ASML Stock Q4 2024 + CHECKLIST

Analysis into ASML Q4 2024 earnings + checklist

STOCKSEMICONDUCTORQUARTERLY EARNINGS

Rafael CARRARA

2/9/20269 min read

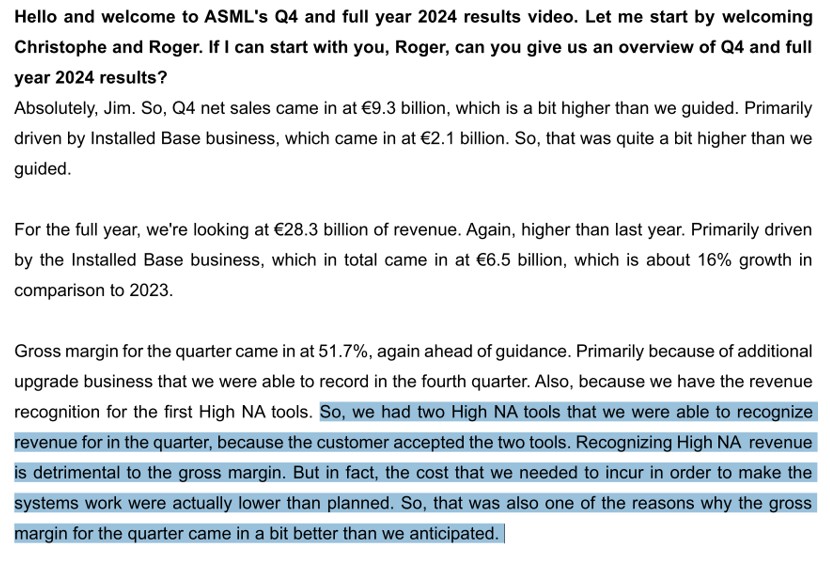

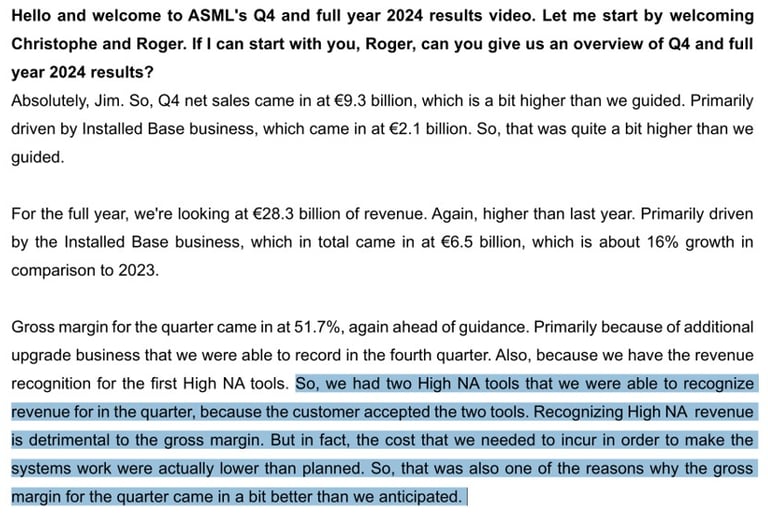

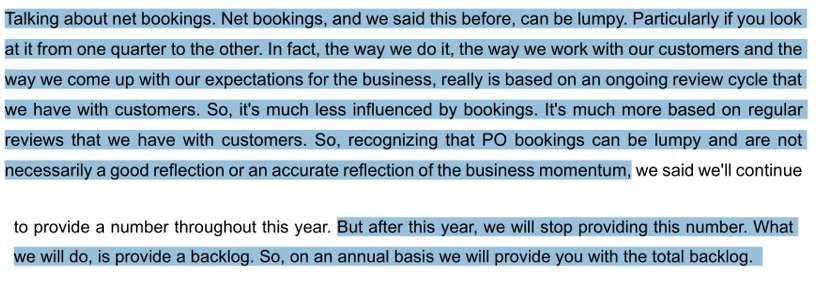

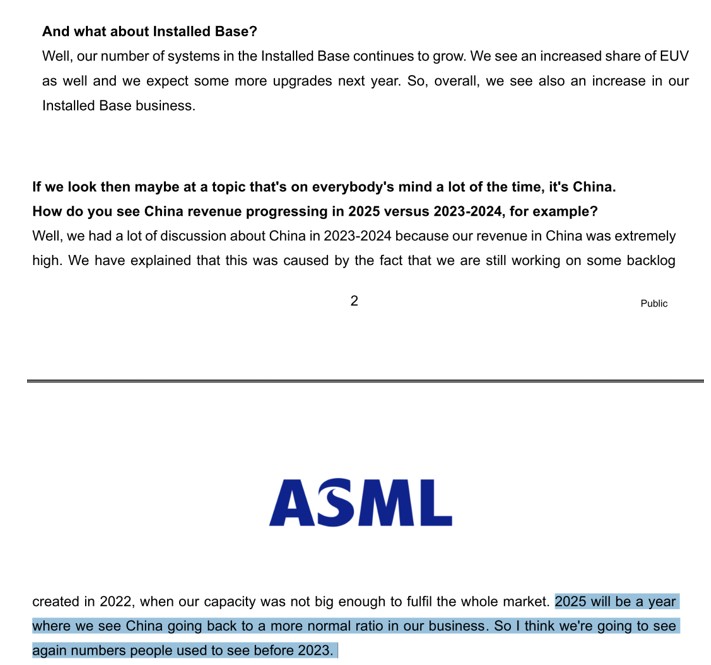

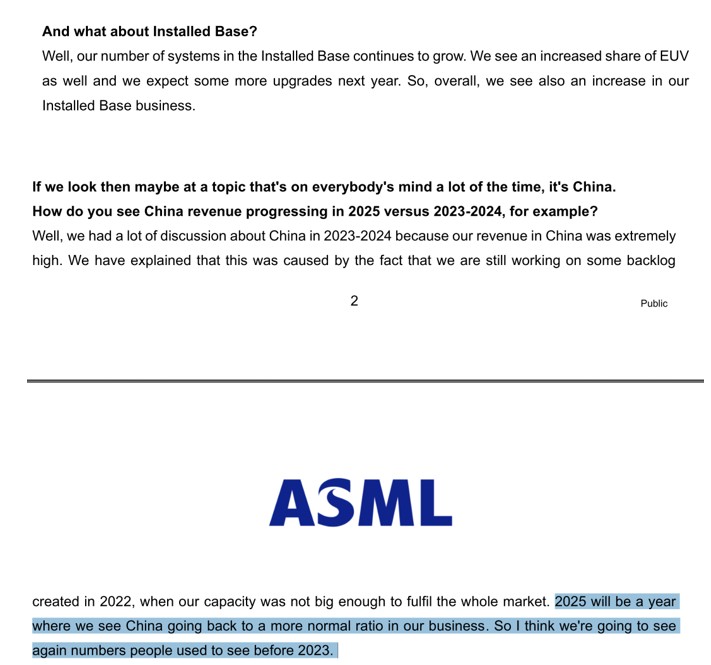

Earning call transcript

2024 Q4

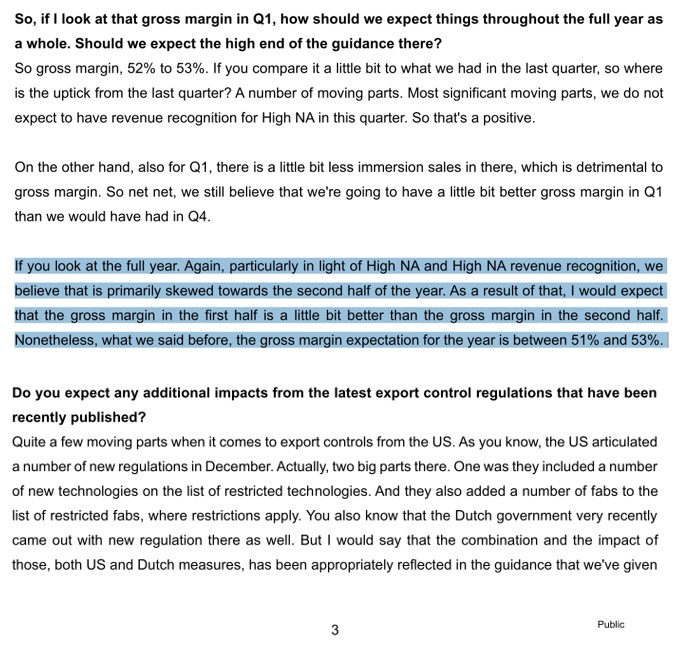

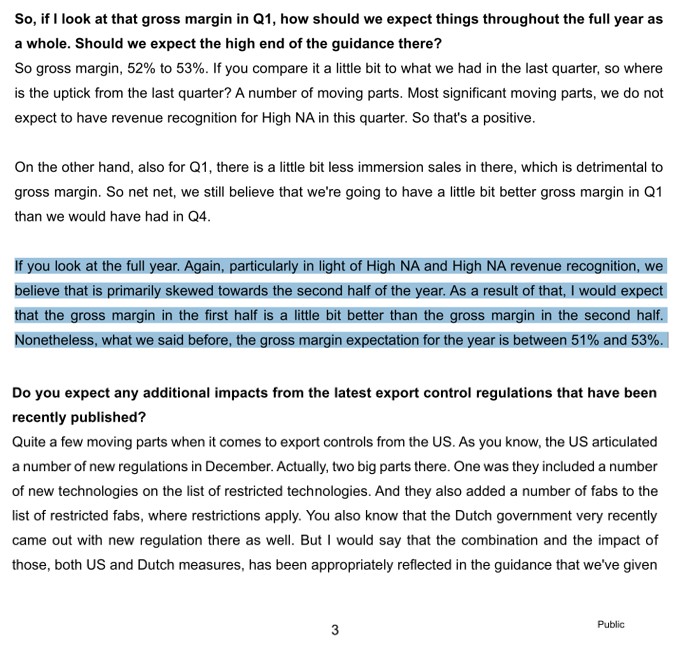

The Backlog number can be lumpy so they will change and provide the number for the year. I’m okay with the change but it is good to remember that as the machines are a big sum of money, particularly High NA could have big jumps in quarter results and changes in gross margin.

Just Backlog for the year represent 36 billion euros, with a 28% net margin ==> 10 Bn euros net profit

247 Bn euros market cap ==> makes it a 24,7 PE at the end of the year if they attain the numbers from a 33 PE right now.

On their guidance they seem to have been more conservative than what they have on their backlog in case of cancellations of order probably, so let’s see what happens with the lower and higher part of their guidance range.

High guidance assumption: 35 billion euros, with a 28% net margin ==> 9.8 Bn euros net profit

247 Bn euros market cap ==> makes it a 25.2 PE at the end of the year if they attain the numbers from a 33 PE right now. Based on current market cap

Low guidance assumption: 30 billion euros, with a 28% net margin ==> 8.4 Bn euros net profit

247 Bn euros market cap ==> makes it a 29 PE at the end of the year if they attain the numbers from a 33 PE right now. Based on current market cap

We will probably see a big decrease in China’s share of revenue geographically next year. Which I consider a good thing as it reduces the risk of Impact because of regulation on profit But if that share is picked up by Taiwan then the geopolitical risk is still there.

They already took into account the impact of regulation into their guidance the difference between backlog and the guidance comes probably partially from this.

Will have to see the Impact of E-beam products on the numbers though the margin will probably be lower than the other equipments as they face competition from KLA that dominates the market.

We might see some buyback this year as they have quite a bit of cash on the side. And prices are attractive at those level I believe. And they have a good history of when they do the buybacks. To look froward to as that would be a positive signal.

Again based on their guidance :

1) High guidance assumption : in 2030, 60 Bn euros ==> let’s say a 30% net margin to be a bit aggressive, that makes 18 Bn euros in net profit, Let’s say that there is exuberance an a PE ratio 40. That makes a price in 2030 a market cap of 720 Bn euros compared to 247 today. So, a 3X on the high part of their guidance in 5 years. Which makes a 25% potential yearly return.

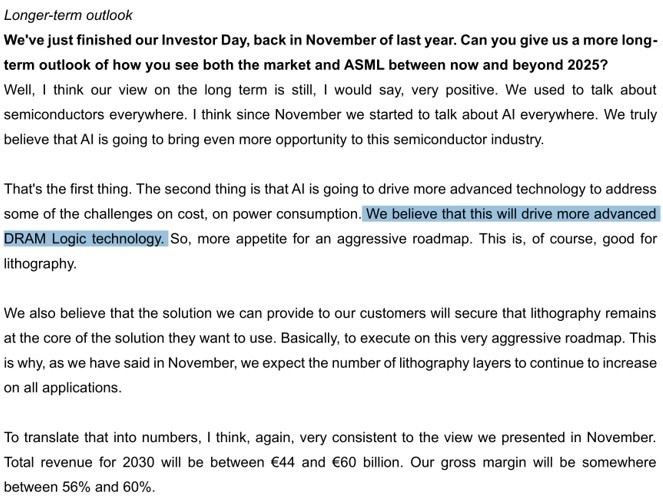

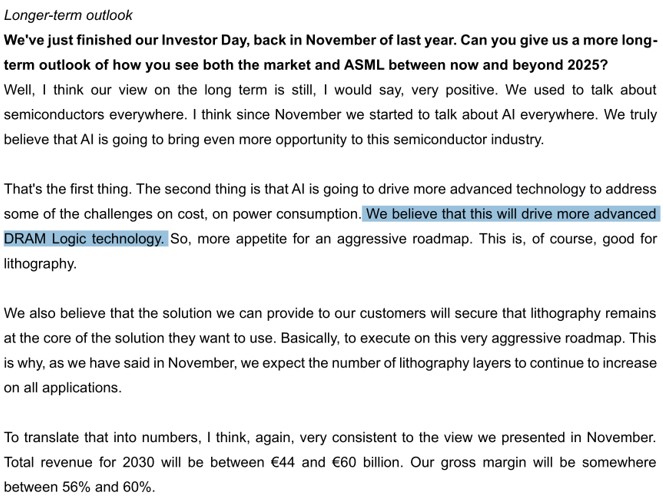

2) Low guidance assumption : in 2030, 44Bn euros ==> let’s say a 27% net profit margin. That makes 11.9 Bn euros in profit, let’s say with a PE of 30. That makes a market cap of 356.4 Bn euros compared to 247 today. Which makes a +50% in 5 years. Which makes a 8.5% yearly return

3) My Bad case assumption so that I have a margin of safety : In 2030, Let’s say they make 40 Bn euros ==> let’s say they have a net margin of 26%, that makes 10.4 Bn euros net profit and have a PE ratio of 25 that makes a 260 Bn euro market cap compared to 247 Bn euros today. So still a 5% increase based on quite bad assumption in 5 years. 1% yearly return, which is quite bad but still not a loss of capital based on quite bad assumptions.

ASML has a business and a Moat that gives them a good visibility on what their number are going to be, which further increase the margin of safety.

For me at those prices, ASML is totally worth it. And there is still a chance, though slim, that they beat their high guidance and there is even more exuberance.

But yeah, it is one where if the price changes significantly and the risk/reward ratio change as a result, it wouldn’t be a bad Idea to diminish the position if there are better opportunities elsewhere. And come back when the risk/ratio is good as it is today.

Again based on their guidance :

1) High guidance assumption : in 2030, 60 Bn euros ==> let’s say a 30% net margin to be a bit aggressive, that makes 18 Bn euros in net profit, Let’s say that there is exuberance an a PE ratio 40. That makes a price in 2030 a market cap of 720 Bn euros compared to 247 today. So, a 3X on the high part of their guidance in 5 years. Which makes a 25% potential yearly return.

2) Low guidance assumption : in 2030, 44Bn euros ==> let’s say a 27% net profit margin. That makes 11.9 Bn euros in profit, let’s say with a PE of 30. That makes a market cap of 356.4 Bn euros compared to 247 today. Which makes a +50% in 5 years. Which makes a 8.5% yearly return

3) My Bad case assumption so that I have a margin of safety : In 2030, Let’s say they make 40 Bn euros ==> let’s say they have a net margin of 26%, that makes 10.4 Bn euros net profit and have a PE ratio of 25 that makes a 260 Bn euro market cap compared to 247 Bn euros today. So still a 5% increase based on quite bad assumption in 5 years. 1% yearly return, which is quite bad but still not a loss of capital based on quite bad assumptions.

ASML has a business and a Moat that gives them a good visibility on what their number are going to be, which further increase the margin of safety.

For me at those prices, ASML is totally worth it. And there is still a chance, though slim, that they beat their high guidance and there is even more exuberance.

But yeah, it is one where if the price changes significantly and the risk/reward ratio change as a result, it wouldn’t be a bad Idea to diminish the position if there are better opportunities elsewhere. And come back when the risk/ratio is good as it is today.

CHECKLIST

-Does it responds to the criterias ?

Yes

If not, why ?

-Is there something better ? (competitors or other)

Haven’t found yet but I am looking through the semi-conductor industry and will compare the opportunity with ASML, if it is better I must be agnostic and change the investment.

-Is the company diversified in products and suppliers?

Yes it is diversified in product, but there numbers depend a lot on their EUV dominance. Though they have multiple clients they have a few that represents quite a big part of the command as they are so expensive few players can afford them. They have multiple suppliers but ZWEISS is a critical supplier for them, and in the US there are special components that they need that come from there.

-What is its sensibility to the economy ?

It is sensitive to it as the semi-conductor industry is cyclical and depend on the demand for chips.

-Regulatory risk ?

Yes there are regulatory and geopolitical risk that already happened in 2023 and 2024

-country risk ?

There is one but I would say it’s more geopolitical than specific to the country.

-Disruption risk ?

There is a risk but not for the immediate future (next 5-7 years)

-Correlated to another line in the portfolio ?

Not correlated

-What is the style of the company ? (growth, stalwart, cyclical, turnaround, quality, …)

Growth/cyclical

-What is the best support to buy the stock ?

PEA

-What Is the liquidity of the shares ?

very liquid

- What is the best class of share, best currency, best market ?

Euro, on euronext.

-Constitution of the board ?

No issue on the constitution of the board.

- When there was big drops, why did those happen ?

Too much growth expectations that didn’t materialized, as they were hit by the cycliclity of the semi-conductor industry.

- What are the margins ?

Very high margin, 28% net and 51% gross

A Small note :

Why is there a shortage of Nvidia GPUs while ASML is struggling to sell its production machines?

Indeed, it is quite strange to observe a shortage of Nvidia GPUs while ASML's results are poor, showing lower-than-expected demand for its EUV machines.

These machines are precisely used to etch this type of chip, so why this "double narrative"?

The shortage does not affect AI chips

There are several explanations for this.

Let's start with the first: the issue is not so much related to EUV lithography capacity but rather to the availability of small auxiliary components.

For example, to manufacture 51.2T switches (Broadcom’s latest high-end switches), a very specific glass component is required, which is produced by a single Japanese manufacturer that is currently out of stock.

Nvidia GPUs are made up of hundreds of small components, so you can probably already see where the problem lies…

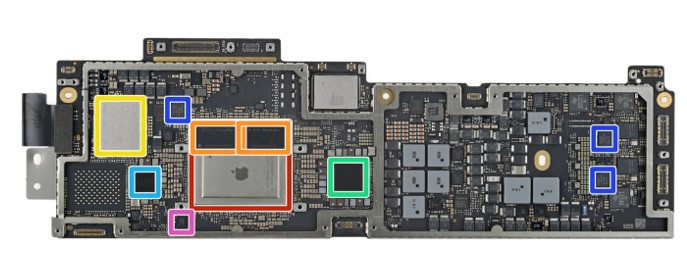

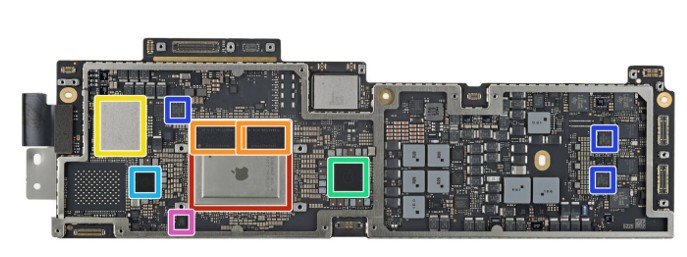

to give a more visual example, here is a MacBook Air motherboard.

In red, you can see the processor, the key component that is precisely etched using EUV machines.

In orange, there's the RAM, also known as memory.

In yellow, the hard drive.

In dark blue and pink, another type of memory.

The rest consists of what we call interface components.

In reality, many of these components don’t need to be etched with ASML’s EUV machines.

These machines are expensive and are reserved for components that require extreme precision.

Here, interface components simply serve as a bridge between two major components. For example, a USB controller is always needed to connect your USB stick to the processor’s ports so they can communicate.

And now you’re probably starting to see the problem.

A single supply chain issue for one of these components can delay the entire production process, even though it has nothing to do with EUV manufacturing capacity.

EUV machines are not only used for AI chips

Another major issue: EUV machines aren’t exclusively used for AI chips.

For instance, the automotive industry relies on them for certain components. And as you may have noticed, this sector isn’t exactly booming right now.

Demand for chips in the automotive industry (and to a lesser extent, in personal computing) is declining, freeing up some EUV manufacturing capacity—which benefits Nvidia.

In any case, we’ll probably learn more once the semiconductor manufacturers release their results (I have to keep an eye on TSMC, Intel, and Samsung in particular).

Nvidia is facing packaging issues

Final problem: Nvidia’s biggest challenge today lies in the new packaging required for the production of Blackwell chips.

Nvidia and TSMC have worked together to develop the CoWoS-L process, an improvement over the previously used CoWoS-S. They encountered several challenges, which notably led to delays in the production of Blackwell.

Here is an excerpt from an article explaining the core issue:

“The main problem affecting deliveries is directly related to Nvidia's Blackwell architecture design.

The supply of the original Blackwell package is limited due to packaging issues at TSMC and Nvidia's design. The Blackwell chip is the first large-scale design to be packaged using TSMC's CoWoS-L technology.

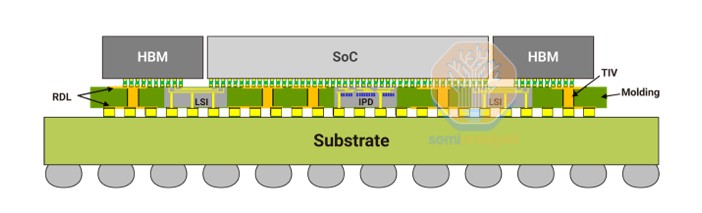

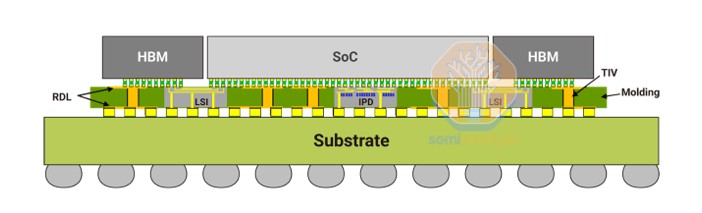

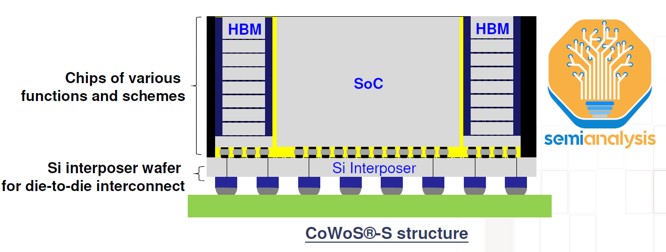

(Packaging CoWoS-L)

To summarize, CoWoS-L uses an RDL interposer with Local Silicon Interconnects (LSI) and bridge chips embedded in the interposer to enable communication between the different compute units and the package’s memory.

In comparison, CoWoS-S is much simpler in structure, essentially a large block of silicon.

CoWoS-L is the successor to CoWoS-S due to the challenges posed by the increasing size and performance demands of CoWoS-S packages, as future AI accelerators integrate more logic, memory, and I/O (input/output).

TSMC has improved CoWoS-S but it has reached its practical limit.

There are several limiting factors, but the main one is that silicon is fragile, and handling ultra-thin silicon interposers becomes increasingly difficult as their size grows. These large silicon interposers also become more expensive due to the increased need for lithographic reticle stitching.

Organic interposers could solve this issue since they are less fragile than silicon, but they suffer from weaker electrical performance and do not provide enough I/O for more powerful accelerators. Silicon bridges (either passive or active) can be used to increase signal density and compensate for this limitation. Moreover, these bridges can offer higher performance and complexity compared to large silicon interposers.

CoWoS-L is a much more complex technology, but it represents the future. Nvidia and TSMC set an extremely aggressive ramp-up schedule, targeting over a million chips per quarter. As a result, several issues have arisen. »

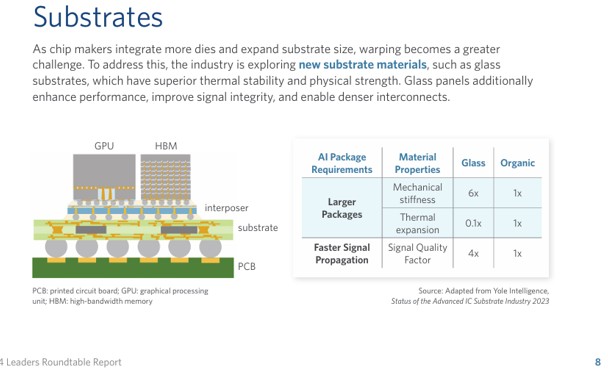

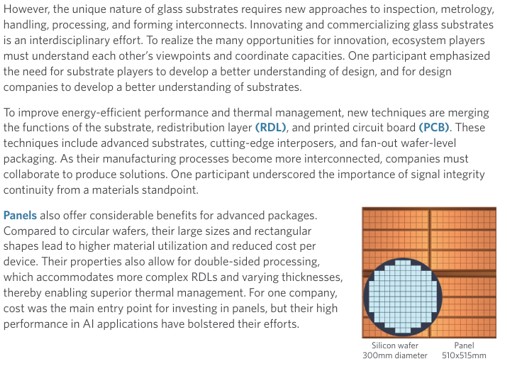

Here are other points I found about the future of packaging technology :

*2024 Leadership Summit for Advanced Packaging - Roundtable Report

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.