Beyond the S&P 500: Why 'Just Buy the Index' Isn't the Whole Story

STOCK

5/23/202613 min read

Let's analyze the argument that "passive" investments like the S&P 500 are always better than mutual funds and stock picking, and let's investigate the idea that stock picking may be the better decision for people willing to spend some time and effort.

ETFs

An ETF is a basket of financial products that trades on an exchange. They are structured to track anything from the price of gold to a certain industry's bonds or stocks, or to track the performance of a country. The most famous ETFs track the index called the S&P 500, which follows the stock performance of 500 leading companies listed on stock exchanges in the United States.[1]

One big advantage of ETFs is the ability to get broad exposure with very low expense ratios while only holding one position in your portfolio.

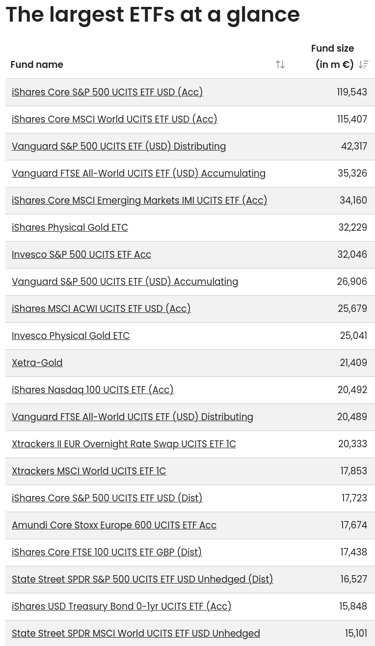

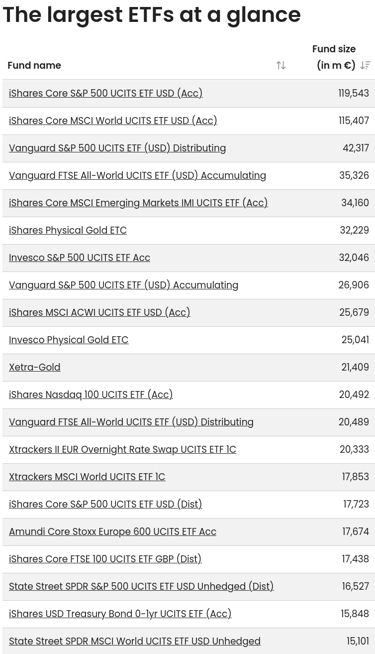

There are a wide variety of ETFs; however, people should be mindful that many of them greatly overlap and track similar stocks. For example, SPY, VOO, and IVV all track the same index, the S&P 500. Others like QQQ and VTI track different indices but overlap with the S&P 500. So buying QQQ on top of VOO won't meaningfully diversify your portfolio, as true diversification also requires exposure across different asset classes such as bonds, real estate, or international stocks.

Given that the current argument is that buying S&P 500 or world index funds will be more profitable compared to actively managed mutual funds or picking your own stocks, I will be mainly focusing on the S&P 500.

Historically the S&P 500 has performed very well, with an average return of 9 to 10% per year over the last 100 years or so (worth noting: this only applies to US stocks, European markets didn't come close, and Japanese markets performed even worse). This is also a survivorship biase, the US happened to be the dominant 20th-century economy, which one reason why it’s stocks market has performed so well. Betting on that continuing isn't guaranteed.

This US growth is also not uniform. Tere have been periods where stock returns were flat for very long stretches of time. For example: 22 years from 1898 to 1920, 25 years from 1929 to 1954, 17 years from 1965 to 1982, and more recently 12 years from 2000 to 2012. During those stagnant periods there have also been severe crashes, such as the 86% drop from 1929 to 1932, the 50% drop after the 2000 dot-com bubble, and a similar decline during the financial crisis in 2008.

So even though the past 100 years have been very lucrative for the S&P 500, timing matters , depending on your investment timeline, especially if it is short, investing in the stock market may not have been a good idea.

Past returns don't guarantee any future returns, so let's deep dive into the reasons for this growth and whether those reasons are still valid today. There are 3 important drivers of S&P 500 growth over the past 100 years or so

Earning growth

Companies have been raising profits through increased efficiency: electrification, industrialization, and the PC and internet revolution. Workers have become more productive, which has driven company profits higher.

While it's impossible to predict future growth, here are a couple of opportunities and challenges for the coming decade:

AI has the potential to greatly increase companies' profitability by lowering costs and increasing output. However, the short-term consequences could include higher unemployment and economic hardship. An overhype of the technology, similar to the dot-com bubble, could create economic hardship in the short term even if the technology ultimately increases efficiency in the long run.

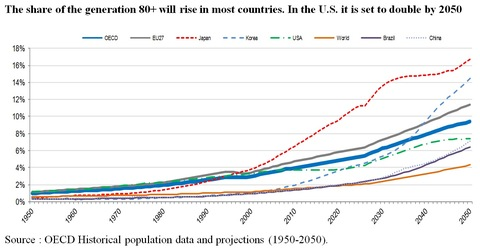

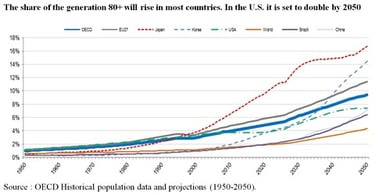

An aging population and shrinking active workforce would negatively impact productivity. However, this impact is forecasted to be lower in the USA than the OECD average, which would be relatively favorable for the S&P 500 compared to other indices or mutual funds based in other geographical areas.

This part can take a whole other chapter, here is another interesting link if you’d like to research this further.

https://www.esm.europa.eu/ESM-briefs/population-ageing-and-productivity-innovation-channel

Climate change: extreme weather event such as drought, floods, hurricane and wildfire could have a negative impact on economic growth

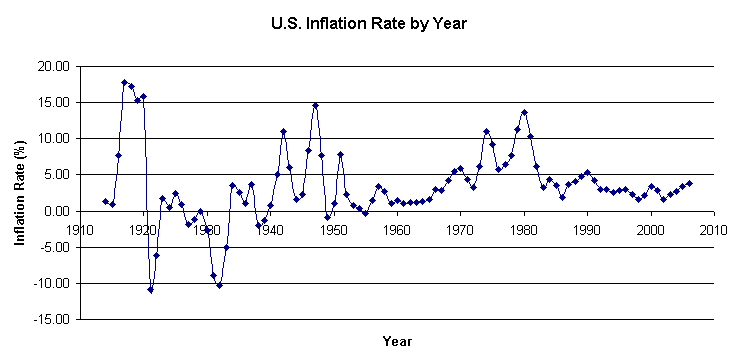

Inflation:

High inflation can be detrimental to the economy and hence the stock market, as it reduces companies' profitability. To combat inflation, central banks are forced to raise interest rates, which decreases companies' profitability even further.

Low inflation on the other hand has pushed the stock market higher in nominal terms, but this can be misleading. A weaker dollar means that the S&P 500 hasn't necessarily gained real value, the dollar has simply lost purchasing power, making the S&P 500 appear more expensive than it actually is.

h

ttps://www.google.com/url?sa=t&source=web&rct=j&url=https%3A%2F%2Fcommons.wikimedia.org%2Fwiki%2FFile%3AUS-Inflation-by-year.png&ved=0CBYQjRxqFwoTCIj44_qOnZQDFQAAAAAdAAAAABBQ&opi=89978449

More money into Stocks and SnP

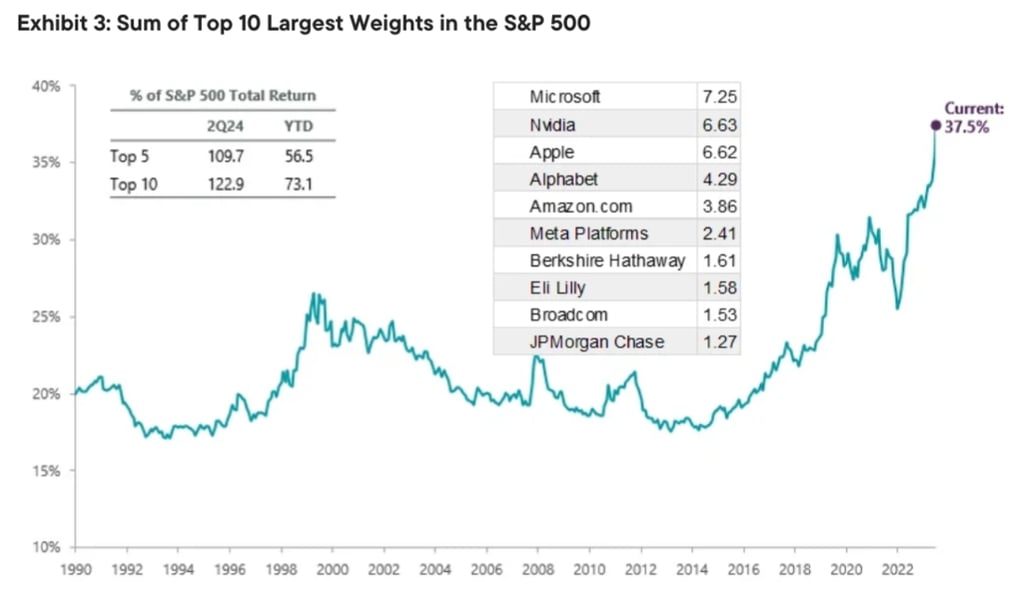

Over the past 40 years, the declining yield of the risk-free rate has pushed investors away from bonds and into stocks to get better returns. This is true for stocks in general, with an even bigger inflow into a handful of ETFs due to the mass adoption of 401(k) plans from the 1980s onward. More money flowing into the stock market has pushed stocks even higher and faster than the real economy, as illustrated by the S&P 500's price-to-earnings ratio sitting well above its historical average, and the market cap to GDP ratio — known as the Buffett Indicator — reaching levels not seen since the dot-com bubble. The worry is that when Baby Boomers draw down their savings for retirement, it may crash the stock market for a prolonged period. This is known as the asset meltdown hypothesis.[2] However, this hypothesis is contested, as many economists argue that younger generations and foreign investors will absorb the selling pressure.

This could create what Barron's magazine calls a self-reinforcing feedback loop, where the success of indexing bolsters the performance of the index itself, which in turn promotes more indexing. This mechanism works because index funds must buy stocks in proportion to their market cap, meaning that inflows mechanically bid up the largest constituents of the index. It does suggest the potential for a reverse trend. When the market trend reverses, broad index funds will not seem so attractive. The selling will then adversely affect the performance of index investors and further exacerbate the rush to the exits, which could create a decline and a long period of stagnation for the market.

As Profesor Lu Zheng is putting: “Basically, what we see happening is large firms keep getting bigger, and their stock prices keep going higher. One day there might be a reversal of this trend, but for now, our study shows a rise of mega-firms in large concentrations.” As of 2023, passively managed index funds accounted for48% of the total assets investment companies managed in the United States [3]

Change of structure over time

Even though the SnP is called “passive” investment , its methodology has changed over time with the following big structural changes:

1926 — The S&P 90 Before the 500, there was a modest 90-stock index split between industrials, railroads, and utilities. [4]

1957 — Birth of the 500 On March 4th, the index expanded to 500 stocks, but still ran on a fixed blueprint: 425 industrials, 60 utilities, 15 railroads.[4]

1976 — Adding finance industry Financial stocks were added for the first time, reshuffling the slots to 400 industrials, 40 utilities, 40 financials, 20 transportation. Still a quota system, just a more modern one.[4]

1988 — Letting go of the quota The fixed model was scrapped entirely. Sector weights would now follow the actual economy rather than a predetermined grid.[4]

1999 — Only profitable companies Amid dot-com mania, S&P introduced a profitability rule: positive earnings in the most recent quarter, and over the prior four quarters combined. A quiet but meaningful line in the sand. [4]

2005 — Only trading shares S&P switched to float-adjusted weighting. Locked-up founder or insider shares no longer inflated a company's index weight. Only shares genuinely available to public investors counted.

As the time of writing there is a potential big upcoming change in methodology:

“S&P Dow Jones Indices has announced a formal review of eligibility requirements for the S&P 500, examining whether megacap companies should face less stringent entry criteria and be eligible for fast-track inclusion” [5] This would impact the IPO of spaceX, OpenAI, Anthropic etc… This will likely make the index more volatile and increase the companies turnover in the index.

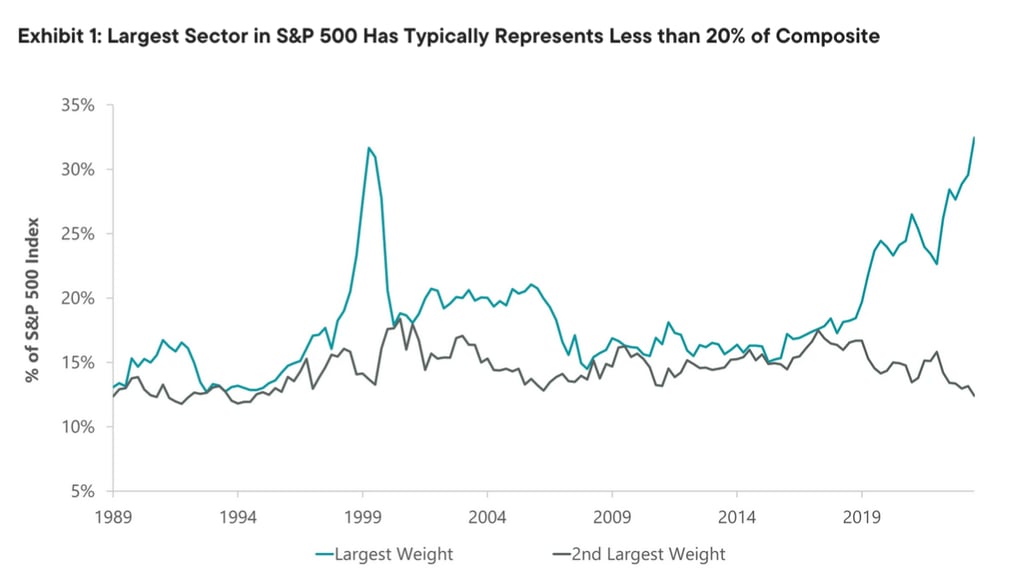

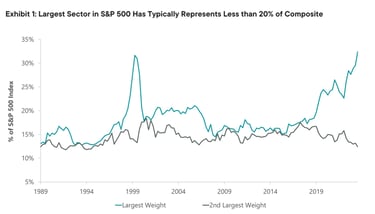

The composition of the index evolves over time as some stocks gain in valuation and hence have a bigger weight in the index while losing stocks get a smaller weight. This structure is great for maintaining a composition that is diversified and up to date. However, it can create over-concentration in a few industries and stocks, as seen during the dot-com bubble and also today.

As of today, the top 10 companies in the S&P 500 account for 39% of the total index. [6] Three technology companies: Apple, Microsoft, and Nvidia, represent 20.5% of the S&P 500. [7] People are more exposed to a smaller number of stocks than they realize.

Even in scenarios where AI is set to revolutionize the workplace as computers did, it doesn’t exclude the possibility of negative stock returns or no return for a long time.

Lastly, increased demand for some stocks can stem from popularity rather than the actual performance of the underlying business. Some companies, like Tesla with a P/E of 360 or Palentir with a P/E of 215 clearly look overvalued.

Active Mutual Funds

Mutual funds are an investment funds managed by a professional portfolio manager. They are called actively managed funds.

A new study from S&P shows that roughly 90% of active public equity fund managers underperform their index. Most publicly listed companies lose stock value over a lifetime. Moreover “the number of high-performing firms that explain half of the net wealth

creation since 1926 decreased from ninety as of 2016 to eight-three as of 2019 and to seventy-

two as of 2022.” [8]

“Four out of every seven common stocks [...] since 1926 have lifetime buy-and-hold returns less than one-month Treasuries.”[9]

This is why it is hard to make money, by selecting a handful of stocks and design a diversified porfolio you would not only be unlikely to beat a risk free rate but also to lose money.

In one study made by Anton, Miguel and Cohen, Randolph B. and Polk, Christopher, named “Best Ideas” in April 21, 2021, the conclusion was that one of the biggest reasons fund managers underperform the market is that they have too much stock in their portfolios.

The average number of positions is 165 stocks.

Generally, they have 10 to 20 convictions and the rest of the stocks are there to complete the portfolio.

And with so much positions it’s nearly impossible to beat the market so if you put on top of that fees. You start to come to understand the issue.

In another study they also took out 75% of funds who underperforms the market. And in those 25% that have true convictions. Generally, the 1st convictions are 10% of the portfolio.

The 5 first represents 20-25%.

The question is : Did those strongest conviction of those funds beat the US market ?

And the answer is yes, they actually did perform better than the market from 2,8 to 4,8% per year.

So the ideas with the biggest convictions are generally good ideas, but how come they underperform the market then ?

Decreasing return to scale

As the fund is getting bigger, manager who once found alpha in small- or mid-cap stocks may be forced to migrate toward large-caps simply because those are the only markets liquid enough to absorb the fund's trades without self-defeating price pressure.

The result is that a mutual fund's past performance , often built when the fund was smaller and more nimble, can become structurally unrepeatable once success attracts more capital. [10]

Fee and fund structure

short term thinking, quarter to quarter reports

High fees

Fee structure is usually 2 – 20

The fee structure is not aligned with client’s interest. There an incentive for those funds to try managing as much money as possible instead of creating good return as they still make 2% of the money with no consequence. If they happen to win money, they get 20% of the profit. This is a very high fee if a fund doesn’t outperform the stock market by a decent margin.

Funds have a short term thinking with a time frame ranging from a quarter to a year because bonuses and performance review are on those basis but also from client’s pressure.

Bound by client’s desire

Pressure to retain clients. Clients frequently replace the worst-performing managers.

Even if they have good analysis, fund managers are bound by cash flows. When lots of savers want to pull their money out, the managers must sell assets quickly; even if they believe it’s a bad time to do so. And the reverse is also true: when money pours into funds, managers are forced to buy; even if prices are too high. So in reality, money flows in and out of the market not based on smart timing, but based on emotional or poorly informed decisions by savers.

To attract more investors funds are incentivized to invest in asset class or stocks they don’t have a conviction in but in what clients want to invest in. Fund managers also don’t really to stand out too much to competition in term of positions with the fear that people clients would leave if they don’t agree with those

Stock Picking

You may have heard statistics that most individual stock pickers lose money. However, most statistics do not differentiate between people investing and speculating. Speculating often uses complex structures like options and futures, which were primarily designed as a way to hedge risks for businesses and facilitate commerce. It is very different from a Buffett-style investment of choosing quality companies at a fair price.

For example, one study analysing individuals between 2013 and 2015 in the Brazilian equity market found that 97% of all individuals who persisted for more than 300 days lost money. Only 1.1% earned more than the Brazilian minimum wage and only 0.5% earned more than the initial salary of a bank teller — all with great risk. [12] However, we can see in the paper that those people took part in speculation and not investment, by using futures and options contracts. I also couldn't find any study differentiating the type of investor. Many retail investors are likely doing it for fun or entertainment, without proper extensive research or training. One study found that 26% of retail investors use social media for their investment ideas, answering "a great deal" or "somewhat" to the question of how much they rely on "social media groups or message boards where people post investment ideas" when making investment decisions. [13]

Another study found that: “skillful investors tend to outperform the market, even without inside information.” [14]

Anecdotally, I've seen even most investors from a finance background (risk analysts, commodity traders, trade finance…) buying stocks without even looking at their financials, relying purely on news. A very good company at an overvalued price is a bad investment, no matter how good the company is.

“the most active traders perform worse than less active traders even on a gross excess return basis” My explanation would be that most active traders tend to speculate a bit more than last active one who might be more focusing on value investing.

“retail investors present in the market for a longer period of time and trading more actively outperform the other investors” This is likely because people learn from their mistake and improve their skill over time [15]

Now that we've covered that most fund managers lose money because of external factors an less about their top stocks selection, and that a large portion of retail investors lose money through speculation or insufficient research (even though hard to put an actual percentage on it), let's look at the advantages retail investors have over hedge funds:

Most major money management firms consider only large-capitalisation securities for investment. These institutions cannot justify analyzing small and medium-sized companies in which only modest amounts could ever be invested.

Small volumes won't move the market, and won't require slowly buying in to prevent price movement.

You face no pressure, as the manager of your own money, to perform in the short term. You can sit and wait patiently and do absolutely nothing for months, if not years, until a fantastic opportunity presents itself. That is a better position to be in if you want to make good, reliable returns over a long period of time.

You don’t need to over diversify your portfolio and only owning 10-15 stocks where you really have a conviction.

Your smaller investment size gives you access to opportunities that wouldn't move the needle for big firms, and allows you to be more agile in entering and exiting positions.

References

[1] “Investopedia ETF.” [Online]. Available: https://www.investopedia.com/terms/e/etf.asp

[2] “Who will pay for 100 million boomer pensions?” [Money and macro]. Available: https://www.youtube.com/watch?v=uqSwRHc-1MQ&t=802s

[3] “Dominance of passive investing”, [Online]. Available: https://merage.uci.edu/news/2024/10/The-Dominance-of-Passive-Investing-and-Its-Effect-on-Financial-Markets.html

[4] “History of the SnP”, [Online]. Available: https://awealthofcommonsense.com/2025/08/a-short-history-of-the-sp-500/

[5] “upcoming potential change sp500”, [Online]. Available: https://www.tradingview.com/news/forexlive:ebe364f89094b:0-s-p-500-considers-fast-track-entry-rules-as-spacex-openai-and-anthropic-eye-ipos/

[6] “snp review,” franklintemple. [Online]. Available: https://www.franklintempleton.lu/articles/2024/clearbridge-investments/clearbridge-snp-index

[7] “slickcharts - snp composition.” [Online]. Available: https://www.slickcharts.com/sp500

[8] “Active fund underperformed”, [Online]. Available: https://www.spglobal.com/spdji/en/spiva/article/spiva-global/

[9] Hendrik Bessembinder, “Do Stocks Outperform Treasury Bills?”, [Online]. Available: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2900447

[10] “active manager skills”, [Online]. Available: https://www.chicagobooth.edu/review/why-active-managers-have-trouble-keeping-up-with-the-pack

[11] A. F. David Kabiller, “Buffett’s Alpha”, [Online]. Available: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3197185

[12] Chague, Fernando and De-Losso, Rodrigo and Giovannetti, Bruno, “Day Trading for a Living?,” Jun. 2020, [Online]. Available: https://ssrn.com/abstract=3423101

[13] K. J. K. Sarah Green, “Finfluencer Followers and Social Media Scrollers:”, [Online]. Available: https://finrafoundation.org/sites/finrafoundation/files/2026-03/FINRA_Foundation_Research_Brief_Social_Media_Finfluencers.pdf

[14] Joshua D. Coval, David Hirshleifer and Tyler Shumway, “Can Individual Investors Beat the Market?,” Jan. 2002, [Online]. Available: https://www.bus.umich.edu/pdf/mitsui/nttdocs/coval-shumway2.pdf

[15] Urbi Garay, Fredy Pulga, “The performance of retail investors, trading intensity and time in the market: evidence from an emerging stock market”, [Online]. Available: https://pmc.ncbi.nlm.nih.gov/articles/PMC8695249/

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.