The Payment Industry

A description of the innerworkings of the Payment Industry

IN-DEPTH ANALYSISPAYMENTINDUSTRY

Rafael CARRARA

4/30/202647 min read

1. Executive Summary

The global payments industry is the foundational plumbing of the modern economy — an invisible infrastructure processing tens of trillions of dollars annually.

We do not appreciate cash enough. It is an extraordinary innovation built over centuries. What makes physical cash so elegant is a property economists call a unified ledger: cash is its own proof of value. When a consumer hands a banknote to a merchant, the consumer is immediately and irrevocably debited, and the merchant is immediately and irrevocably credited. No bank is involved. No computer needs to check anything. No counterparty needs to be trusted. The cash itself is the record.

Cash only requires two things to be verified: that the note is not forged, and that the person giving it is not acting under coercion. That is a remarkably simple set of problems — which is why cash has persisted for thousands of years and why, even today, billions of people prefer it.

Without a physical object as the unified ledger, a whole new set of questions must be answered for every transaction:

• Does the buyer actually have the money to pay? (Cash makes this obvious; digital payments require a real-time check)

• Is the buyer authorized to access those funds? (Is this their account? Is their card stolen?)

• Will the funds actually arrive in the merchant's account? (Who guarantees settlement?)

• Is all the sensitive financial information being transmitted securely?

• Who bears the loss if something goes wrong?

As we can see payments as a whole are complex, more than we give it credit for. It's one of those technology layers we use multiple times a day and it just works, and we never give it a second thought. But behind each tap, swipe or digital flow is a myriad of technology providers, fiercely competitive companies, some of the world’s most powerful network effects and a whole lot of regulations and geographic diversity.

It is simultaneously one of the most resilient sectors in finance and one of the most actively disrupted. Understanding it as an investor requires grasping both its extraordinary structural advantages and the forces that are systematically eroding those advantages from multiple directions.

Source: Quartr

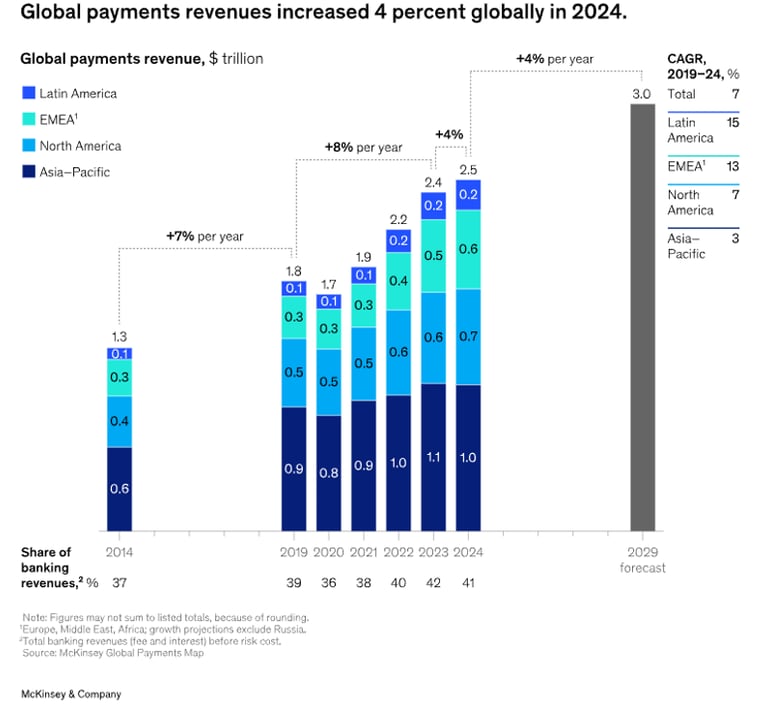

From 2019 to 2024, global payments revenue grew at an average rate of 7% per year. The sector delivered a mean return on equity of 18.9% in 2024, with some players exceeding 100% ROE — numbers that explain why payments has consistently attracted capital from Silicon Valley, private equity, and sovereign wealth funds alike. Yet the industry's growth slowed to 4% in 2024, as interest rates peaked and structural shifts toward lower-margin payment methods accelerated.

The core thesis for payments as an investment is the secular migration from cash to electronic transactions — a decades-long tailwind that is far from complete. In many emerging markets, cash still represents more than 50% of all transactions. As digital penetration rises, the total addressable volume for electronic payments expands, creating persistent revenue growth for the companies that own the rails, the technology, and the relationships.

However, the industry's complexity is often underestimated. The "payments industry" is not a monolith — it is a multi-layer ecosystem in which different players capture value at fundamentally different points of the chain. Visa and Mastercard own the network rails and earn highly predictable, asset-light toll fees. Issuing banks capture the largest share of every transaction via interchange. Acquirers and processors compete on a commoditized, high-volume, low-margin service. Payment Service Providers (PSPs) like Stripe and Adyen layer software and services on top of commodity processing to escape that compression. Each layer has a distinct risk/return profile for investors.

Key themes for 2025–2030 include: the rise of real-time account-to-account payments (A2A) threatening card interchange; the integration of stablecoins and tokenized money into mainstream rails; the emergence of agentic commerce as a new payment paradigm; AI-driven fraud prevention and routing optimization; and the ongoing geographic divergence between the card-dominant West and the super-app-driven Asia.

2. Market Size & Industry Structure

2.1 Global Revenue Overview

Payments is the most valuable subsector in all of financial services.

The headline figures underscore the industry's scale and resilience:

The 2024 deceleration was driven by three factors: (1) peaking interest rates reducing net interest income for issuing banks, which had represented 46% of total industry revenues in 2024; (2) a more muted macroeconomic environment dampening consumer spending growth; and (3) structural shifts toward lower-yield payment methods such as debit, real-time transfers, and digital wallets. Despite this, McKinsey's baseline forecast remains positive through 2029, anchored by the continuing global shift away from cash.

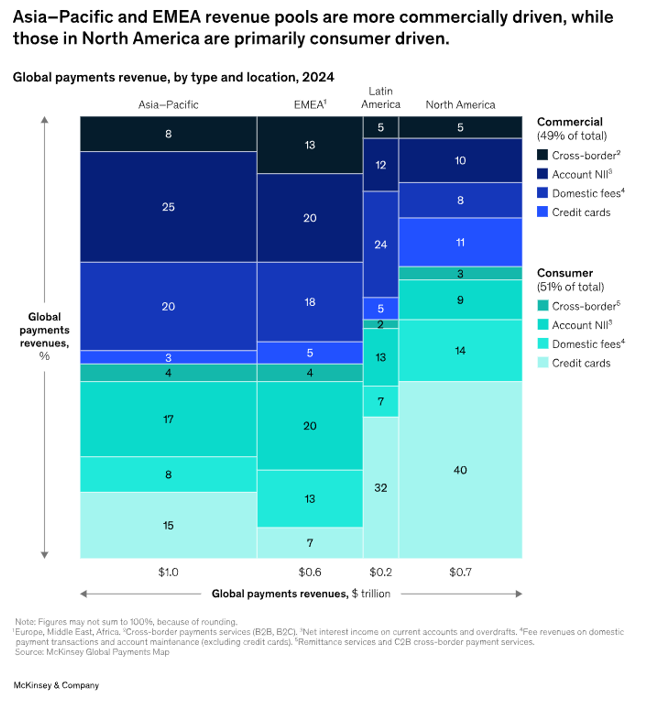

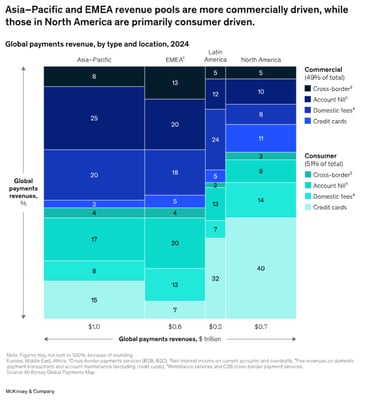

2.2 Regional Breakdown

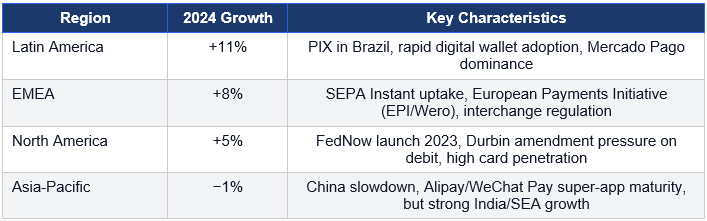

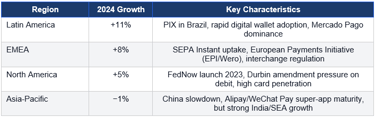

The payments industry is not globally uniform. Geographic fragmentation is one of the industry's most important structural features, creating both complexity for market entrants and durable competitive advantage for those who have built local relationships and regulatory compliance.

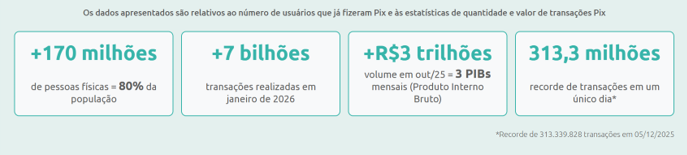

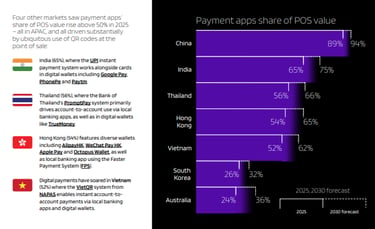

Latin America's outperformance is largely driven by Brazil's PIX, the central bank's instant payment system, which processed over 7 billion transactions in January 2026 alone with adoption exceeding 80% of the adult population — making it a global model for low-cost real-time payments.

Source: Banco central do brasil

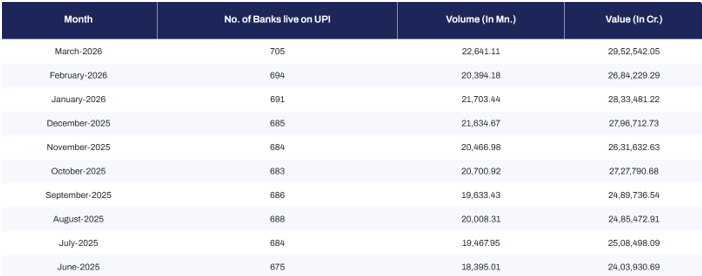

India's UPI system processed approximately 21.7 billion transactions and ₹28.3 trillion ($300 billion) in a single month in January 2026, reinforcing its role as the world's largest real-time payment system by volume.

Source: UPI statistics

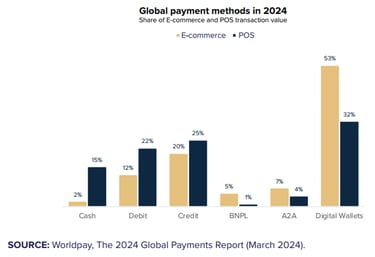

Here are also a few examples of payment rails and methods in different countries beyond your traditional credit cards:

India: Adhaar, Paytm

Brazil: Mercado Pago, Pix

US: Venmo, Cash app, Zelle

Mexico: Mercado Pago, BBVA app

Argentina: Mercado Pago, Uala

Sweden: Swish

Germany: Paypal

Kenya: M-Pesa, Airtel Money

Indonesia: GoPay, OVO

Nigeria: Opay, Palmpay

Source: WorldPay global payment report

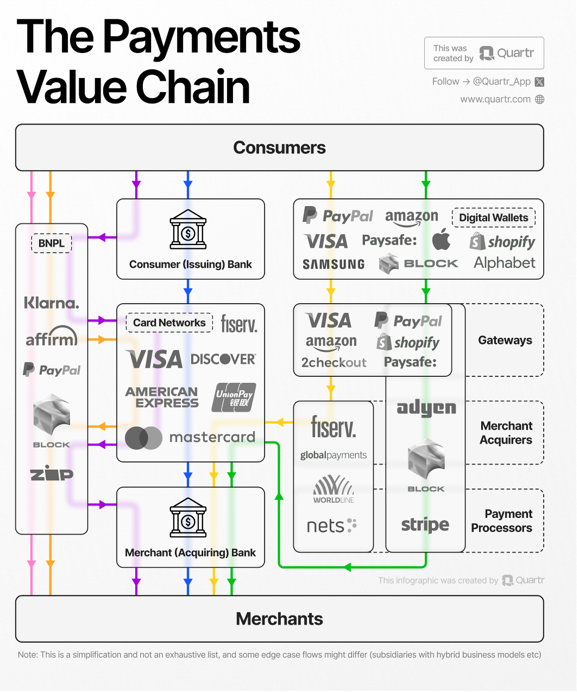

3. The Payments Value Chain

Every electronic payment involves multiple parties operating simultaneously within a tightly coordinated ecosystem. Understanding who does what — and crucially, who earns what — is the prerequisite for any investment analysis in this space.

Just as a cash transaction, non cash payments still need to verify:

The authority of a transaction (that a consumer isn't being 'coerced' and has the authority to transact)

That the transaction is legitimate and not forged in some way

But in addition, non cash payments now needed to verify new things:

That a customer has the funds to pay! In cash this was easy, but in a no cash world someone has to check that the consumer has the funds to transfer.

That funds can and will transfer to the merchant’s bank account

That all the information that's being processed and transferred to perform the above two tasks is done securely.

It's the above three points that credit card payment networks like Visa and Mastercard do. They connect your merchant to the consumers bank account, verifying the right to transact, the funds to do so and make sure the funds settle, while ensuring information security along the way. In return for this work credit card networks take a fee of the processed money.

To ensure all of the above requires several different actors and jobs that need to be done. This is a lot of work for one company, so the two dominant credit card networks, Visa and Mastercard outsourced this work in return for a portion of the fee they take to process transactions. American Express on the other hand does all the consumer issuing and merchant acquiring on their own.

The traditional card payment model involves five core participants.

The Classic Four-Party Model (Visa / Mastercard)

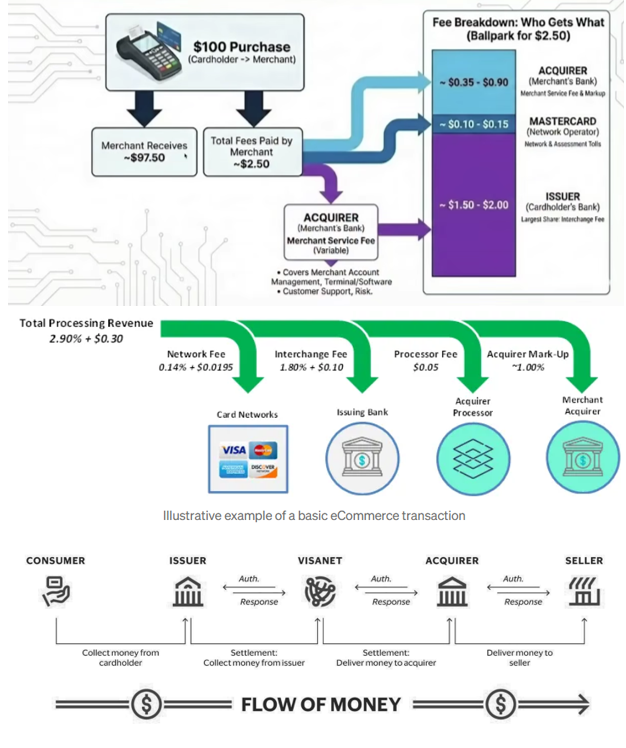

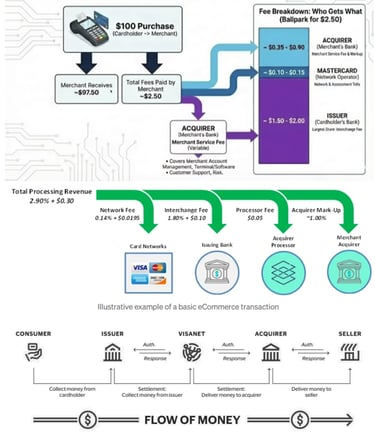

Consumer → Merchant → Acquiring Bank → Card Network → Issuing Bank.

Each party performs a distinct function and extracts a portion of the transaction fee. The total fee to the merchant (the Merchant Discount Rate, or MDR) is typically 2.0–3.0% and is split across the chain.

Source: Medium — Payments Value Chain Economics and Visa Annual Report 2025

3.1 The Consumer (Cardholder)

The consumer initiates the payment and is the ultimate source of all revenue in the chain. Consumers do not typically pay direct transaction fees — instead they are incentivized to use cards via rewards programs, cashback, and purchase protection. These rewards are funded primarily by interchange fees collected from merchants, creating a cross-subsidy from merchants (especially lower-income merchants) to consumers (especially higher-income, high-spend cardholders who maximize rewards).

Consumer behavior is the fundamental variable in the industry: the shift from cash to digital, from physical card to mobile wallet, and increasingly from card to direct bank transfer, all reshape the fee flow through the chain.

3.2 The Merchant (The Coffee Shop)

Merchants are the economic engine of the payments industry — they pay the fees that fund the entire ecosystem.

The Merchant Discount Rate (MDR) they pay typically averages 2.0–3.0% for credit cards and 0.5–1.5% for debit, though rates vary significantly by merchant size, card type, and geography.

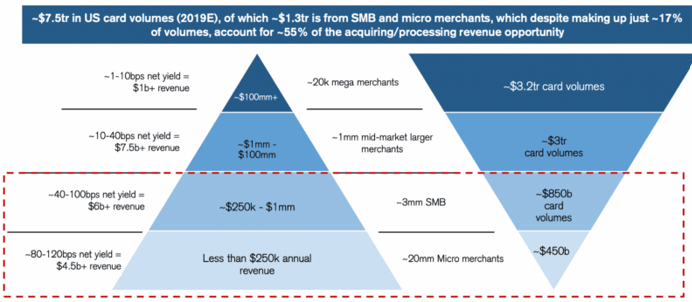

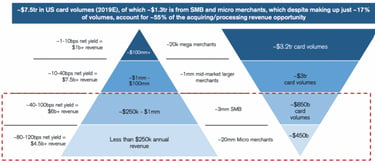

The largest 150 merchants generate more than half of total North American card volume, giving them significant negotiating leverage to secure near-cost-plus rates. The smallest 80% of merchants — small businesses with no bargaining power — effectively subsidize the ecosystem. This is a persistent political and regulatory flashpoint.

Merchants must open a merchant account with an acquiring bank to accept card payments. The acquiring relationship determines the merchant's effective rate, technology access, and fraud exposure. The rise of Payment Facilitators (PayFacs) like Stripe and Square dramatically simplified merchant onboarding, allowing small businesses to accept cards in minutes rather than weeks.

3.3 The Merchant Acquirer / Acquiring Bank (The Coffee Shop's Bank)

The acquirer is the merchant's financial institution — it establishes the formal relationship, underwrites the merchant's risk, and settles funds into the merchant account. After a transaction is authorized, the acquirer pays the merchant within 1–3 business days, effectively extending short-term credit while awaiting settlement from the issuing bank.

The acquirer is exposed to merchant fraud and chargeback risk: if a merchant delivers fraudulent goods and consumers dispute the charge, the acquirer absorbs the loss. This risk-bearing role justifies the acquiring fee, though margins are thin in the commodity processing market.

Most acquiring banks also provide processing services, but in modern infrastructure these roles have bifurcated: a specialized Acquirer Processor (e.g., Fiserv, FIS) handles the technical routing, authorization, and settlement, while the acquiring bank holds the regulatory relationship.

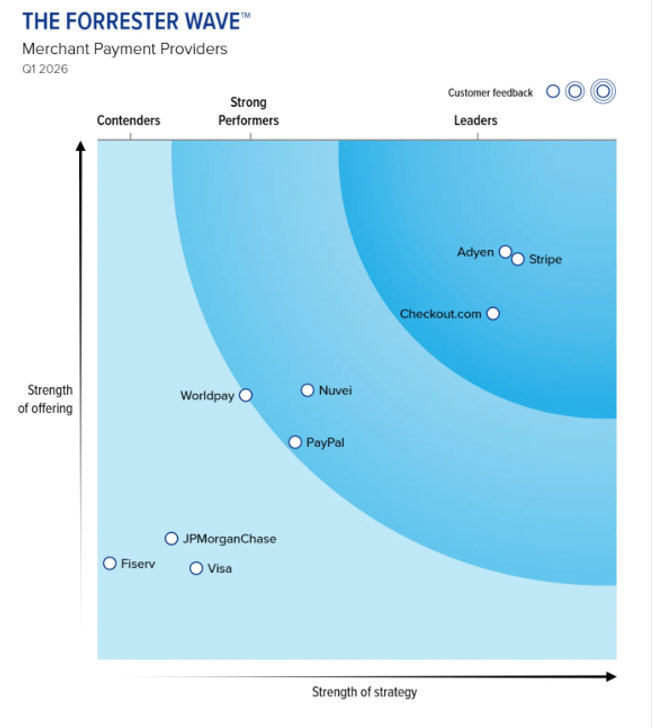

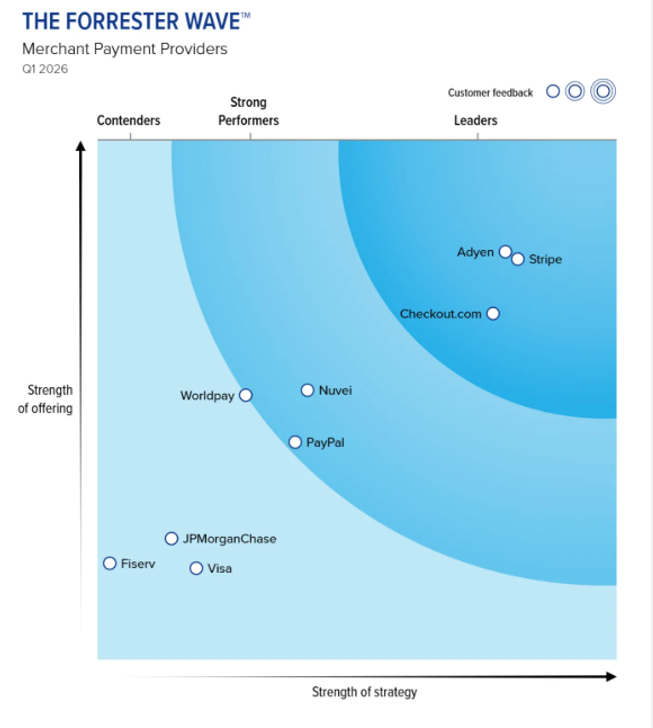

Many modern Payment Service Providers or PSPs (Stripe, Adyen) have acquired their own acquiring licenses, collapsing this distinction. Forrester’s latest research report underlines the growing capability gap between the three leading global processors – Stripe, Adyen and Checkout – and the rest of the industry.

3.4 The Card Network (Visa / Mastercard)

Visa, Mastercard, American Express, and UnionPay are the four-party model's nervous system — they own the electronic rails that connect acquiring banks to issuing banks globally.

Here is something important to understand: Visa and Mastercard do NOT issue cards. They do NOT hold your money. They do NOT take any credit risk. What they own is the network of rules, technical standards, and switching infrastructure that allows any cardholder, anywhere in the world, to pay at any merchant that displays their logo. They earn a small fee — called a network fee or assessment — on every transaction that passes through their rails, and they set the exchange rates (called interchange) between acquiring and issuing banks.

Their economic model is elegant: they do not lend money, they do not take credit risk, and they do not process transactions. They maintain the network, set the rules, manage fraud standards, and collect a small toll on every transaction.

For a standard credit card transaction, Visa and Mastercard each charge a network fee of approximately 0.13–0.15% plus a fixed per-transaction amount. On $100 of spending, the network earns roughly $0.20. This seems small, but across Visa's roughly $15 trillion in annual payment volume, even tiny basis points generate enormous revenue at near 100% incremental margins.

Networks also set and publish the interchange rates that issuers earn — a critical structural choice that effectively determines the economics of the entire chain. By setting high interchange, networks make card issuance attractive for banks, ensuring wide card acceptance, which in turn attracts merchants to the network — a classic two-sided market dynamic.

American Express operates a different three-party model: it is simultaneously the network, the issuer, and in some cases the acquirer — capturing all the economics but also bearing all the risk. This explains AmEx's historically higher interchange rates and its premium positioning.

3.5 The Issuing Bank (Your Bank)

The issuing bank — Chase, Capital One, Bank of America, HSBC, BNP Paribas, Société Générale — is the largest single beneficiary in the card payments chain.

When you tap your card, the card network routes the transaction request to your bank in real time. Your bank checks that you have sufficient credit or funds, verifies that the transaction looks legitimate (not stolen or fraudulent), and either approves or declines the payment — all within 20 milliseconds.

Acquiring customers is a costly act and bears the most risk. Because the issuer has extended credit to the consumer (on a credit card) — if the consumer doesn't pay their bill, the issuer absorbs the loss. The issuer also absorbs fraud losses when transactions are disputed as unauthorized. That's why the acquiring actor receives the lion’s share of the payment processing fee.

It captures approximately 60–70% of the total merchant fee through interchange. On a $100 credit card transaction with a 2.5% total MDR, the issuing bank receives roughly $1.80.

Issuers earn revenue from two sources: interchange (a percentage of every purchase) and interest income (charged on revolving credit card balances, typically at 15–25% APR). Together, these represent a powerful dual revenue model. In the US, where interchange is not regulated for credit cards, this model is enormously profitable. In Europe, where the EU capped interchange at 0.3% for credit and 0.2% for debit in 2015, issuers depend far more heavily on interest income and annual fees.

Issuers compete vigorously for consumer spending through rewards programs — airline miles, hotel points, cashback, and exclusive benefits. These programs are funded by interchange and represent both the industry's greatest consumer value creation and its most politically contested feature.

3.6 Payment Service Providers (PSPs) & Payment Facilitators (PayFacs) (Stripe / Adyen / Square)

Payment Service Providers (PSPs) and Payment Facilitators (PayFacs) are a more recent addition to the ecosystem. They sit between merchants and the traditional bank/acquirer infrastructure, providing a technology layer that simplifies the entire process of accepting payments.

They aggregate thousands or millions of merchants under a single master merchant account, simplifying onboarding, technology integration, and compliance.

Stripe, Adyen, PayPal, and Square pioneered this model.

Think of a PayFac like a corporate umbrella: instead of requiring every small merchant to have their own formal merchant account with a bank (a process requiring credit checks, legal agreements, and weeks of setup), the PayFac holds one master account and lets thousands of sub-merchants operate under it. This allows a coffee shop to start accepting Stripe payments in minutes, not weeks.

The major PSPs today include Stripe (dominant in startups and SaaS companies), Adyen (dominant in large multinational enterprises), Square/Block (dominant in small businesses and restaurants), and PayPal (dominant in e-commerce marketplaces). Each has a different go-to-market strategy and a different set of services layered on top of payment processing.

Rather than setting up individual merchant accounts for each client — a process that historically took weeks — PayFacs sponsor merchants under their own acquiring relationship, enabling same-day onboarding and developer-friendly APIs. The trade-off: the PayFac absorbs the fraud and compliance risk that traditional acquirers would have required merchants to manage themselves.

PSPs typically earn a blended revenue per transaction that includes: (1) the gross MDR minus pass-through costs (interchange + network fees), (2) software subscription fees for billing, fraud, analytics, and reporting tools, and (3) financial services revenue from embedded products like lending, FX conversion, and card issuing.

4. The Mechanics: What Actually Happens in 2s

When you tap your card, a two-second sequence of events unfolds that involves at least four companies, multiple data centers, real-time fraud analysis, and the movement of a virtual IOU across continents. Most people are amazed to learn this happens at all, let alone that it happens reliably at millions of times per second, 24 hours a day, 365 days a year.

4.1 Authorization (The First Second)

The moment you tap your card, the merchant's payment terminal reads your card information and sends an authorization request — encrypted — to the merchant's payment processor. The processor routes it to the relevant card network (Visa, Mastercard, or AmEx). The card network looks up which bank issued your card and forwards the request there in milliseconds.

Your issuing bank then performs a series of checks, all simultaneously:

• Do you have sufficient credit or funds?

• Does this transaction match your normal spending pattern?

• Is the card being used at an unusual location or time?

• Has this card number been reported stolen?

• Does the merchant category seem consistent with your history?

The bank returns an approval code or decline reason back through the same chain — network → processor → terminal. The total round-trip time for this authorization should be under 20 milliseconds for in-store transactions. (As payment technology expert Lisa Ellis noted: standing at a supermarket checkout register waiting more than about 20 milliseconds for authorization makes customers impatient — and this throughput requirement drives enormous technology investment in the industry.)

4.2 Clearing (End of Business Day)

Authorization is not the same as money moving. It is a reservation — the issuing bank has set aside the funds, but nothing has physically moved yet. At end of day, the merchant submits a batch of all its authorized transactions for clearing. This is the reconciliation process: each transaction is matched against its authorization, and the net amounts to be settled between banks are calculated.

4.3 Settlement (1–3 Days Later)

Settlement is when money actually moves. The acquiring bank credits the merchant's account with the sale proceeds (minus fees). The issuing bank debits the cardholder's account (or adds to their credit card balance). The card network facilitates the interbank settlement — the transfer of actual funds from the issuing bank to the acquiring bank, minus the interchange fee that the issuer keeps.

The Key Distinction: Online vs. In-Store Payments

In-store payments are optimized for speed (20ms authorization) and relatively low fraud (the card is physically present, chip-and-PIN confirms identity). Online payments face fundamentally different challenges: there is no physical card present, the customer could be anywhere in the world, and the fraud rate is dramatically higher. According to Adyen's data, digital transactions fail 15% of the time due to declines and fraud friction — compared to only 4% for card-present in-store transactions. This 11-point gap is what drives the enormous investment in online fraud prevention.

4.4 The Three-Party Model: American Express

American Express operates differently. Instead of using separate issuing and acquiring banks connected through a shared network (the four-party model), AmEx handles everything itself: it issues the cards directly to consumers, acquires the merchant relationships directly, and operates its own network. This is called a three-party or closed-loop model.

This gives AmEx several advantages: richer data (it sees both sides of every transaction), direct consumer and merchant relationships, and the ability to set its own terms without negotiating with banks. The downside is that AmEx must invest its own capital in the issuing and acquiring businesses, and its network is only as large as its direct relationships allow — hence American Express is still not accepted everywhere, particularly among smaller merchants who object to its historically higher merchant fees.

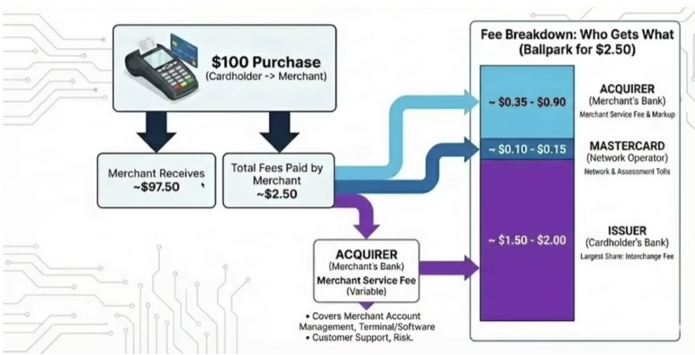

5. The Economics: Where the Money Goes on Every Purchase

5.1 The Anatomy of a Transaction Fee

When a consumer pays $100 with a rewards credit card at a typical retail merchant, the following fee flows occur almost instantaneously. This breakdown is critical for investors seeking to understand where economic value is actually created and captured.

This fee structure illustrates one of the industry's most important structural features: the issuing bank captures by far the largest share, yet does the least "work" at transaction time. The issuer's high take-rate reflects its role as the credit risk-bearer, consumer relationship owner, and funding source — but it also reflects the political economy of interchange-setting. Card networks have historically set interchange high to make card issuance attractive for banks, ensuring a wide network of cards in circulation — and thus attracting merchants to accept them.

5.2 Interchange: The Industry's Central Economic Mechanism

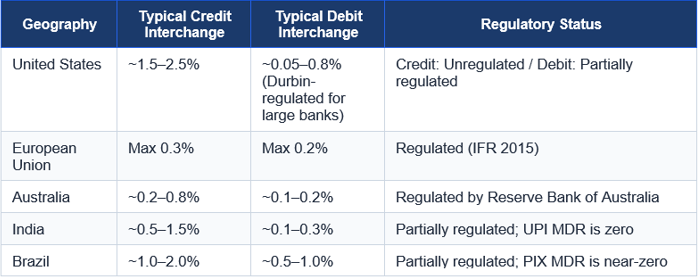

Interchange is simultaneously the industry's most important economic lever and its most politically contested element. It is a transfer payment from the merchant's bank (the acquirer) to the consumer's bank (the issuer) for every card transaction. The interchange rate is set by the card network (Visa and Mastercard) — not negotiated between banks — and varies based on:

• Card type (credit vs. debit vs. prepaid vs. commercial)

• Transaction type (card-present vs. card-not-present / online)

• Merchant category code (MCC) — grocery stores pay lower interchange than airlines

• Authentication method — chip/PIN typically qualifies for lower rates than magnetic stripe

• Card tier — standard, rewards, premium, commercial cards carry progressively higher interchange

In the United States, where credit card interchange is unregulated, premium rewards cards carry interchange of up to 2.5–3.0%. The Durbin Amendment (2010) capped debit interchange at ~$0.21 + 0.05% for large banks, effectively eliminating debit rewards programs and redirecting value from issuers to merchants and consumers.

In the European Union, Interchange Fee Regulation (IFR, 2015) capped credit card interchange at 0.3% and debit at 0.2%. %. This regulatory difference explains much of why the European payments market looks so different from the American one. As this dramatically compressed issuer economics in Europe, accelerating the region's shift toward A2A (account to account) payment alternatives.

Source: CGAP — Acquiring Models

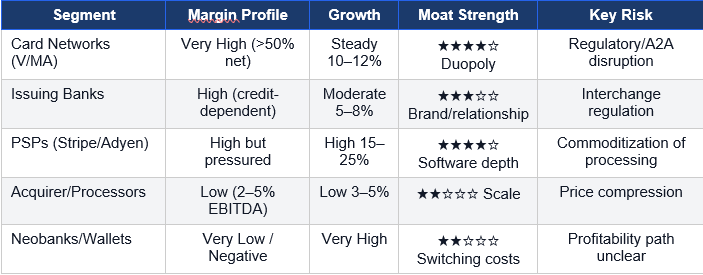

5.3 Profit Pools by Segment

From an investment perspective, not all participants in the payments value chain have equal economic characteristics. The table below summarizes the key investment metrics by segment.

6. Key Players & Competitive Landscape

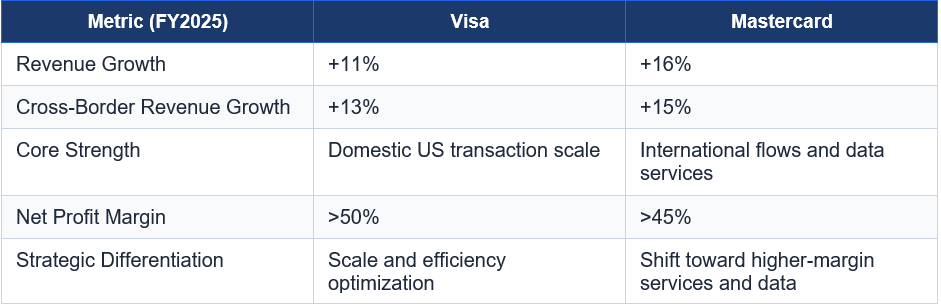

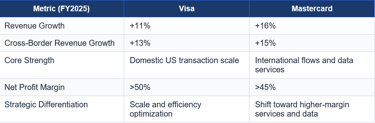

6.1 Card Networks: The Duopoly

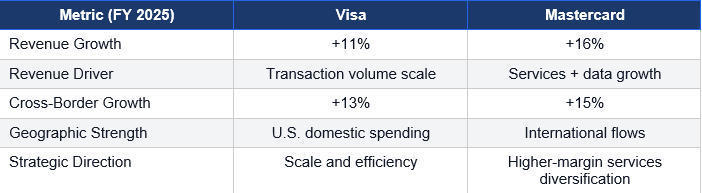

Visa and Mastercard represent one of the most durable duopolies in global finance. Together they process the overwhelming majority of global card transactions through their respective networks. Their business model — owning the rules, standards, and rails without taking any balance sheet risk — generates extraordinary returns.

Mastercard's faster growth reflects its deliberate shift toward data analytics, cybersecurity, and consulting services — revenues that are less dependent on transaction volume and carry higher margins. Visa's strategy has remained more tightly focused on scale efficiencies from its dominant volume position. Both companies benefit from the same structural moat: network effects that make it virtually impossible for a new global card network to achieve critical mass against a 60-year head start.

American Express occupies a distinct position. Its closed-loop three-party model gives it richer data, stronger merchant relationships, and higher interchange — but limits network ubiquity. AmEx has deliberately positioned as a premium brand, with its cards carrying average spending per account significantly above Visa or Mastercard equivalents. This premium positioning creates resilience in economic downturns as AmEx's customer base skews higher-income.

6.2 Payment Service Providers: The New Generation

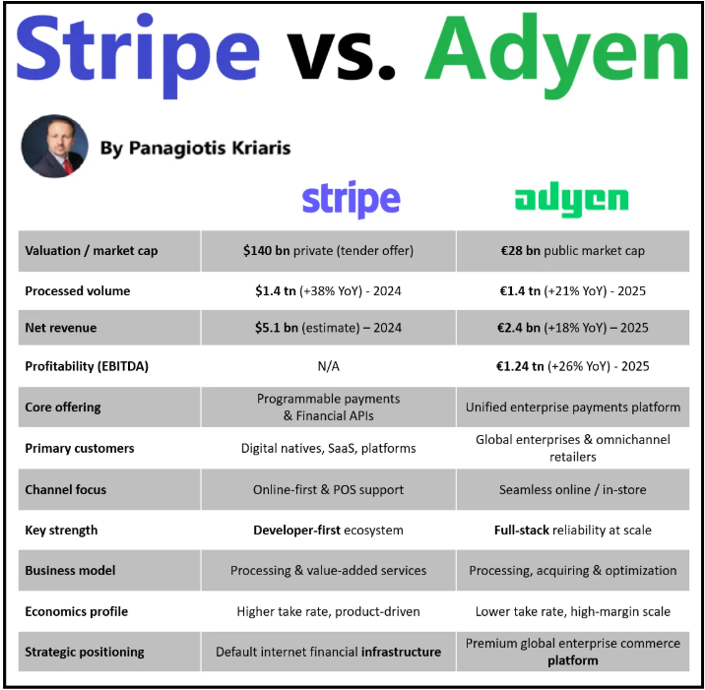

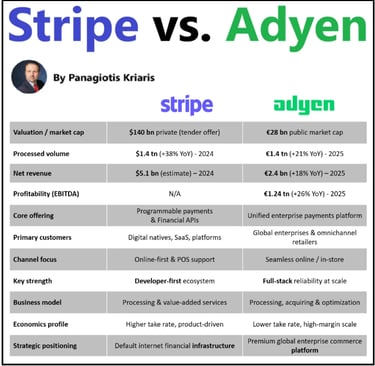

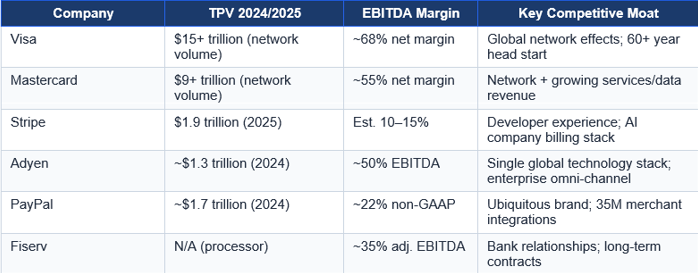

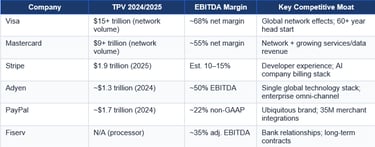

The PSP layer — companies that provide full-stack payment technology to merchants — has been the industry's fastest-growing and most valuationally dynamic segment over the past decade. The two dominant players, Stripe and Adyen, have different models, different customer bases, and different paths to long-term value creation.

Source : Paniagotis FinTech Newsletter

For modern PSPs like Stripe and Adyen, the key revenue metric is the take rate — the net revenue earned as a percentage of Total Payment Volume (TPV) processed. This is different from the gross MDR: the PSP (Payment Service Provider) first collects the full MDR from the merchant, then passes through the interchange and network fees (which it does not keep), and retains only its margin.

If Adyen processes $100 of a merchant’s sales, the merchant pays the full Merchant Discount Rate (roughly $2.00–2.50 gross) to cover interchange, network fees, and Adyen’s own margin. After passing through interchange and network fees to issuing banks and Visa/Mastercard, Adyen retains approximately $0.17 — a ~17 basis point net take rate. It is this 17 basis points, multiplied across €1.3 trillion in TPV, that drives Adyen’s ~50% EBITDA margins. Crucially, Adyen’s net take rate actually expanded from 14.7 bps in H1 2024 to 17.1 bps in H2 2025.

Take rate is the most watched metric for payments investors because it captures the pricing power and product depth of a PSP. A higher take rate indicates either premium pricing (the PSP offers differentiated services worth paying for) or a mix shift toward higher-margin products. A declining take rate can signal healthy volume growth from lower-margin enterprise clients, or dangerous commoditization.

The critical investor observation about this layer is commoditization risk. Because the core processing service is technically undifferentiated — authorization, clearing, and settlement are identical regardless of provider — merchants routinely run multiple processors in parallel and can shift volume between them by "turning a dial." Stripe and Adyen's moats, therefore, do not rest on payments processing per se, but on the depth of their software platforms, the breadth of their financial services stack, and the switching costs created by deep integrations into merchant ERP, accounting, and operations systems.

Stripe's acquisition of Bridge (stablecoin infrastructure, ~$1B) and its buildout of treasury, lending, issuing, and tax products reflects a deliberate strategy to expand the number of financial services each merchant uses — increasing revenue per customer and raising switching costs. Adyen's moat is more operational: its single global technology stack eliminates the integration overhead and performance variability of assembling multiple regional processors, which is highly valuable for multinational retailers operating across dozens of payment methods and currencies.

6.3 Legacy Processors: The Challenged Incumbents

The largest payment processors by revenue — Fiserv, FIS, Global Payments, and Worldpay — were built through decades of acquisitions rather than organic technology development. This heritage creates both scale advantages and profound structural challenges.

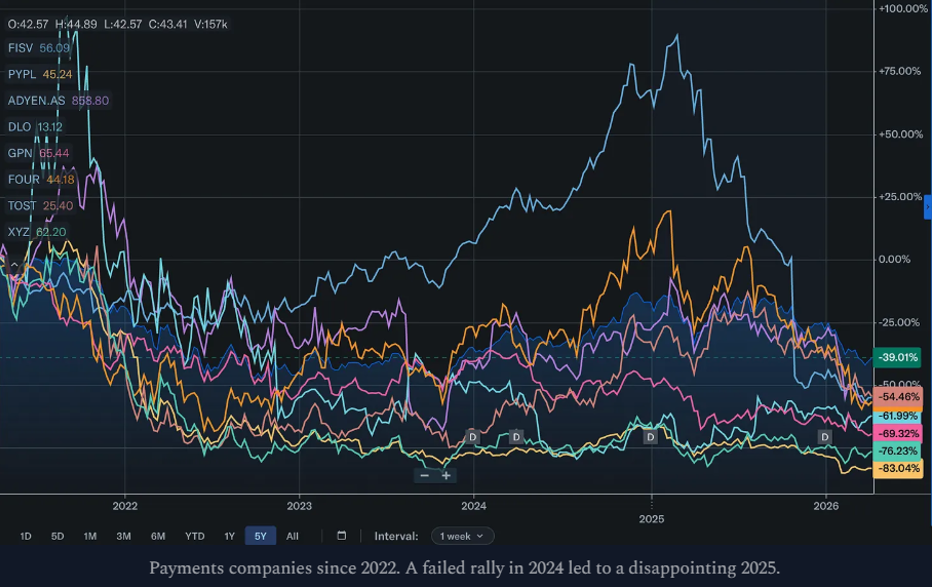

Fiserv's stock dropped 40% after Q3 2025 results showed only 1% revenue growth and a significant earnings miss. Its new CEO attributed underperformance to predecessors' strategy of "short-term decisions to cut costs and defer investment" — a pattern visible across much of the legacy processing industry. These incumbents generate large volumes of revenue from sticky bank relationships and long-term merchant contracts, but their fragmented technology stacks — often running on systems from acquired companies — make them slow to innovate and increasingly vulnerable to the full-stack competition from Adyen and Stripe in the enterprise tier, and from Square and SumUp in the SME tier.

6.4 Super-Apps & Regional Champions

In Asia, the Western card-network model never achieved dominance. Alipay (Ant Group) and WeChat Pay (Tencent) together control over 90% of China's mobile payments market, operating as vertically integrated ecosystems where payments are embedded within a broader platform of social, commerce, and financial services. This model — where payments are a utility layer inside a super-app — represents the alternative evolutionary path for digital payments.

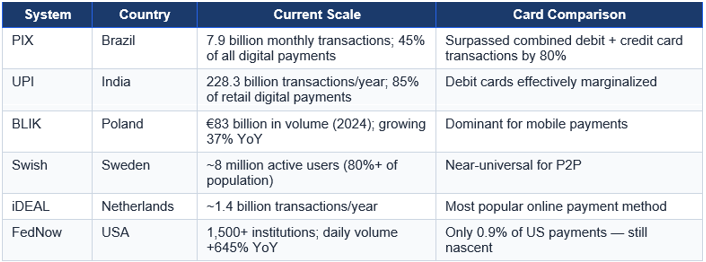

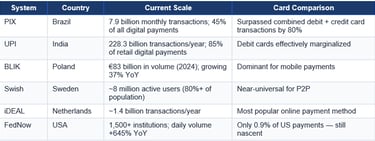

India's UPI, Brazil's PIX, Poland's BLIK (processing €83 billion in 2024, growing 37% year-over-year), and Sweden's Swish all demonstrate that government-backed real-time payment infrastructure can achieve massive scale in a single market. Each threatens the card model in its home jurisdiction and represents a global model for what A2A payments can achieve.

7. Business Models & Competitive Moats

7.1 The Toll-Road Model (Card Networks)

Visa and Mastercard are the definitive toll-road businesses in financial services. They own the infrastructure through which trillions of dollars flow, charge a tiny fee on each flow, and do so at near-zero marginal cost. The critical insight is that their revenue is driven by the number and value of transactions, not by any balance sheet activity — they take no credit risk, hold no deposits, and require almost no capital to grow.

The durability of this model rests on three reinforcing advantages: (1) network effects — the more cardholders there are, the more valuable Visa is to merchants, and vice versa; (2) trust infrastructure — decades of fraud protection standards, dispute resolution, and consumer guarantees that are extremely difficult to replicate; and (3) brand — Visa's and Mastercard's logos at checkout represent an implicit guarantee of security and interoperability that no new entrant can quickly match.

Investor Insight: Why Visa & Mastercard Have Exceptional Moats

Even if a competitor could build superior technology, they would need to simultaneously convince millions of banks to issue their cards, tens of millions of merchants to accept them, and billions of consumers to carry them — all at the same time. This cold-start problem makes the Visa/Mastercard duopoly one of the most defensible competitive positions in global business.

7.2 The Scale Compounding Model (Adyen/Stripe)

PSPs like Adyen demonstrate a different but equally powerful dynamic: the scale compounding model. As transaction volume grows, the fixed cost of the technology infrastructure is spread across more transactions, driving EBITDA margin expansion. Adyen's EBITDA margin is approximately 50% as of 2025 — extraordinary for a technology company at its scale.

Scale brings advantages on both the cost and revenue side simultaneously: (1) higher volume unlocks better rates from card networks and issuing banks; (2) larger merchant portfolios generate richer fraud data, improving authorization rates and reducing losses; (3) more data enables smarter payment routing, further improving conversion for merchants; and (4) deeper integration into merchant operations raises switching costs.

The "payments pyramid" — a concept from Credit Suisse analysis — describes how the industry bifurcates into two go-to-market strategies: Stripe's developer-led bottoms-up adoption in the SME and startup segment, and Adyen's enterprise top-down relationship model. Both are valid and neither is inherently superior — they target structurally different customer segments with different buying processes and different value drivers.

7.3 The Commoditization Trap (Legacy Processors)

The inverse of the scale compounding story plays out in the commodity processing layer. When processing is purely a technical service — authorization, clearing, settlement — it becomes price-competitive and subject to margin compression. The history of the acquiring/processing industry is largely a history of consolidation in pursuit of scale: FIS acquired Worldpay for $43 billion in 2019; Fiserv acquired First Data for $22 billion; Global Payments acquired TSYS for $21 billion.

Yet scale alone has not protected margins. The fundamental problem is that switching barriers are low for digital-first merchants and the processing layer is visible to the merchant — making it a cost centre they actively seek to optimize. This is why the surviving profitable businesses in the processor tier are those that have added software, value-added services, or specialized vertical expertise (e.g., Shift4's focus on hospitality, stadiums, and casinos).

7.4 Why in all those Scale Is the Holy Grail

The payments business is characterized by very high fixed costs (technology infrastructure, compliance, regulatory licenses) and near-zero marginal costs (processing one more transaction costs essentially nothing). This means that as volume grows, every additional transaction produces almost pure margin.

This is the scale compounding model. Consider Adyen's economics: in 2025, its net revenue was approximately €2 billion on EBITDA margins near 50%. As volume grows, fixed costs stay roughly constant, so nearly all incremental revenue flows to EBITDA. This is why payments companies aggressively pursue volume growth even at razor-thin take rates — because the operating leverage is so powerful

8. How The Industry Evolved: Three Waves of Disruption and Key Trends Reshaping the Industry

8.1 Wave 1 — The Card Revolution (1960s–1990s)

Visa and Mastercard were created as cooperative associations of banks in the 1960s and 1970s to solve a shared problem: how to let any consumer pay any merchant, anywhere, without each bank needing a direct relationship with every other bank. Their solution — a shared network with common rules and technical standards — was one of the great technological achievements of the 20th century.

The infrastructure they built was, and remains, extraordinary. In-store payments require processing millions of transactions per second with authorization times under 20 milliseconds. These are massive, highly resilient data centers processing an unimaginable volume of tiny messages, 24 hours a day, 365 days a year. It is the financial world's equivalent of air traffic control.

For decades, this infrastructure was owned and operated by a small group of financial institutions: the acquiring and issuing banks, along with specialized processors like First Data (later acquired by Fiserv), FIS, and Worldpay. These companies built the pipes that carry trillions of dollars annually — and most consumers have never heard of them.

8.2 Wave 2 — The E-Commerce Revolution (2000s–2015)

The internet changed everything. When payments moved online, all the assumptions of the physical card world broke down. There is no physical card present. The customer could be anywhere in the world. The merchant has no way to verify identity through a PIN. And fraud — which had been manageable in the physical world — exploded.

According to Stripe's 2024 annual letter, fraud costs the average online business approximately 3% of its revenue. To put that in perspective: many online businesses operate at 10–15% net margins. Fraud at 3% of revenue represents 20–30% of net profit, wiped out before the business earns a cent. Fraudsters operate at industrial scale, with teams of engineers, data analysts, and managers working full-time to steal from online merchants.

The incumbents — Fiserv, FIS, the traditional acquiring banks — were not built for this environment. Their technology was optimized for physical, in-store transactions with known fraud profiles. Into this gap stepped a new generation of companies.

PayPal was the first dot-com era company to solve online payment trust at scale, creating a system where buyers and sellers could transact without sharing sensitive financial information directly. Founded in 1998, it became the de facto payment method for eBay (which eventually acquired it) and the foundation of the online payment ecosystem.

8.3 Wave 3 — The Software Revolution: Square and Stripe

The second major disruption of the 2010s came not from the internet but from the 'consumerization of business software' — the expectation that business tools should be as easy to use as consumer apps. Two companies embodied this revolution from different directions.

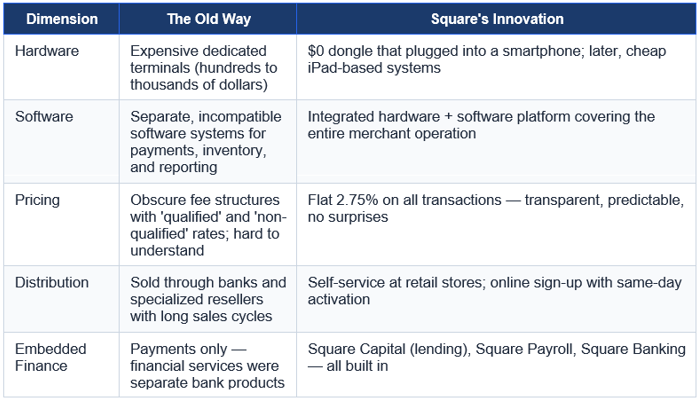

Square (Now Block): Reinventing the Physical Point of Sale

Square's disruption of in-store payment processing was so comprehensive that it serves as a template for understanding how mature technology markets get disrupted. The traditional POS (point-of-sale) hardware market in 2009 was expensive, complicated, and controlled by banks and large processors. Square disrupted it on five dimensions simultaneously:

Square essentially showed the industry that payments infrastructure could be reimagined from scratch — not as a banking product sold through banks, but as software sold directly to merchants who needed it.

Stripe: Reinventing Online Payments for Developers

If Square disrupted physical payments, Stripe disrupted online payments. Founded in 2010, Stripe's insight was that the existing tools for accepting online payments were so technically complex that most developers spent weeks just wiring them up before they could write a single line of their actual business logic.

Stripe reduced the integration from weeks to minutes. Their API was so clean, their documentation so clear, and their developer experience so superior that word spread through the startup community virally. Companies like Lyft, Airbnb, DoorDash, and thousands of others chose Stripe not because a salesperson called them but because their engineers recommended it.

Stripe's strategy has been to compound their advantage over time by expanding from payments processing into a full financial infrastructure stack: billing and subscriptions, fraud prevention (Radar), corporate cards (Stripe Issuing), treasury management, tax compliance, identity verification, and, most recently, stablecoin infrastructure through the $1 billion acquisition of Bridge. Stripe's TPV reached $1.9 trillion in 2025, growing 34% year-over-year, at a scale where such growth rates are extraordinary. Its private valuation reached $159 billion in a February 2026 tender offer — more than three times the market capitalization of Fiserv.

Stripe's AI Dominance: The Most Important Strategic Fact of 2025

Stripe has captured essentially the entire billing infrastructure of the AI economy. OpenAI, Anthropic, Replit, Cursor, Perplexity, ElevenLabs, and Windsurf are all billed through Stripe. In January 2026, Stripe acquired Metered Billing company Metronome for approximately $1 billion — specifically designed to own metered usage pricing, which Stripe's CEO called 'the native business model of the AI era.' This is not coincidental. As AI companies grow and their revenues compound, Stripe's take from that ecosystem grows proportionally.

8.4 The Omni-Channel Challenge

As e-commerce grew, a new problem emerged for large retailers: how to unify the physical and digital payment worlds. A customer might buy online and return in-store. Or buy in-store and get customer service online. If a retailer uses one payment processor for its website and a different one for its stores, these two systems may not share data — making refunds, chargebacks, loyalty programs, and customer analytics a nightmare.

This is the 'omni-channel' challenge, and it became particularly acute during COVID-19 when 'buy online, pick up curbside' became standard retail behavior. Managing two completely separate payment flows — with different fraud profiles, different data formats, and different settlement cycles — was enormously complex.

Very few payment companies can bridge this gap. Adyen is the clearest example: its single global technology stack handles both in-store and online payments through the same system, giving merchants a unified view of every transaction regardless of channel. This is Adyen's core 'Unified Commerce' value proposition and a key reason it has won large enterprise accounts like McDonald's, H&M, L'Oréal, and eBay.

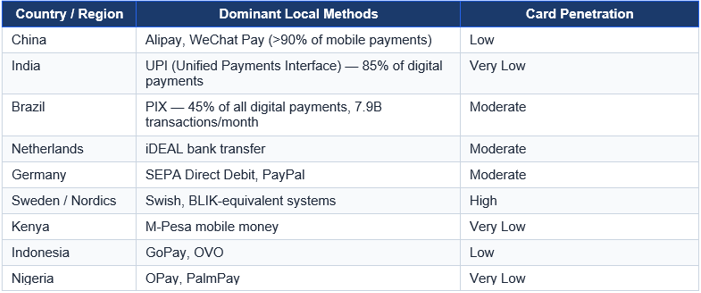

8.5 The Global Complexity: Why Geography Is Destiny

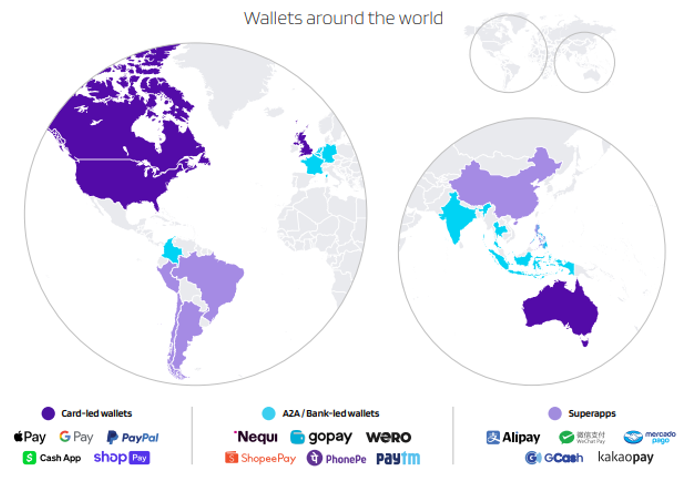

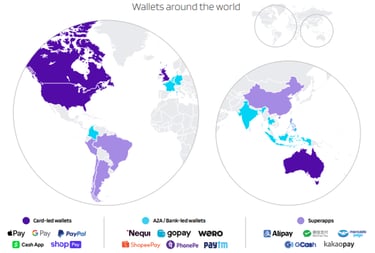

One of the most important and least understood aspects of the payments industry is that it is radically fragmented by geography. A global merchant cannot simply choose Stripe or Adyen and expect to reach every customer on earth. Local payment methods, currencies, regulations, and acquiring relationships all vary enormously by market.

While Visa and Mastercard are widely accepted in the US and Western Europe, they are far from dominant globally. In most of the world, consumers use a mix of local payment methods that are more convenient, cheaper, or simply more trusted:

dLocal, the payment processor for emerging markets, offers over 900 distinct payment methods across 40 countries. A global e-commerce company that ignores local payment methods is not just leaving revenue on the table — it is often locking out the majority of the market entirely. But Beyond accepting local payment methods, there is a second dimension of geographic complexity: local acquiring.

When a multinational merchant processes a payment through a non-local acquiring bank (for example, routing all European transactions through a US-based processor), two things happen: the authorization rate drops and the cost goes up.

Data from payment analytics company Rapyd shows that approval rates for local cards used in online purchases jump from just 20–45% with offshore acquiring methods to over 80% with local acquiring solutions. This is a staggering difference. A merchant who fails to use local acquiring in Latin America may be declining more than half of all attempted purchases — losing customers who genuinely wanted to buy.

Local acquiring requires a payment processor to hold banking licenses and maintain relationships with local banks in each market — an enormously expensive and complex operation. Companies like Adyen, Stripe, and dLocal have spent years building out these local infrastructure networks. For smaller competitors, the cost of geographic expansion is a nearly insurmountable barrier to entry.

In emerging markets — Latin America, Africa, Southeast Asia, South Asia — the payments landscape is fundamentally different from developed markets:

• Credit card penetration is far lower. In many countries, fewer than 20% of adults have a credit card.

• Currencies are volatile. Processors must manage FX risk in currencies that can devalue dramatically overnight — the Argentine peso, Turkish lira, Nigerian naira.

• Regulatory environments are less predictable. Operating a payment business in Brazil requires navigating a web of regulations from the Banco Central do Brasil, the country's central bank — and those regulations change frequently.

• The payments infrastructure can itself be unstable. Mobile network quality, electricity, and banking connectivity may be unreliable.

Despite these challenges — or rather, because of them — emerging markets represent the highest-growth opportunity in payments. A market where 70% of adults are unbanked and cash is dominant has enormous runway for electronic payment adoption. A question for investors is which companies have the operational capability, the local relationships, and the financial resilience to capture that growth profitably, and are they at attractive prices.

9. Disruptions & Structural Threats

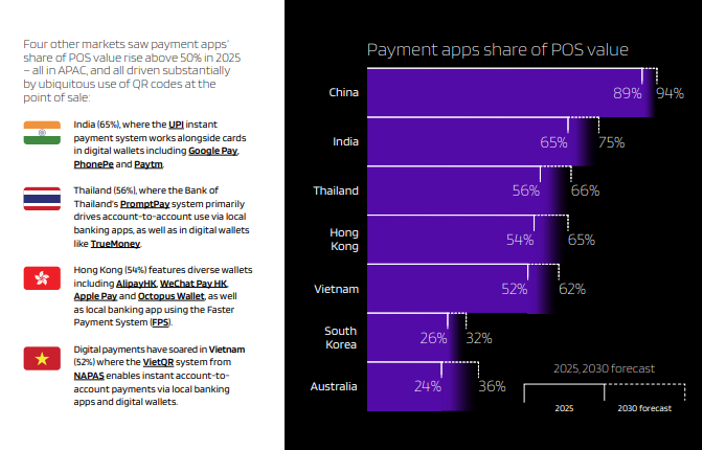

9.1 Real-Time Payments & Account-to-Account (A2A) Transfers

The most strategically significant secular trend in global payments is the rise of real-time, account-to-account transfers as an alternative to card networks— bypassing Visa, Mastercard, and the entire card infrastructure entirely.

When you use Venmo to split dinner, or a Brazilian business uses PIX to pay a supplier, or an Indian consumer uses UPI to pay a street vendor — these are A2A transactions. They settle directly between bank accounts, typically in real time, with no card network involved.

The economic case for A2A is overwhelming for merchants. Card networks charge merchants 1.5–3% per transaction. A2A rails charge a fraction of that. PIX in Brazil charges merchants 0.22–0.33%. That is a 6–10x cost reduction. For a grocery store with 2% net margins, the difference between paying 2.5% in card fees versus 0.3% in PIX fees could double their profitability on digital transactions.

The evidence of A2A's scale is now undeniable. Even outside of Brazil's PIX, Europe's SEPA Instant Credit Transfer or Wero, and india’s UPI. The United States' FedNow, launched in July 2023, is targeting coverage of over 80% of US deposit accounts. Europe's instant payments market is also projected to grow tenfold by 2028.

Source: GR4VY Payment Statistics 2025

Despite its momentum, A2A does not eliminate the need for payment processors — it just changes their role. This is a critical nuance for investors. Consider PIX in Brazil:

• PIX settles only in Brazilian Reais (BRL) through Brazilian bank accounts. A cross-border merchant cannot connect directly to PIX from their US headquarters — they still need a local processor like dLocal to bridge the connection.

• PIX has no consumer fraud protection equivalent to card chargebacks. If a consumer pays by PIX and receives defective goods, there is no automatic dispute resolution mechanism — unlike card payments.

• For cross-border payments, the processor remains essential for currency conversion, regulatory compliance, and KYC (Know Your Customer) checks.

The take rate on A2A transactions is substantially lower than on card transactions. But — crucially — the gross margin can actually be higher, because there are no interchange or network fees to pass through. The processor keeps less per transaction, but retains a larger portion of what it does keep.

For investors in card networks (Visa, Mastercard), A2A is a slow-motion structural headwind. The card networks' response — heavy investment in tokenization, value-added services (data analytics, fraud tools, consulting), and defending consumer protections as a marketing advantage — is the right strategic move, but it does not fully offset the long-term revenue pressure from interchange compression as the economic incentive to go for A2A is there for merchant to motivate the switch.

For investors in PSPs, A2A changes the revenue profile but not the necessity of the business. Adyen and dLocal are actively processing A2A transactions in markets where they dominate. dLocal launched SmartPix in Q2 2025 specifically to monetize PIX volume. Brazil became dLocal's highest-margin geography despite the lower take rate — because the absence of pass-through interchange costs improves gross margin structure.

9.2 Stablecoin & Tokenization

A stablecoin is a digital asset designed to maintain a constant value relative to a reference currency — most commonly the US dollar. Unlike Bitcoin or Ethereum, which fluctuate wildly in value, a dollar stablecoin like USDC or Tether always equals $1. Stablecoins combine the programmability and global accessibility of cryptocurrency with the stability of traditional currency.

Think of a stablecoin as a digital dollar that can move anywhere in the world, instantly, at near-zero cost, 24 hours a day, 365 days a year — including weekends and public holidays when traditional banking systems are closed.

Stablecoins have grown from a niche cryptocurrency product to a mainstream financial instrument:

• Global stablecoin market capitalization grew from approximately $125 billion to over $255 billion in just over a year (per ECB data), with some 90% of that value concentrated in just two issuers (USDC and Tether).

• Total stablecoin transfer volume reached $33 trillion in 2025 — up 72% year-over-year.

• 99% of stablecoins are denominated in US dollars, creating significant geopolitical implications for non-dollar economies.

• Stripe acquired Bridge, a stablecoin infrastructure company, for over $1 billion in 2025. Mastercard acquired BVNK (another stablecoin infrastructure company) for up to $1.8 billion.

Stablecoins have genuine utility in two specific contexts: cross-border B2B payments (where traditional wire transfer fees of 2–5% create enormous cost-reduction opportunity) and as a store of value in countries with unstable local currencies (Turkey, Argentina, Nigeria).

However, they carry significant risks that the payments and banking industry must manage:

• Financial stability risk: If a major stablecoin lost its dollar peg (as Terra/Luna did catastrophically in 2022, destroying $40 billion in value overnight), the ripple effects could destabilize banks and financial markets.

• Banking disintermediation: If consumers hold stablecoins instead of bank deposits, banks lose the funding base they rely on to make loans — a threat to the entire credit system.

• Monetary sovereignty: For non-US countries, the mass adoption of dollar-denominated stablecoins represents a form of de facto dollarization that could undermine domestic monetary policy.

Tokenization refers to representing ownership of a real-world asset — a government bond, a share of stock, a piece of real estate — as a digital token on a distributed ledger. The ECB's description captures it well: a tokenized asset carries two sets of information simultaneously: the asset itself (what it is, who holds it, who issued it) and the rules about how it can be used (who can hold it, how ownership transfers, and complex rules compiled into smart contracts).

For payments, tokenization is relevant in two ways. First, payment card tokenization — replacing a card number with a cryptographic token — is already mainstream and is reducing fraud and improving authorization rates at scale. Mastercard has set a goal to eliminate manual card entry entirely by 2030; Visa has already tokenized 50% of all digital transactions through its Token Service, issuing 12.6 billion tokens. Second, broader financial asset tokenization (bonds, securities) is beginning to enable new settlement models where the ECB is conducting active experiments.

For investors, tokenization has compounding benefits: it reduces fraud (tokens cannot be reused outside their intended context), improves authorization rates (tokens carry richer context), and strengthens the card networks' position in the digital payment stack. It also deepens the relationship between the network and issuers — tokens are managed at the network level — potentially allowing networks to capture more value from the A2A migration by becoming the identity and authentication layer for digital commerce.

9.3 Artificial Intelligence in Payments

AI is restructuring payments operations across three dimensions: fraud detection, payment routing optimization, and customer service.

The scale of the fraud problem justifies significant AI investment — fraud costs the average online business approximately 3% of revenue, operating on an industrial scale with specialized teams of engineers and analysts.

Fraud Detection and Prevention

Fraud is an existential challenge for online payments. According to Stripe's 2024 annual letter, fraud costs the average online business 3% of revenue — not 3% of profit, but 3% of top-line revenue. Fraudsters operate on an industrial scale: dedicated teams of engineers, managers, and data scientists working full-time to steal from merchants using AI-generated deepfakes, mass credential-testing, and sophisticated social engineering.

In response, payment processors use machine learning models trained on billions of transactions to detect anomalies in real time. Every transaction is scored against thousands of variables — transaction size, location, device fingerprint, time of day, merchant category, and behavioral patterns — to generate a fraud probability score in milliseconds. The arms race between fraud prevention AI and fraud execution AI is ongoing and intensifying.

Payment Routing Optimization

Large merchants typically connect to multiple payment processors simultaneously. AI-driven orchestration platforms dynamically route each transaction through whichever processor has the highest predicted authorization rate for that specific card, at that specific time. These systems use machine learning models — what Checkout.com calls 'hierarchical contextual multi-armed bandit algorithms' — to continuously optimize routing. The result: higher authorization rates for merchants and lower costs, with the processor being competed away from on pure price.

The Business of Payments newsletter describes these systems as using "hierarchical contextual multi-armed bandit algorithms" to maximize authorization at minimal cost. This optimization layer is increasingly a standard expectation for enterprise merchants.

Operational Automation

Inside payment companies themselves, AI is automating significant portions of operations: customer support, chargeback dispute management, compliance monitoring, and reconciliation. Checkout.com reports that AI now automates 100% of its rejected transaction distribution and is expected to handle 50% of support volume by 2026.

Agentic Commerce: When AI Does the Buying

As AI assistants become capable of autonomously browsing the web, comparing products, and completing purchases — without a human at the keyboard — the entire model of a consumer initiating a payment at a checkout page begins to break down.

This is already happening. OpenAI partnered with Stripe to introduce an Agentic Commerce Protocol, allowing transactions to be initiated within ChatGPT conversations. Google announced an Agent Payments Protocol with over 60 partners including Adyen, Mastercard, PayPal, and Coinbase. PayPal launched an agent-ready checkout in early 2026 enabling its 35 million merchants to accept payments from AI-driven conversations.

The security challenges are substantial: traditional fraud detection models assume a human is present — they look for behavioral biometrics like typing speed, mouse movements, and session dynamics. When an AI agent is the buyer, these signals vanish. The industry is developing new authentication standards — delegated credentials, spending limits per agent, scope-bounded payment tokens — but the standards are still being written.

9.4 Big Tech & Platform Competition

The global mobile payments market is experiencing explosive growth. Apple Pay is expected to reach over 500 million global users in 2025, handling approximately 12% of all online card transactions globally. Google Pay surpassed 150 million users worldwide in 2024. In China, Alipay and WeChat Pay together account for over 90% of the mobile payments market.

Digital wallets have fundamentally altered the consumer-payment interface. Increasingly, consumers do not think in terms of which bank card they are using — they think about their wallet (Apple Pay, Google Pay, PayPal). This creates a new layer of consumer interface ownership that neither Visa nor Mastercard fully controls.

Apple, Google, Meta, and Amazon each represent a potential strategic threat to traditional payments players — they own the consumer interface at which payment credentials are stored and used. Apple Pay and Google Pay are already deeply embedded in consumer payment behavior. Amazon's in-house payment infrastructure processes its enormous e-commerce volume with minimal fees flowing to the traditional card ecosystem.

However, Big Tech has so far chosen to route payments through existing card rails rather than build competing infrastructure. This decision is primarily driven by regulatory risk — any attempt to directly compete with card networks or banking infrastructure would invite intense regulatory scrutiny. The opening of Apple's NFC interface in 2025 suggests some regulatory pressure is successfully moderating Big Tech's platform leverage in payments.

The more asymmetric risk is platform dependency: when Shopify processes $248 billion through Shop Pay (via Stripe), or when Uber routes all its driver payments through a single PSP, the concentration of payment volume in a few mega-platform relationships creates binary revenue risk for PSPs. When Adyen lost Cash App processing in the US in 2025, it had a material impact on disclosed volume, despite robust performance in the underlying business — a sharp illustration of platform concentration risk.

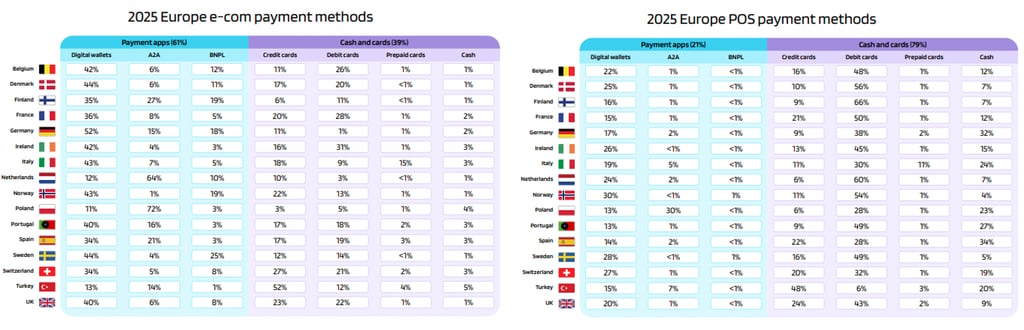

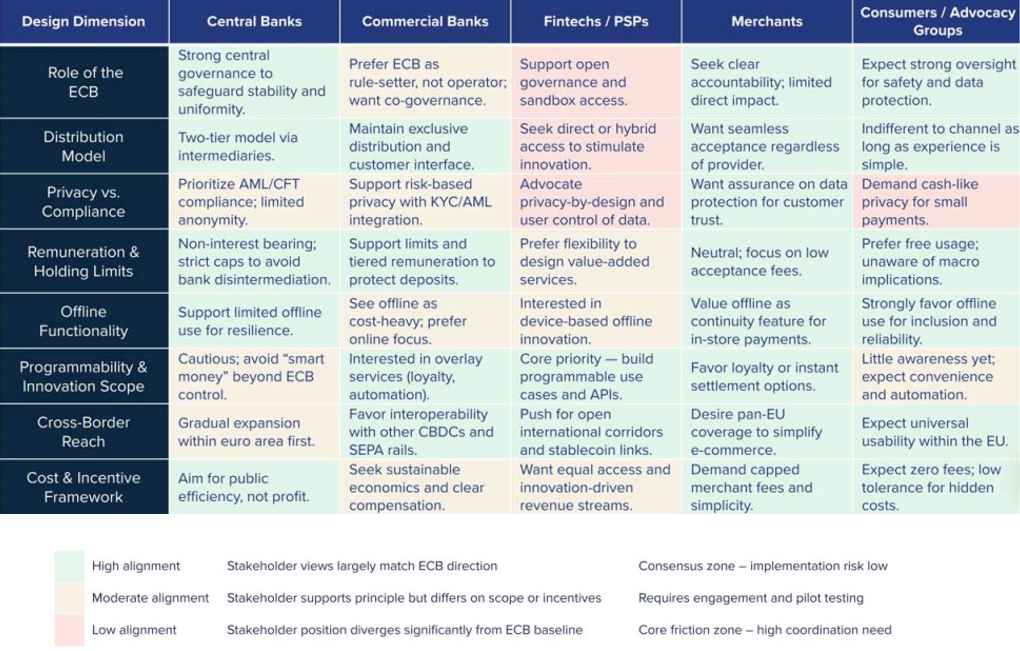

10. Europe Deep Dive: A Market at a Crossroads

Europe deserves dedicated attention as a distinct competitive theater — its regulatory environment, interchange caps, and sovereignty ambitions create dynamics that differ sharply from North America or Asia. European payments in 2025 is a market where technological ambition collides with regulatory constraint and political will.

Here is a Guest lecture by Piero Cipollone, Member of the Executive Board of the ECB, at the Frankfurt School of Finance & Management if you want to go in more detail.

10.1 The European Payments Sovereignty Agenda

European policymakers view the current payments landscape as a strategic vulnerability. The continent relies overwhelmingly on non-European infrastructure for its daily payment needs: Visa and Mastercard for card payments; Apple Pay and Google Pay for mobile wallet interactions; and increasingly, Stripe and Adyen (both founded in the US and Netherlands respectively, but operating global platforms) for merchant processing.

The ECB has expressed this concern directly: if European payment infrastructure were to be disrupted — through geopolitical conflict, US sanctions, or commercial disputes — Europe has limited ability to maintain its own payment systems. The European Payments Initiative (EPI) and its consumer wallet product Wero represent the continent's most serious attempt to build sovereign alternatives.

Wero — the digital wallet developed by a consortium of European banks under the European Payments Initiative — represents Europe's most serious attempt at payment sovereignty: reducing dependence on Visa, Mastercard, and American infrastructure providers. In 2025, Wero has made solid progress, adding PSPs including Airwallex, Unzer, PPRO, and Raiffeisen, and signing a dozen large merchants in France and Germany including Decathlon, Lidl, and Eventim.

The strategic logic is compelling: European banks collectively process enormous payment volumes but route them through American-owned networks, paying American companies billions in fees. A European wallet with European rails would retain that value in the region and reduce geopolitical dependence. The execution challenge is equally compelling: consumer adoption requires changing behavior deeply embedded around card usage, and merchant integration requires investment across a fragmented retail landscape.

10.2 The Winners and Losers in European Processing

The European PSP market is producing clear divergence between winners and losers:

Source: WorldPay global payment report

10.3 The SEPA Instant Mandate

The EU's mandate for all banks to support SEPA Instant Credit Transfers — with the transaction limit raised to €1 million in 2025 — is quietly building the infrastructure for A2A payment scale in Europe. As instant bank transfers become universal and interoperable across all euro-area bank accounts, the merchant case for accepting them (lower fees, instant settlement) will become more compelling. The missing piece remains consumer incentive: without rewards programs equivalent to card benefits, consumers have limited reason to choose bank transfer over a card that earns them airline miles.

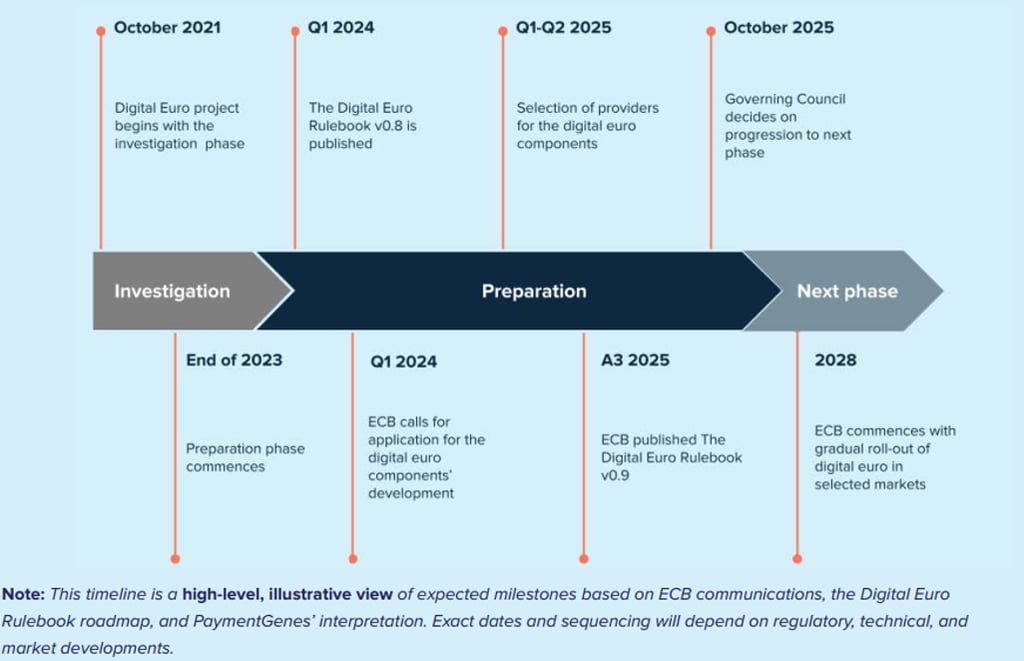

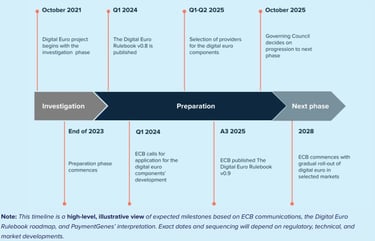

10.4 The Digital Euro: Set to Fundamentally Reshape Europe payment industry

Europe’s payments landscape is entering a decisive transformation. With the European Central

Bank’s October 2025 “go-decision”, the Digital Euro is moving from exploration to advancing

the technical work and continuing to support the legislative process. This marks a structural shift:

for the first time, the very form of money, long dominated by private-sector innovation, will be

redesigned through public policy intent.

Across all futures, one insight is clear: the Digital Euro will not replace the existing payment

ecosystem but reconfigure it.

For commercial banks, this shift brings both challenges and opportunities. As deposits risk

partial migration into central bank money, banks must evolve their role — moving not only from

custodians of balances to providers of digitaleuro services, but also to broader providers of

digital financial solutions such as embeddedfinance propositions, programmable payments,

and multi-asset wallet offerings.

For fintechs and PSPs, By offering API-accessible payment rails, the digital euro is intended to serve as public digital infrastructure, enabling private actors — including banks, fintechs, and PSPs — to build services on top of a trusted foundation. This mirrors how physical euro cash underpins the current financial system to banks that embrace open, API-driven collaboration models. A quote from Adyen CEO on the subject of the role of PSPs with the digital euro: “Adyen will operate as an ecosystem integrator. Our role will be to ensure that merchants can easily accept Digital Euro payments through a single, unified integration that covers all channels and countries. We will focus on simplifying complexity, optimizing conversion, managing risk, and enabling programmable capabilities.”

For merchants, lower acceptance costs and instant settlement are tangible benefits—but the value will depend on seamless integration and consumer trust. In mature digital markets such as the Netherlands or Finland, adoption will hinge on whether the Digital Euro adds resilience or privacy beyond what existing methods already provide.

If you want a more in-depth analysis on the subject I would advise reading PaymentGenes Consultancy Digital Euro report that goes more in-depth on the subject.

11. Industry Structure, Outlook & Investor Framework

11.1 The Coopetition Paradox

One of the most counterintuitive features of the payments industry is coopetition — the practice of simultaneously competing and cooperating with the same company. PayPal's payment orchestration product competes directly with Adyen, yet PayPal also routes some of its transactions through Adyen. Stripe's Shopify Payments product is the exclusive processor for the world's largest small-business e-commerce platform — but Shopify also sells Stripe's services on behalf of other e-commerce merchants, making Shopify both a customer and a distribution channel.

Large enterprise merchants almost always have multiple payment processors connected simultaneously. This is not waste — it is resilience. If one processor goes down (hardware failure, software bug, network outage), the merchant instantly routes all traffic through the backup. This means a PSP can be losing market share without losing any of its merchant logos — the merchant is still there, just routing less volume through that specific processor.

Lisa Ellis of MoffettNathanson described this in a conversation with Ben Thompson: it is 'almost as easy as turning a dial.' A merchant might run 80% of its volume through Adyen and 20% through Braintree, and if Adyen performs poorly one quarter, they simply turn the dial — without switching providers, signing new contracts, or any technical integration work.

In summary, it is an industry where winner-takes-all is structurally impossible because no enterprise wants to depend on a single processor.

11.2 The Winners

Stripe — The Private Giant

Stripe is the clearest winner in the modern payments era for now. It is private and rarely publishes detailed financials, but the available data is extraordinary: TPV of $1.9 trillion in 2025 (up 34% from the prior year), private valuation of $159 billion (more than 3× Fiserv's market cap), and dominant positioning across the AI economy's billing stack. Its acquisition of Metronome — the leading metered billing infrastructure provider — for approximately $1 billion in January 2026 positions it as the default billing engine for AI-native companies, which characteristically use consumption-based pricing that Stripe is now uniquely equipped to handle.

Adyen — The Publicly Listed Benchmark

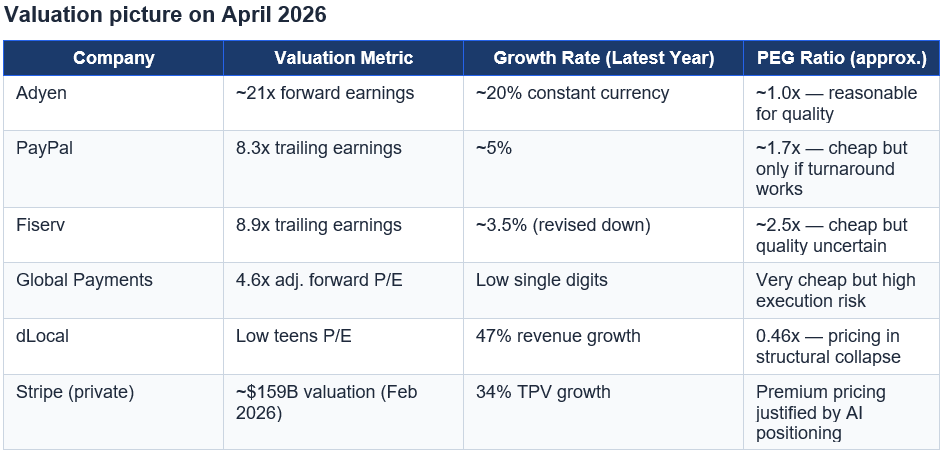

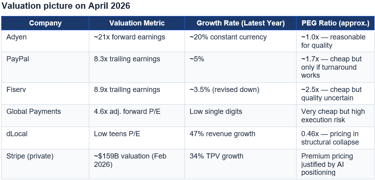

Adyen is the only publicly listed pure-play PSP of Stripe's caliber, and it is the benchmark for what a high-quality payment processing business looks like. Net revenue up 23% to €2 billion in its latest fiscal year, EBITDA margins approaching 50%, and a single global technology stack that can serve McDonald's in-store terminals in Germany and its online ordering in Japan on the same platform. Adyen's take rate actually expanded from 14.7 basis points to 17.1 basis points, demonstrating pricing power rather than compression.

Visa and Mastercard — Enduring Duopoly

11.3 The Challenged Incumbents

The contrast between the new generation of PSPs and the legacy processors built through acquisition is stark. In October 2025, Fiserv's stock crashed 44% in a single day after management slashed full-year guidance from $10.15 to $8.50 EPS and cut revenue growth expectations from 10% to 3.5%. The CEO attributed this to predecessors' "short-term decisions to cut costs and defer investment" — exactly the M&A integration trap that destroyed value across the legacy processing industry.

PayPal, Global Payments, and FIS have all underperformed their stated growth targets. Global Payments completed a transformational asset swap with FIS — where the jury is still out on whether it will create or destroy value. PayPal spent 2024 and 2025 promising a turnaround that has not yet materialized.

This generation of companies was built through consolidation in the 1990s and 2000s — buying up smaller acquirers and processors to achieve scale. The scale was real, but the technology integration was often incomplete. Running multiple acquired companies' technology stacks in parallel — instead of rebuilding on a single modern platform — created exactly the kind of brittle, expensive infrastructure that makes it impossible to respond quickly to market changes.

11.4 The New Challengers in specific markets

Below Stripe and Adyen sits a tier of emerging challengers that are gaining share in specific verticals or geographies:

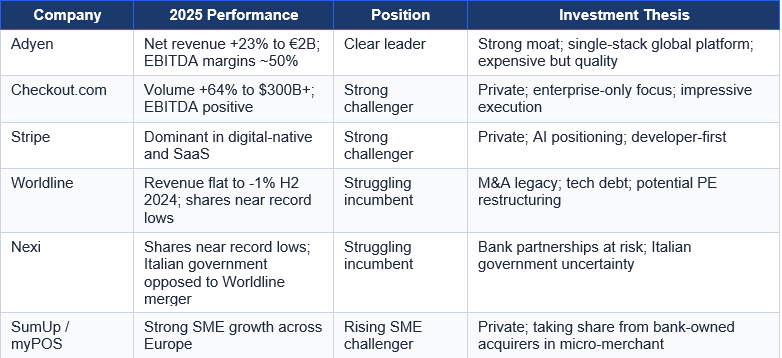

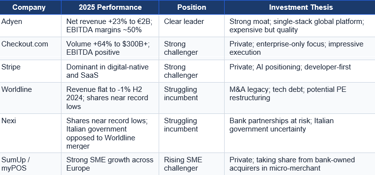

• Checkout.com: Processed over $300 billion in 2025 (volume up 64% YoY), exclusively focused on large enterprise merchants. Now EBITDA-positive without adjustments.

• dLocal: The leader in emerging market payment processing. TPV grew 60% to $40.8 billion in 2025, with net revenue retention of 162% — meaning existing merchants on average increased their payments volume through dLocal by 62% organically. Brazil is its highest-margin geography.

• Toast: Vertical SaaS for restaurants — deeply integrated into how restaurants manage their entire operation, making payments one feature of a broader software suite. Toast and Shopify represent companies that sit on top of PSPs, using payment processing as a revenue stream rather than a core identity.

• Shift4: Focused on high-transaction-volume verticals — stadiums, casinos, hotels, large restaurant chains. This vertical focus provides defensible pricing power that commodity processors lack.

11.5 The Structural Secular Tailwind

The structural tailwind is quite simple: the world is shifting from cash to electronic transactions, and this shift is far from complete. In 2024, cash still represents more than 40% of all global transactions by volume. In many emerging markets, it exceeds 70%. Every percentage point of share that moves from cash to digital creates more transaction volume, more fee revenue, and more data for payment processors.

This secular tailwind has been growing the industry for sixty years and has masked significant competitive failures. Companies built on poor technology, executed bad acquisitions, and accumulated technical debt — yet still grew revenues for decades because the rising tide of digital payments lifted every boat. The tide is still rising, but it is rising more slowly now (4% versus 12%), which is why the companies with genuine competitive advantages are finally separating from those that were merely riding the wave.

11.6 The Current Market Situation : A Sector in Re-Rating

This section addresses one of the most important questions for anyone considering investing in payments today: why has the sector performed so badly recently, and does that create an opportunity?

Critically, this is primarily a multiples compression story, not an earnings collapse. Shift4's EPS grew from $1.05 in FY2022 to an expected $5.32 in FY2025 — yet the stock is roughly flat over that period. DLocal's revenue grew 47% and net income grew 63% in FY2025; its stock is down 30% since 2024. The multiples have absorbed — and then some — all of the earnings growth.

Several forces are simultaneously weighing on the sector:

1. Fundamental Disappointment from the Largest Players

The biggest companies in payments — Fiserv, PayPal, Global Payments, and FIS — have fundamentally underperformed. Fiserv's 44% single-day crash was not a one-time shock; it was the culmination of years of deferred technology investment and M&A integration failures. When the bellwether companies in a sector all disappoint simultaneously, investor sentiment degrades across the entire sector — dragging down even well-performing names like Adyen and dLocal.

2. Macro Uncertainty

Softening consumer spending would hurt all payment processors, and the macro signals are increasingly concerning. Consumer sentiment fell to 47.6 in April 2026 — an all-time record low according to the University of Michigan survey. J.P. Morgan raised recession probability to 40–50%. One-year inflation expectations spiked to 4.8%, raising stagflation concerns.

3. Technology Disruption Fears

The structural disruption narratives — A2A taking share from cards, stablecoins building critical mass, AI agents routing around card networks — create uncertainty even when the near-term data does not support a crisis. Investors price in the possibility of structural deterioration before it has materially affected earnings, which explains why the sector trades at depressed multiples relative to earnings.

The Bull Case: A Sector Near a Bottom

PayPal at 8.3x earnings, Fiserv at 8.9x — these are historically low multiples for businesses with genuine competitive moats, strong free cash flow, and the ability to return capital through buybacks. The best companies in the sector (Adyen, dLocal, Stripe) are compounding earnings well. If the macro holds and the largest players stabilize, any catalyst could re-rate the sector. The companies are not broken — they are broken stocks.

The Bear Case: Structurally Lower Multiples Are Justified

McKinsey and BCG both project global payments revenue growth settling at 4–5% annually through 2029 — down from 12% at its peak. If this is accurate, then low multiples for legacy acquirers are not pessimism but accurate pricing. Three concurrent disruption vectors (A2A, stablecoins, CCCA/interchange regulation) are intensifying, not receding. Fiserv's 44% single-day crash is a reminder that valuation floors can break catastrophically when growth disappoints. 'Cheap' is not the same as 'bottoming.'

11.7 The Investment Framework: Segment-by-Segment Analysis

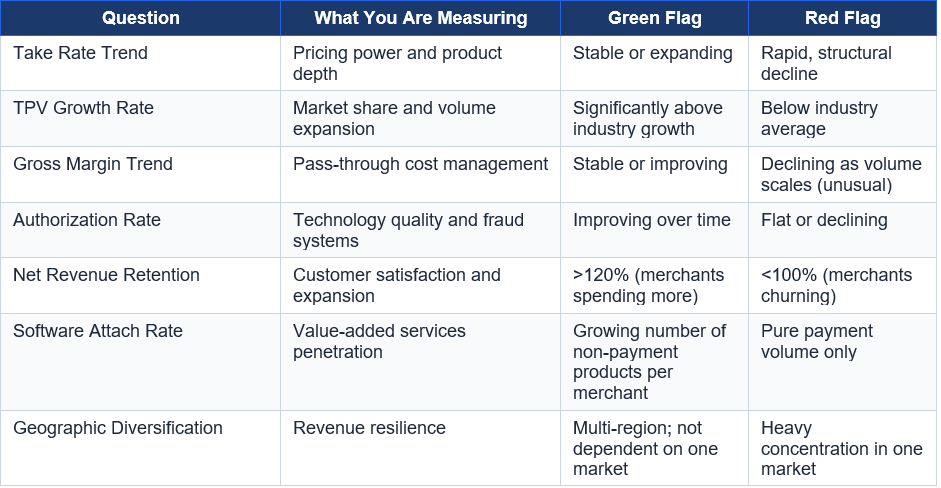

How to Evaluate a Payments Company

Before looking at specific segments, here is the analytical framework that applies across the industry. When evaluating any payments company, an investor should ask seven questions: what is the ...

Tier 1: Card Networks (Visa, Mastercard, American Express)

The card networks are the highest-quality businesses in the payments industry — arguably in all of financial services. They earn toll fees on every transaction that passes through their rails, bear no credit risk, and require minimal capital to grow. Visa's net profit margin consistently exceeds 50%.

The investment risk is real but slow-moving. A2A rail adoption and potential interchange regulation threaten the long-term revenue trajectory. The network's response — tokenization, value-added services, investing in the trust and fraud infrastructure that A2A still lacks — buys considerable time. For a long-term investor, the key question is whether the duopoly moat (which has survived 60 years) will survive another decade at current earnings power.

American Express is distinct: higher-margin, premium-positioned, with richer data. Its customer base skews higher-income, providing resilience in downturns. The business is more cyclical than Visa/Mastercard because AmEx bears credit risk, but its brand and data advantages are formidable.

Tier 2: Full-Stack PSPs (Stripe, Adyen)

These are the most attractive investment opportunities in the industry currently — offering the growth rates of technology companies with increasingly visible competitive moats in software depth and embedded finance. The key analytical question is whether their moats rest on processing (which is commoditized) or on the software layer above it (which has genuine switching costs).

Adyen's case: its single global technology stack is genuinely difficult to replicate. A competitor cannot easily offer Adyen's ability to handle in-store payments in Germany, online payments in Japan, and QR-code payments in Brazil through a single integration. The investment in this infrastructure took over a decade to build. Large multinational enterprises switching away from Adyen face enormous re-integration costs.

Stripe's case: its developer experience and API design created network effects among software engineers that have proven remarkably durable. More importantly, its positioning at the center of the AI economy's billing infrastructure — through its dominance of AI company billing and the Metronome acquisition — is creating a new moat that competitors will struggle to crack.

Tier 3: Legacy Processors (Fiserv, FIS, Global Payments, Worldpay)

These companies generate large, relatively stable revenues from long-term bank and merchant contracts. Their investment case rests on free cash flow generation and capital return (buybacks and dividends), not on growth. The risk is that deferred technology investment eventually becomes irreversible — not a gradual 5% annual market share loss, but a catastrophic client loss event when a large bank or retailer finally migrates to a more modern platform.

At 4–9x earnings, legacy processors may offer value. But investors must distinguish between companies where the technology debt is manageable (can be fixed with investment over 3–5 years) and those where it is structural (the entire platform must be replaced, which is nearly impossible without service disruption). Fiserv's October 2025 earnings shock was a warning: the market assumed stabilization; management revealed they had been borrowing from the future. Now that it has gone much lower it might present opportunities for risk takers but investors must remain careful.

Tier 4: Emerging Market Specialists (dLocal, Mercado Pago, Paytm)

The highest-risk, highest-reward segment. These companies operate in markets where digitization is still in its early stages and the runway for growth is enormous. dLocal's 60% TPV growth in 2025 with 162% net revenue retention speaks to the scale of the opportunity — existing merchants are growing dramatically on the platform without dLocal needing to acquire new customers.

But the risks are real: currency volatility, regulatory uncertainty, take rate compression as enterprise clients scale, and competitive pressure from both global PSPs (Stripe entering EM) and local competitors.

11.8 Key metrics to monitor for the industry

An investor tracking the payments industry should watch these leading indicators on a quarterly basis:

• Total Payment Volume (TPV) growth rate — the primary revenue driver; above-market growth signals share gains

• Net take rate trend — the margin indicator; watch for structural vs. cyclical compression

• Authorization rate by merchant — improving rates signal technology quality; declining rates signal problems

• A2A transaction share of total digital payments, by geography — the structural disruption tracker

• Net Revenue Retention (NRR) — >120% is excellent; <100% is a serious red flag

• US Credit Card Competition Act — legislative calendar and probability updates

• Stablecoin daily settlement volumes — the nascent disruption proxy

• Fiserv/PayPal quarterly earnings — the bellwether signal for legacy sector stability

• Visa/Mastercard quarterly earnings — helps with having insight on where the industry is going

12. Conclusion