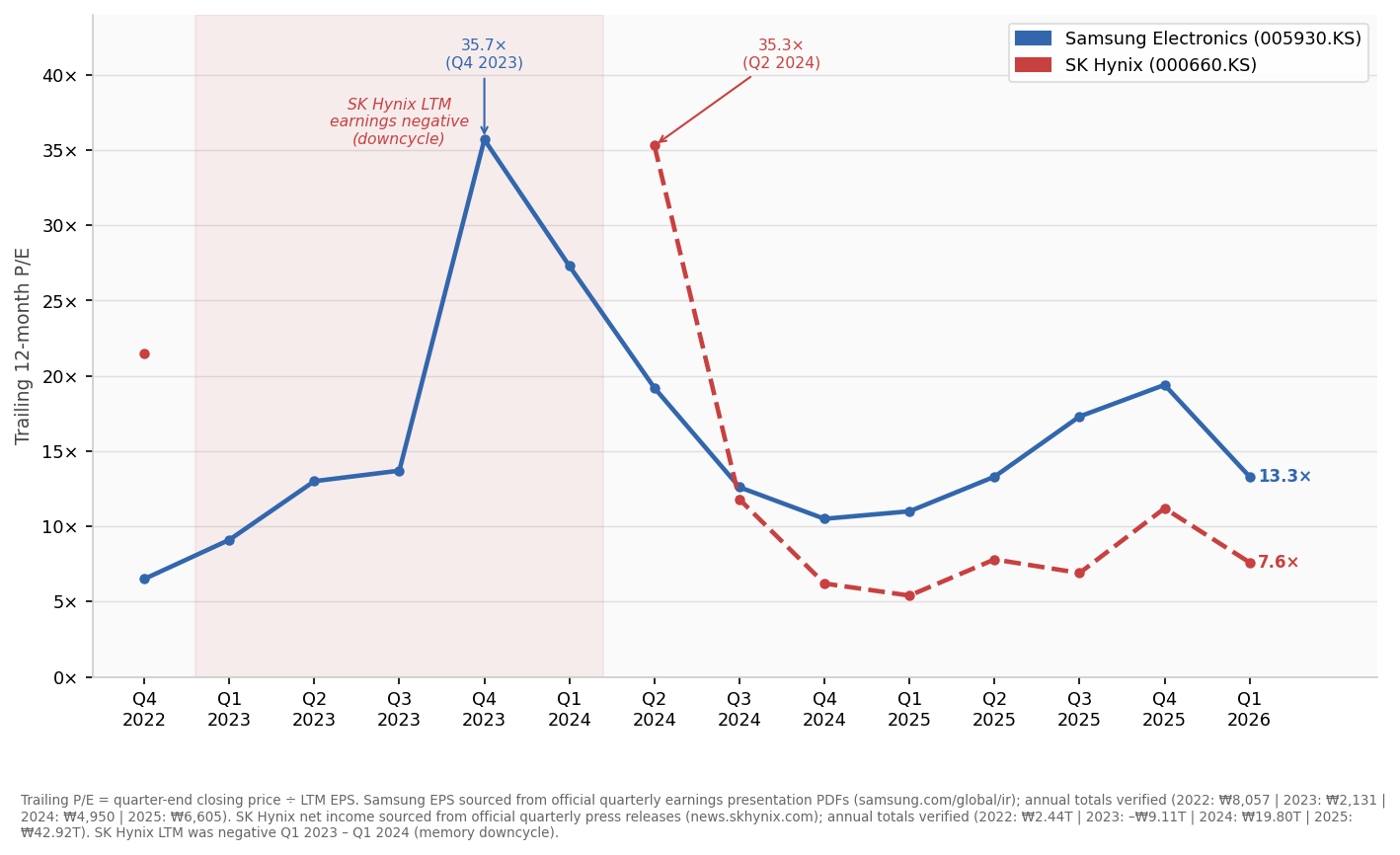

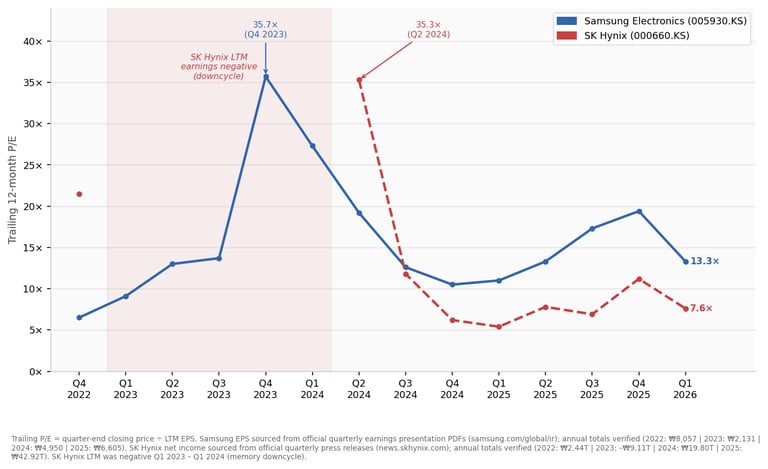

Despite the KOSPI at all-time highs, Korean equities are cheaper on a trailing earnings basis than at any point in recent memory — and the chart makes the mechanism clear. Samsung's trailing P/E peaked at 35.7× in Q4 2023 as prices recovered ahead of the earnings cycle, then compressed to 10.5× by Q4 2024 as profits followed; a subsequent price surge has nudged it back to 13.3× as of Q1 2026. SK Hynix's LTM earnings were negative throughout the 2023 downcycle; once the HBM revenue inflection hit, the trailing multiple collapsed from 35.3× in Q2 2024 to 6.2× by year-end, and stood at 7.6× in Q1 2026.

On a forward basis the discount is starker: MSCI Korea trades at approximately 7× forward earnings against MSCI Asia Pacific's 15.4×, despite projecting materially stronger EPS growth. Goldman Sachs has raised its 2026 MSCI Korea EPS growth forecast to +130%, reaching the third upward revision this year, meaning the forward multiple is compressing because earnings estimates are rising faster than prices. The sustainability question is therefore not whether multiples will deflate, but whether the earnings trajectory holds.

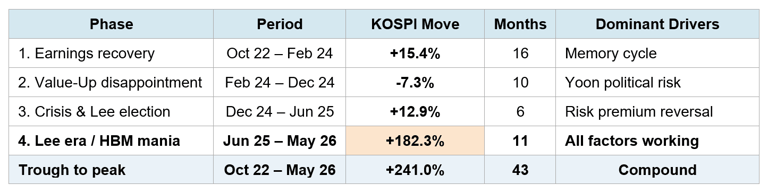

Four key phases are identifiable with respective drivers. Roughly 80% of the aggregate +241% was generated in the eleven months since Lee Jae-myung's June 2025 election, when all eight factors were operating simultaneously.

Phases of the rally

Phase 4 alone produced +182 percentage points in 11 months. It is accompanied by earnings growth that exceeds price appreciation, pushing against claims of mere speculative mania.

The decomposition below allocates the +241 percentage points of KOSPI return to 8 driving factors. Data shows P/E multiples have compressed, not expanded, through the rally. The price move is entirely justified by earnings growth and capital flow reallocation, making it structurally more defensible than a multiple-expansion narrative would suggest.

Aggregate driving factor attribution

Driver 1: Semiconductor earnings and the HBM supercycle

Driver 2: Lee administration domestic capital reallocation

The Lee administration's policy stack operates through four distinct but interconnected channels, all pointing domestic capital toward equities. These are real estate disincentives, inheritance tax asymmetry, dividend income tax cut and active repatriation from US equities.

Capital Gains Tax Surcharge on Multiple-Home Owners (다주택자 양도소득세 중과세) 소득세법 제104조 제1항 제4호 및 제7호

The surcharge adds 20 percentage points above the standard capital gains rate for owners of two homes selling within a designated speculation zone, and 30 percentage points for owners of three or more homes. The Yoon administration suspended it annually from May 2022. The Lee administration allowed the suspension to expire on 9 May 2026, reinstating it in full. The National Tax Service statutory rate table confirms the surcharge structure and its suspension window of 10 May 2022 to 9 May 2026.

Korean household wealth in residential real estate exceeds 75% of net worth. Reinstatement of a 20–30 percentage point penalty on sale directly raises the cost of holding multiple properties and shifts the after-tax return comparison between property and listed equities. Even marginal reallocation from this base is large relative to KRX float.

Source: National Tax Service

Inheritance Acquisition Tax System Reform (유산취득세 전환) 기획재정부 세법 개편안 2025년 3월

The Ministry of Economy and Finance announced in March 2025 the first overhaul of Korea's inheritance tax in 75 years, shifting the tax base from the total estate of the deceased to each individual inheritor's share. The top rate of 50% is retained but the basic deduction per child rises from 50 million won to 500 million won, and spousal inheritances up to 1 billion won become fully exempt. The reform takes effect in 2028 and is projected to reduce annual inheritance tax revenue by approximately 2 trillion won. The Ministry published the full legislative plan on its official press release page.

The reform reduces the tax friction on transferring listed financial assets between generations while the multi-home surcharge simultaneously increases the cost of holding property into an estate. For high-net-worth families approaching succession events, the relative attractiveness of holding wealth in listed securities has improved on both sides of the ledger.

Source: Ministry of Economy and Finance (announcement);

primary legislative text lodged at https://www.moef.go.kr

High-Dividend Stock Separate Taxation (고배당주식 배당소득 분리과세) 조세특례제한법 개정안, 2025년 12월 2일 국회 통과

The National Assembly passed this amendment on 2 December 2025. Under the previous system, financial income exceeding 20 million won per year was aggregated with all other income for comprehensive taxation at up to 49.5%.

The new law creates a fully separate taxation track for dividends received from listed companies with a payout ratio of at least 40%, or at least 25% if dividends grew by 10% or more year on year. The separate rates are: 14% on amounts up to 20 million won, 20% on 20 million to 300 million won, 25% on 300 million won to 5 billion won, and 30% above 5 billion won. The maximum effective rate on dividend income therefore falls from 49.5% to 30%.

The threshold structure creates a simultaneous incentive on both sides: companies are pushed to raise payout ratios to qualify, and investors receive a materially better after-tax yield once they do. Running equity yields improve for the entire domestic investor base, not just the high-net-worth segment.

Source: Ministry of Economy and Finance 2025 Tax Reform Proposals

Domestic Capital Market Revitalisation and FX Stability Tax Support Package (국내투자·외환안정 세제지원 방안) 기획재정부 보도자료, 2025년 12월 23일

The Ministry of Economy and Finance published this package on 23 December 2025. It provides specific tax incentives for retail investors who sell overseas equity positions and reinvest in KRX-listed securities, and simultaneously lifts the dividend tax exemption on inbound dividends from overseas subsidiaries of Korean corporates to 100% from 95%.

The policy was issued jointly with the Bank of Korea as part of a coordinated response to acute won depreciation pressure. At the time of publication, Korean retail investors held $161.1 billion in foreign-listed stocks, a share that had grown from under 10% of Korea's overseas equity investment before 2020 to over 30% by late 2024.

The package targets two repatriation channels at once: retail investors rotating out of foreign names and Korean corporates bringing overseas earnings home. Both flows add incremental demand to KRX-listed securities beyond new equity converts from property or deposits.

Lastly, for context, the structural argument is that Korean households remain at world-low levels of financial asset holdings relative to GDP, meaning the reallocation runway is very long even if near-term momentum normalises. The "money move" is a named and tracked trend or phenomenon in recent Korean financial media which aims to describe this shift from bank deposits and real estate into domestic equities.

Source: Ministry of Economy and Finance

Driver 4: Retail participation and leverage amplification

Corporate Value-Up Programme (기업 밸류업 프로그램) Financial Services Commission, launched 26 February 2024

The FSC launched this programme at its first policy seminar on 26 February 2024, modelled explicitly on the Tokyo Stock Exchange's 2023 governance initiative. The programme requires listed companies to assess their valuation against P/B and P/E benchmarks, identify the causes of any undervaluation and disclose medium- to long-term plans to address it; including targets for return on equity, dividend policy and capital structure. For companies with total assets exceeding 500 billion won, confirmation of whether a Value-Up plan has been prepared must appear in their mandatory corporate governance report. A dedicated Value-Up Index was launched by the Korea Exchange in September 2024, tracking companies that meet five criteria: top-400 market capitalisation, no losses over two prior years, consistent dividend or buyback history, P/B in the top 50% of peers and above-average ROE. ETF AUM tracking the index exceeded 1 trillion won within months of launch.

The market reaction in 2024 was tepid and correctly so: the programme was disclosure-based and entirely voluntary, with no tax incentives attached at launch and no legal liability for non-compliance. For the non-semiconductor half of the KOSPI, where earnings growth has been far slower than the HBM names, the programme alone was insufficient to drive re-rating. It established the framework and the vocabulary, but enforcement was the missing element.

Source: Financial Services Commission

Commercial Act Amendment — Directors' Fiduciary Duty to All Shareholders (상법 제382조의3 개정) 상법 개정안, National Assembly passed 3 July 2025, promulgated 22 July 2025

The amendment revised Article 382-3 of the Commercial Code, clarifying that directors owe a duty of loyalty not only to the company but also to its shareholders. It was passed once before in March 2025 but vetoed by then-acting President Han Duck-soo, before being reintroduced and enacted in July 2025. Directors are now explicitly required to act in the best interests of all shareholders and to treat all shareholders fairly and equally.

The fiduciary duty provisions took effect immediately upon promulgation on 22 July 2025. The same amendment also extended the aggregate 3% voting cap on controlling shareholders and their affiliates to all audit committee appointments including independent directors, renamed "outside directors" to "independent directors" and increased the minimum independent director requirement from one-quarter to one-third of the board in listed companies. A second amendment passed on 25 August 2025 added mandatory cumulative voting for large listed companies with assets above 2 trillion won and increased the minimum number of separately elected audit committee seats.

This is the upgrade that converts the Value-Up programme from a soft disclosure exercise into one with legal liability behind it. Before the amendment, a director who favoured the founding family over minority shareholders in a merger, spin-off or capital transaction had no clearly established fiduciary breach to minority shareholders under Korean law. After it, minority shareholders can bring civil claims directly against directors. The chaebol cross-holding and treasury share structures that have depressed P/B ratios for decades now carry governance and litigation risk they previously did not. For the non-semiconductor portion of the KOSPI the governance re-rating is the primary explanation for price appreciation where earnings growth alone cannot account for it.

Source: Legal500 client alert Primary legislative text: National Assembly of Korea.

KOSPI 5000 Special Committee (코스피 5000 특별위원회) Formed June 2025, immediately upon President Lee taking office

The committee was established by the Lee administration within weeks of inauguration to coordinate and accelerate corporate governance and capital market reform across ministries and regulators. It sits above the FSC, the Ministry of Economy and Finance and the Korea Exchange and is tasked with tracking implementation of Value-Up disclosures, the Commercial Act amendments and dividend tax reform simultaneously. It gives the reform programme a cross-government coordination function that the FSC alone did not have.

The committee signals political commitment at the presidential level, not merely regulatory enthusiasm. For foreign institutional investors who have historically discounted Korean governance reform efforts as cyclical and reversible, the formation of a dedicated body with presidential backing changes the credibility calculus.

Source: Matthews Asia

Korean equity markets are structurally retail-heavy. Individual investors have historically accounted for 50–70% of KOSPI and KOSDAQ trading volume, a concentration that has no close equivalent among major developed markets. In Phase 4 this baseline has been amplified by two reinforcing developments: the introduction of single-stock leveraged ETFs on Samsung and SK Hynix, and a record build in margin debt balances at Korean securities firms.

Single-Stock 2x Leveraged ETF Authorisation (단일종목 레버리지 ETF 허용) 금융감독원 금융투자업규정 시행세칙 개정, Financial Supervisory Service, April 2026

To understand what this policy changed it is necessary to understand what existed before it. Korea already permitted leveraged ETFs tracking broad indices, products such as KODEX KOSDAQ150 Leverage attracted net inflows of 1.79 trillion won in early 2026 alone, but regulations requiring each ETF to hold a minimum of ten stocks with no single holding above 30% made single-stock leverage vehicles impossible to list domestically. Retail investors who wanted 2x exposure to Samsung or SK Hynix individually had to buy Hong Kong-listed products, accept foreign-exchange losses on won movements and trade across time zones. The FSS pre-announced a proposed revision to the Enforcement Rules of the Financial Investment Business Regulations in April 2026, formally authorising single-stock leveraged and inverse ETFs for the first time. Regulators expanded the lineup beyond 2x products to include inverse 2x ETFs as well, given that these were entirely new product types in the domestic market. Coverage was restricted to Samsung Electronics and SK Hynix as the only eligible underlying stocks, subject to admission criteria requiring the underlying to represent over 10% of market capitalisation and over 5% of trading volume. Eight Korean asset managers launched sixteen products on 22 May 2026, with some firms targeting management fees as low as 2 basis points.

The demand context matters. The CSOP SK Hynix Daily 2x Leveraged ETF, listed in Hong Kong in October 2025, had already surpassed HK$40 billion in AUM by 8 May 2026, overtaking the Direxion Daily TSLA Bull 2X ETF to become the world's largest single-stock leveraged ETF. From listing through April 2026, SK Hynix's underlying stock rose 208%, which would theoretically imply a 416% gain for a clean 2x product; the ETF actually returned 513%. Domestic listing brings that return profile inside the KRX at 15.4% capital gains tax rather than the 22% rate on overseas ETF gains, and without the currency drag. The product launch did not create the retail appetite, it channelled an appetite that already existed and was already distorting price action in the underlying names via indirect routes.

Source: FSS enforcement rules revision announcement

Margin Debt (신용잔고) and the Reflexive Feedback Loop

Margin trading in Korean equities operates through securities firms extending credit against existing portfolio collateral. When stock prices rise, the collateral value of existing holdings increases, which mechanically raises the amount a retail investor can borrow to buy more stock. That additional buying supports further price appreciation, which again raises collateral values. This is the reflexive feedback loop: rising prices enable leverage, leverage funds purchases, purchases support prices. Retail investors had accumulated 32 trillion won in margin debt at the point when geopolitical shocks in early March 2026 triggered a sharp reversal, prompting major Korean securities firms including Korea Investment and NH Investment to suspend new margin purchases entirely as credit limits were exhausted. The suspension itself became a second-order shock: forced liquidations began as collateral values fell below minimum ratios, accelerating the decline.

The buy-side expression of the same dynamic is visible in the May 11 session. On 11 May 2026, the KOSPI surged 324 points or 4.32% to close at 7,822. A buy-side sidecar was triggered at 9:29 a.m., the eighth such trigger in 2026 alone. On the KOSPI that day, retail and institutional investors were net buyers of 2.87 trillion won and 623.9 billion won respectively, while foreign investors were net sellers of 3.51 trillion won. The sidecar, to define it plainly, is a five-minute suspension of programme trading triggered when KOSPI 200 futures move 5% or more in a single minute. It does not halt manual trading in individual stocks. Its activation on the buy side, something that occurs only in acute upward momentum conditions, alongside net foreign selling of 3.51 trillion won confirms the character of the session: domestic retail and leveraged flow pushed the index through a historic threshold against the direction of the largest and most informed participants. That 735 stocks declined and only 147 advanced on the same day makes the index concentration explicit; two names with the largest retail leverage overhang carried the benchmark while the rest of the market went the other way.

Source: Seoul Economic Daily, margin suspension.

Special case insight: the stocks retail Korea most wants to own are becoming unreachable for them

There is a structural irony running through the retail participation story. SK Hynix trades at KRW 1.88 million per share (~USD 1,280) and Samsung Electronics at KRW 285,500 (~USD 195). These are not split-adjusted oddities, Korean listed companies have historically been slow to conduct stock splits, and the high nominal price per share has simply compounded as the AI rally has run. For a 20-year-old opening a Toss or KakaoPaySecurities account with KRW 100,000 to invest, a single share of SK Hynix costs nineteen months of that budget.

Fractional share trading (소수점 매매) for domestic Korean stocks technically exists; it was introduced in September 2022 when Kiwoom, Mirae Asset, NH, and KB joined a KRX-coordinated scheme, with Samsung Securities and Shinhan following in October. But the implementation carries three structural penalties that make it materially inferior to whole-share trading. Settlement is end-of-day only, at closing price, with a maximum of one order per day; real-time fractional execution is unavailable. Commission rates are ten times higher: domestic whole-share trading charges 0.01–0.015%, while fractional domestic trading costs 0.15% at most brokers, a penalty the industry acknowledges openly as necessary because whole-share commissions are already priced at near-loss levels. And critically, Toss Securities. the fastest-growing platform among the under-35 demographic, does not offer domestic stock fractional trading at all, only foreign stock fractional trading. The broker most beloved by the retail investors most affected by the share price barrier is precisely the one that has not solved the problem.

The practical workarounds are well-understood by the community. The dominant solution is ETFs: any KOSPI200, semiconductor, or AI-themed ETF effectively delivers Samsung and SK Hynix exposure at low unit cost. One Korean financial analysis put it plainly: buying a semiconductor ETF means money flows to those two names regardless of whether the investor touches the underlying stock. Some leveraged semiconductor ETFs allocate 40%-plus of weight to SK Hynix alone. The secondary workaround is SK Square (SK스퀘어), a listed holding company with a major SK Hynix stake that trades at a meaningful NAV discount and at a fraction of the underlying share price — a proxy route used by both Korean domestic investors and, notably, by the first wave of US IBKR buyers on May 4, 2026, who targeted SK Square specifically as the cheaper access vehicle.

A potential resolution is coming from an unexpected direction. SK Hynix is reported to be pursuing a US ADR (American Depositary Receipt) listing within 2026. If completed, this would make SK Hynix accessible through any US brokerage platform with full real-time fractional trading at US commission rates — solving the accessibility problem from the outside in, and simultaneously deepening the foreign retail demand channel that IBKR has just opened. The Korea stock market's most extraordinary beneficiary of the AI cycle may ultimately become more accessible to a retail investor in America than to one in Korea.

Korea's contribution to the global AI supply chain means its equity market no longer trades simply as an emerging market beta. It trades as a hybrid: EM index weight with developed-market technology sensitivity. The structural buyer of HBM (Nvidia, AMD, Google, Amazon and Microsoft) is simultaneously the primary driver of Nasdaq performance. When AI infrastructure capital expenditure accelerates, it lifts Nasdaq and directly confirms the earnings thesis for Samsung and SK Hynix in the same motion. The result is a double impulse: the global risk-on environment raises all beta assets, and the specific AI capex read-through is applicable to Korean earnings rather than merely sentiment.

In Phase 4, successive S&P 500 and Nasdaq all-time highs provided the macro backdrop that amplified Korea-specific drivers. The March 4 session illustrated the same mechanism in reverse. The KOSPI fell 12% in a single day, its largest ever single-session decline, after AI-bubble concerns briefly compressed the global technology trade. The 10% single-day recovery that followed, the strongest since 2008, was equally reflexive. The beta works symmetrically and the speed of both moves reflects how much of the Korean market's Phase 4 appreciation was financed by leveraged positions benchmarked to global technology sentiment rather than held as conviction long-term equity.

Korea's energy import dependence is the principal modifier of this beta relationship. As a large crude oil importer, Brent above USD 100 per barrel represents a direct margin headwind for Korean corporates and a secondary drag on consumer spending through higher domestic fuel costs. The US-Iran tensions driving current oil prices therefore simultaneously pressure Korean earnings at the company level and introduce macro volatility at the index level, partially offsetting the positive AI liquidity impulse and contributing to the intraday amplitude of Phase 4 price action even within the structural bull market.

To understand why this matters, some mechanical context is necessary. The world's largest passive funds, those tracking MSCI Emerging Markets and MSCI World, are required to hold exactly what their benchmark holds, in proportion. When a country moves from one index to another, those funds are forced to buy or sell regardless of valuation. Korea has been classified as an Emerging Market by MSCI since 1992 despite being Asia's fourth-largest economy and among the most liquid markets in the world. FTSE Russell, S&P and Dow Jones already classify it as developed. The MSCI anomaly is the one that matters for passive flows because of the size of the funds benchmarked to it.

MSCI declined in its 2025 annual review to add Korea to its watchlist for potential reclassification. The specific barriers cited were limited convertibility of the won in the offshore currency market, restrictions on omnibus accounts and OTC trading, and incomplete adoption by listed companies of the pre-record-date dividend confirmation system Korea had introduced in line with global norms. MSCI stated it would continue to monitor the implementation and market adoption of measures to enhance accessibility, specifically to determine whether these measures have replicated the outcomes of fully operational offshore FX markets found in Developed Markets. The mechanics of the timeline are fixed: a market must spend a minimum of one year on the watchlist before formal reclassification can occur, and the watchlist is updated only at the June annual review. Missing the June 2025 review means the earliest possible watchlist addition is June 2026, formal reclassification June 2027 at the earliest, and passive inflow materialisation in 2028.

Korea MSCI DM Inclusion Roadmap (MSCI 선진국 지수 편입 로드맵) Ministry of Economy and Finance / FSC task force, announced January 2026

The Korean government published a comprehensive roadmap in January 2026 targeting watchlist addition at the June 2026 annual review, with a formal reclassification decision possible in June 2027 and passive inflows materialising in 2028. The centrepiece accessibility measure is extension of foreign exchange market operations to 24 hours starting in July, directly addressing MSCI's primary objection about offshore won convertibility. The government simultaneously established a task force comprising the Bank of Korea, FSC, FSS and Korea Exchange alongside private-sector participants to coordinate implementation across the outstanding MSCI requirements.

The equity market is pre-pricing some probability of this outcome. Unlike the other four drivers, MSCI reclassification is a binary event with a discrete and very large flow consequence: Goldman Sachs projects USD 30 billion in passive inflows upon inclusion and the Korea Economic Research Institute estimates as much as USD 45 billion. Markets do not wait for the event to occur; they discount the probability-weighted present value of expected inflows in advance. The June 2026 review is the next decision point. If Korea is added to the watchlist, the inflow probability shifts from speculative to high-confidence and the re-rating could accelerate materially. If it is missed again, the optionality premium currently embedded in prices will partially unwind.

Source: MSCI 2025 Market Classification Review, Korea MSCI roadmap announcement.

Driver 5: MSCI Developed Market inclusion optionality

Driver 6: DM beta and global AI infrastructure liquidity

Driver 7: Interactive Brokers KRX access

The December 2024 martial law declaration by Yoon Suk-yeol and the subsequent impeachment created an acute political risk premium that compressed Korean equity valuations relative to Asian peers and contributed directly to Phase 2 underperformance. This was not a structural deterioration in Korean fundamentals, but a discrete governance shock that artificially widened the gap between intrinsic value and market price. Lee's orderly election in June 2025 and the immediate policy continuity signals that followed resolved the overhang cleanly and rapidly.

The reversal of this discount coincided with, and was reinforced by, the announcement of the National Growth Fund; a KRW 100 trillion vehicle financed through public-private structures with the National Pension Service as cornerstone investor, targeting AI, semiconductors and advanced manufacturing. The two elements belong together because they operate on the same underlying variable: the credibility of Korea as a stable, long-duration destination for capital. The martial law episode temporarily destroyed that credibility; the election restored it; and the National Growth Fund, by committing the NPS to a structural increase in domestic equity allocation, converts the restored credibility into a durable demand signal. The NPS manages approximately USD 800 billion in assets with a historical bias toward international equities. Even a modest reallocation toward domestic strategic industries represents hundreds of trillions of won in incremental demand that does not depend on foreign sentiment, retail leverage or any of the other more volatile Phase 4 flows.

The contribution attributed to this driver is small in retrospective terms because the martial law compression was resolved quickly and the National Growth Fund has not yet deployed capital at scale. Its significance is prospective: it removes the tail risk of political instability from the Korean equity risk premium on a more durable basis than any prior administration has managed, and it creates an institutionally anchored domestic buyer that will accumulate through cycles rather than amplify them.

Source: Korea Herald, Lee administration market initiatives and National Growth Fund.

Driver 8: Martial law risk-premium reversal and National Growth Fund

Interactive Brokers enabled direct retail access to KRX-listed securities approximately one week ago, meaning this factor has had no time to affect prices and carries zero retrospective contribution to the +241% rally analysed here. It is included solely as a prospective catalyst.

The structural logic is directly analogous to Citrini Research's documented analysis of the Taiwan Stock Exchange access opening via IBKR, which contributed meaningfully to TSMC and the broader Taiwan market re-rating during its AI cycle: latent foreign demand that previously lacked execution infrastructure converts to actual flow once the friction is removed.

The forward potential is meaningful. Foreign flows into KOSPI were approximately KRW 16 trillion net negative through May 2025 and have been volatile since; net buying in H2 2025 as the Lee rally took hold, reverting to net profit-taking in YTD 2026. On today's record session, foreign investors were net sellers of KRW 366 billion against retail net buying of KRW 540 billion. The rally to date has been powered overwhelmingly by domestic investors. IBKR access creates a new marginal buyer pool that has not yet been a factor.

The Taiwan precedent suggests the effect compounds over 12 to 24 months rather than arriving as an immediate step-change: global retail investors and smaller institutions who had a thesis but lacked access begin accumulating gradually once the infrastructure is in place. Given that Korea now offers AI earnings growth, Value-Up governance reform and MSCI DM reclassification optionality as a combined investable thesis for foreign retail, the setup for IBKR-driven incremental demand is arguably stronger than Taiwan's was at an equivalent stage.

Forward outlook

The eight drivers do not all run at equal intensity going forward. Understanding their sequencing matters as much as their individual strength.

In the next twelve months the market sits at peak driver concentration. Semiconductor earnings, Lee policy and DM beta are firing simultaneously at or near maximum intensity. The reflexive layer of retail leverage and leveraged ETFs is at a level historically associated with sharp mean reversion. A 20 to 30% correction would be entirely consistent with the structural bull market remaining intact. The MSCI June 2026 review is the single most important near-term binary: watchlist inclusion front-runs USD 24 to 45 billion in passive inflows; a second consecutive exclusion removes a meaningful premium from current prices.

Over three years the durable drivers take over from the cyclical ones. Value-Up and the Commercial Act fiduciary amendment compound legally and cannot easily be reversed. Lee's domestic reallocation policy runs through approximately 2030 and the dividend tax cut is legislated permanently. IBKR-driven foreign demand builds from near zero as global retail investors discover a thesis combining AI earnings growth, governance reform and historically low valuations. The HBM earnings cycle extends through 2027 to 2028 on current consensus. The three-year structural floor for KOSPI is materially higher than pre-2025 levels regardless of how the reflexive layer normalises.

At five years, semiconductor earnings moderate as ASPs normalise and HBM matures. Lee policy approaches its natural political cycle limit. The structural floor is held by legally binding governance reform, MSCI reclassification either completed or approaching, IBKR-driven foreign accumulation and National Pension Service reallocation. These are slow and large forces. They do not depend on sentiment.

The overall conclusion is straightforward. The Korea discount, the persistent valuation gap relative to global peers that has defined this market for two decades, is in structural rather than cyclical retreat for the first time. The rally to date has been overwhelmingly earnings-driven and fundamentally justified. What comes next depends less on whether the structural case holds, and more on whether the reflexive amplification layer unwinds gradually or violently before the next leg of structural appreciation begins.

Driver 3: Value-Up programme and Commercial Act fiduciary reform

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.