ASML Stock Q2 2025

Analysis into ASML Q2 2025 earnings

STOCKSEMICONDUCTORQUARTERLY EARNINGS

Rafael CARRARA

2/15/20267 min read

Earning call

2025 Q2

Market is down after earnings again in Q2 though still up since Q1 release, let’s see why it’s down :

Here is extract of the article :

“Looking at 2026, we see that our AI customers’ fundamentals remain strong. At the same time, we continue to see increasing uncertainty driven by macro-economic and geopolitical developments,” Fouquet said in an earnings release. “Therefore, while we still prepare for growth in 2026, we cannot confirm it at this stage.”

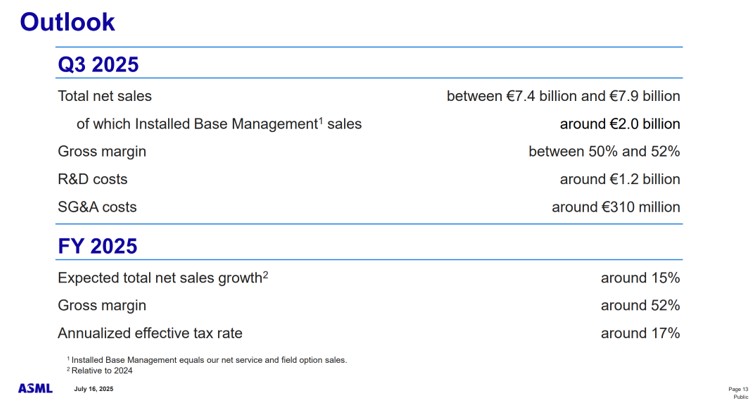

ASML also narrowed its guidance for this year. It’s now predicting sales to rise 15% to €32.5 billion, having previously forecast a range of €30 billion to €35 billion. Analysts are expecting sales of €32.36 billion, according to a FactSet poll.

U.S. tariffs have made it tough for European companies to stand by past profit guidance. President Donald Trump has threatened 30% levies on the European Union from Aug. 1, and the trading bloc is preparing retaliatory tariffs. That could make it more expensive for ASML to ship its chip tools to Intel and other American customers.

Ok, I see the issue. So basically, the market is reacting the exact same way as in Q1 and is worried about the impact of tariffs on ASML’s future results. So I’m expecting a a similar analysis as last time but let’s verify.

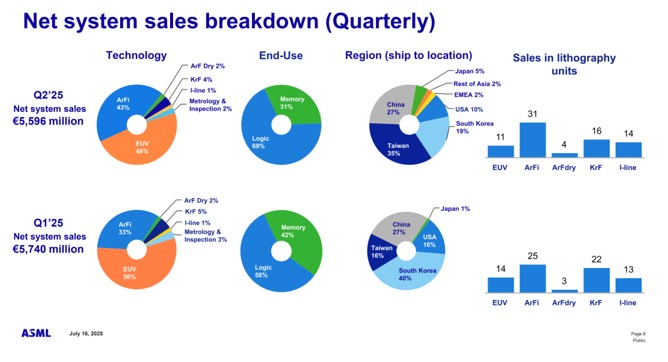

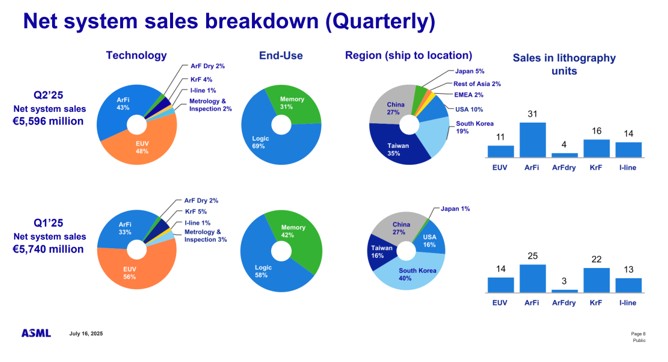

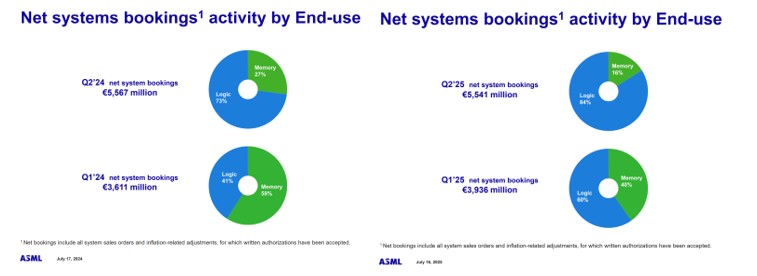

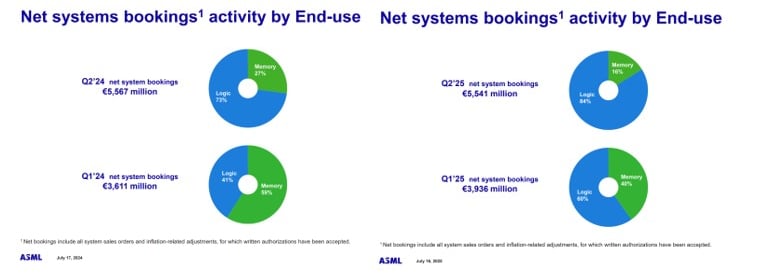

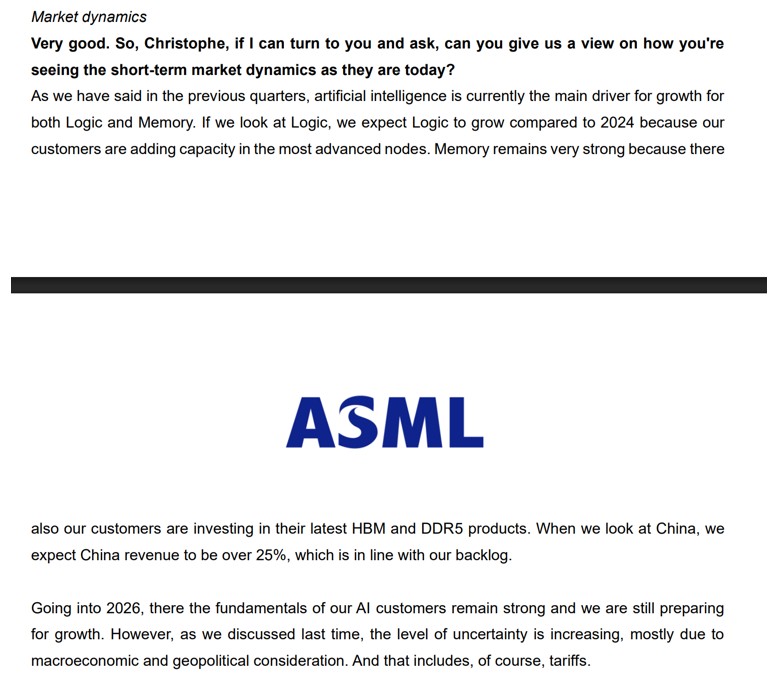

Ok, so a decrease from south Korea as Samsung’s or SK Hynix order were being done mostly in Q1 2025 though we see they are still buying quite a bit, and we are seeing the ramp up from TSMC in Taiwan as we saw last quarter, they are expanding their capital expenditure.

2024 Trough Q2

As we can see the numbers are great compared to 2024.

We can see the big increase in from the logic part and slight increase in the memory part. As we said it mainly comes from the ramp up from TSMC in capital expenditure.

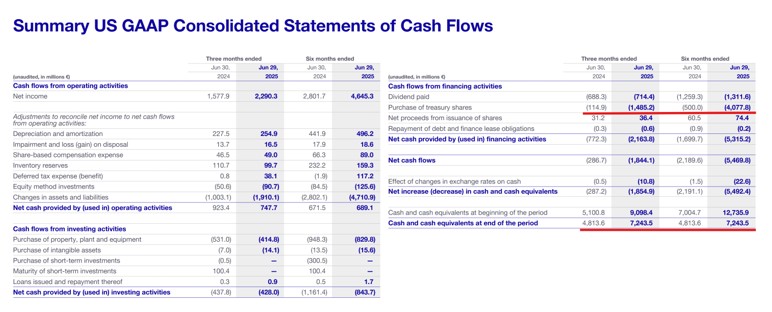

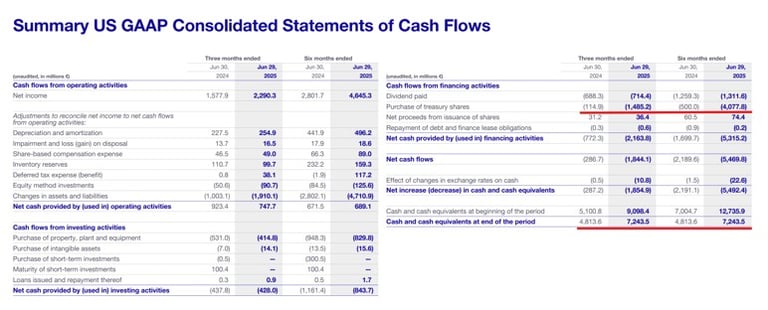

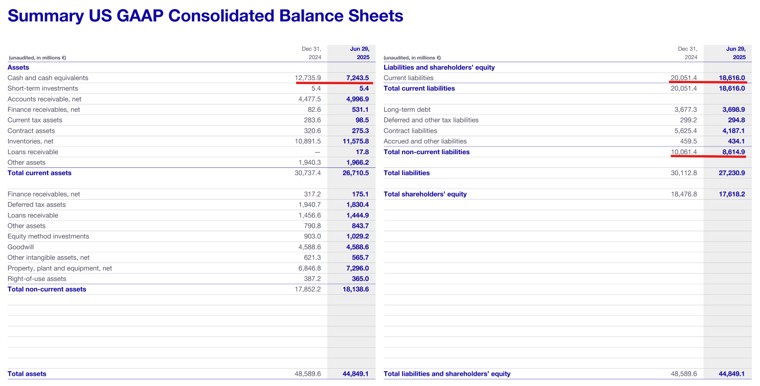

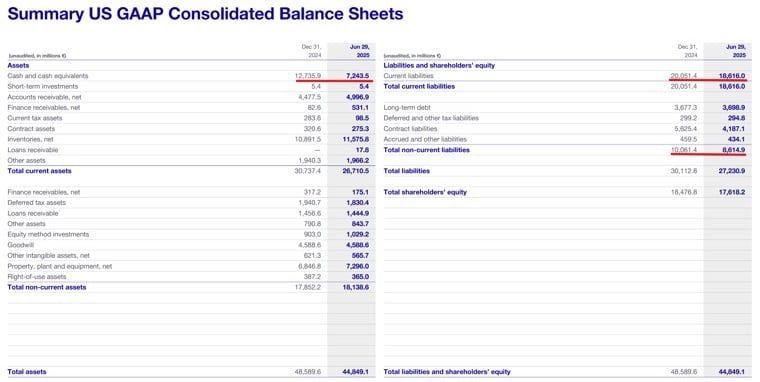

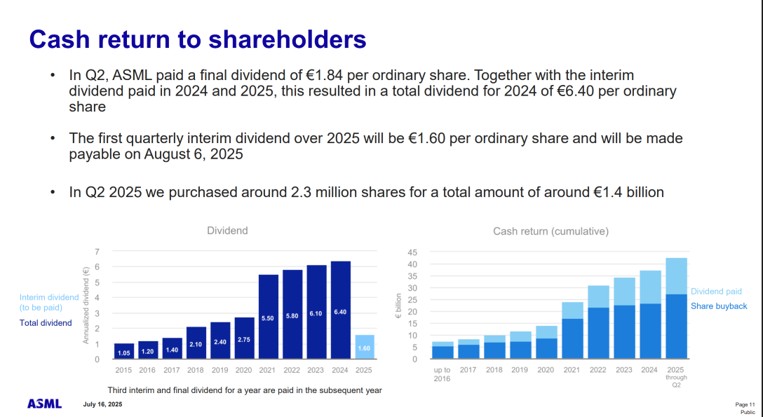

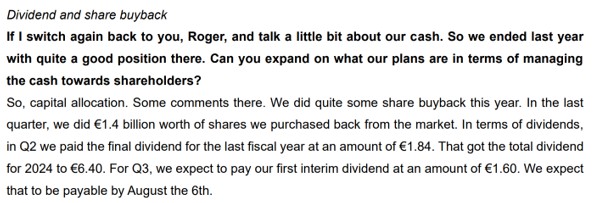

They are continuing to buyback shares as they did in Q1 and they still have more cash than in mid 2024.

Though less cash than in December 2024.

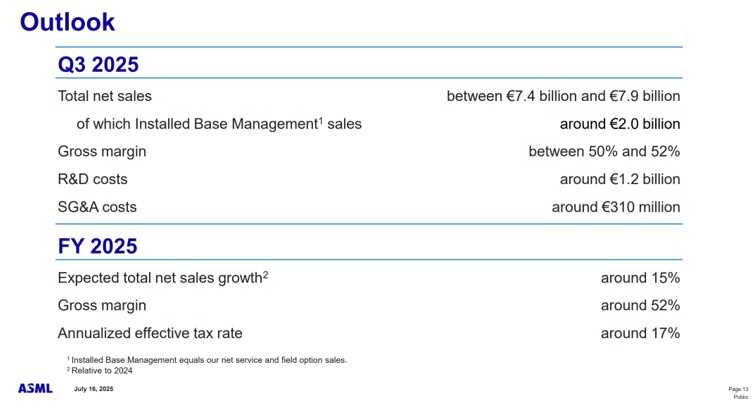

They are giving a more accurate guidance for the year, which seems reasonable to me considering what we said earlier, though we should still take into account the lower range of the guidance given in Q1 as there is a risk with trumps tariffs.

so, let’s see what happens with the lower part from Q1 and their guidance from Q2 with the current market cap.

guidance assumption from Q2: 32.5 billion euros, with a 28% net margin ==> 9.1 Bn euros net profit

251.8 Bn euros market cap ==> makes it a 27.6 PE at the end of the year if they attain the numbers from a 32.53 PE right now. Based on current market cap.

Low guidance assumption: 30 billion euros, with a 28% net margin ==> 8.4 Bn euros net profit

251.8 Bn euros market cap ==> makes it a 30 PE at the end of the year if they attain the numbers from a 32.53 PE right now. Based on current market cap.

As we can see the opportunity was more interesting in Q1 when the price was lower, that’s where I bought most of my position. Right now, I think it’s still a buy but less interesting than in Q1.

Now things could become worse than the lower part of the guidance if we see a recession. But The slowdown would be temporary as the underlying AI demand is still pushing the semiconductor market.

So I don’t see an increase of risk for now for the long term prospect of the business.

All in all, I have a hard time understanding the reaction of the market, outside of that they had very high expectations thinking it was going to be on the higher side of the guidance range or even above that, and they were disappointed when it came a bit short of that because of tariffs.

As I see it, with the decrease in price, the situation just got better from a risk/reward perspective for the long term than a week ago, though not as interesting as in Q1 where there was a bigger dip in price as the tariff factor was new and consequences not well understood and the fear greater.

Earning call transcript

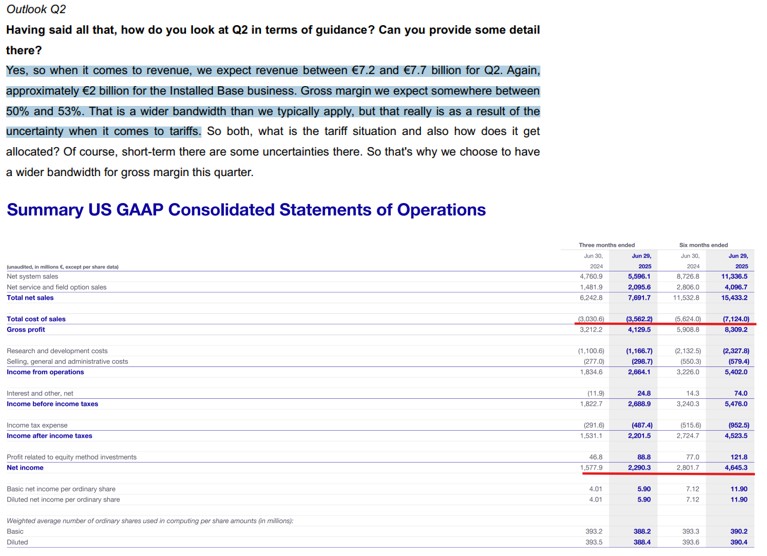

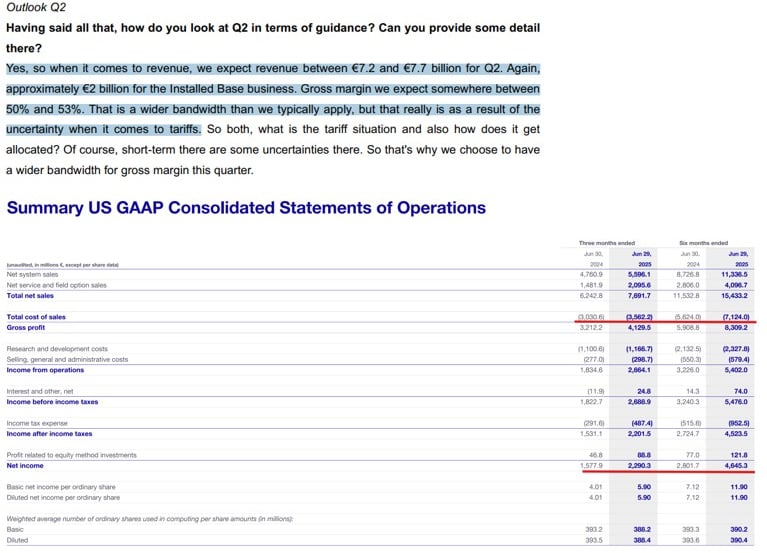

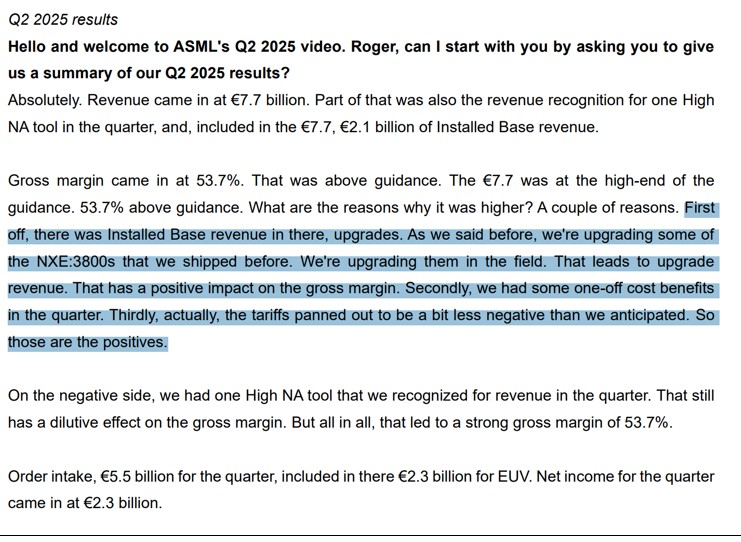

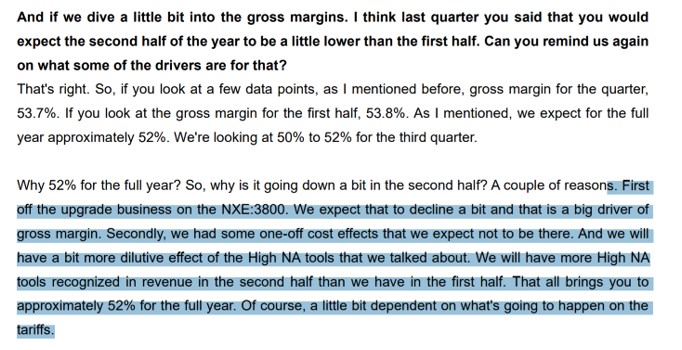

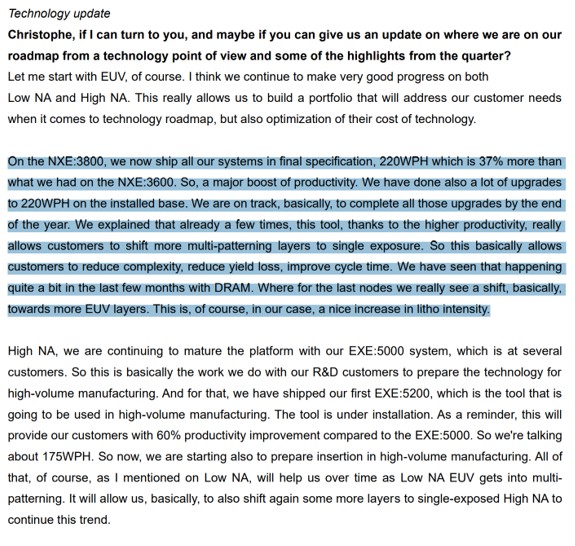

The higher margin was mainly because of the upgrades to the NXE:3800s that were shipped. We can see how the spending in R&D can bring revenue not only with new machines but with the upgrades they provide to the existing machines owned by the clients.

Will have to confirm the guidance.

So exactly same thing that was said in Q1 and that is what spooked the market, funny when you think about it because exactly the same thing was said in Q1, for memory:

In Q1 :

As we guessed in the analysis of ASML the growth mainly comes from the EUV part of the business.

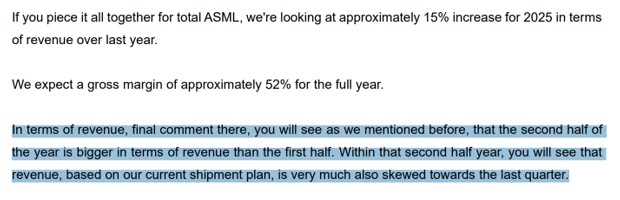

And as we said in Q1 generally they have a second half of the year that is bigger than the first half in term of revenue.

But margin will be lower because of the sale of High NA tools but that is also why they have the higher revenue and so more profit though margin contract a bit. To be expected for the second half of the year.

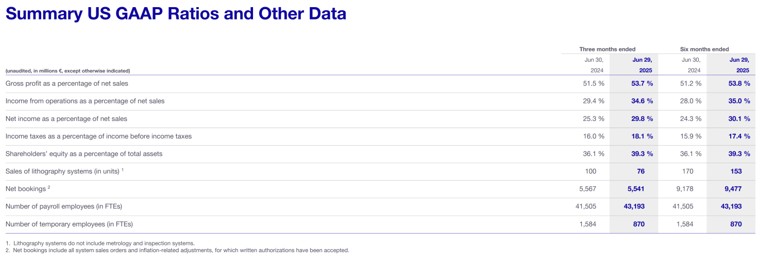

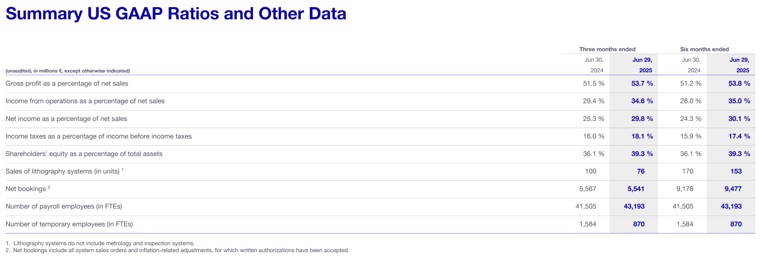

Overall ratios are looking good with an increase in margins in comparison with last year.

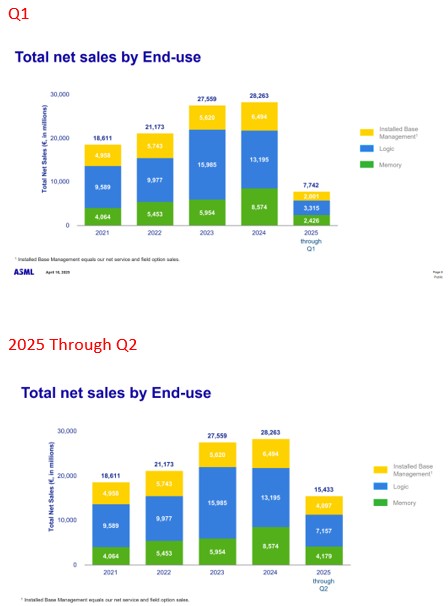

A near 50% increase in revenue compared to 2024, and nearly 2x the net income compared to 2024.

They have managed to meet the higher end of their guidance for the quarter, which is a good sign.

Those are again great results, now those results are still mainly because of the ramp up in capex coming from TSMC, so to keep in mind, but still great results.

They also managed that increase in profits not by decreasing spending in R&D but by controlling the increase in the cost of sales which I like.

So, to summarize they are deploying some of the cash that they had accumulated in 2024 to buyback shares and diminish their liabilities which is ok with me. 4 Billion for buybacks and around 4 Billions to decrease liabilities. That’s why they have negative cash flows, what they earned they must have put in the liabilities and with the cash on the side they starting doing buybacks, or inverted.

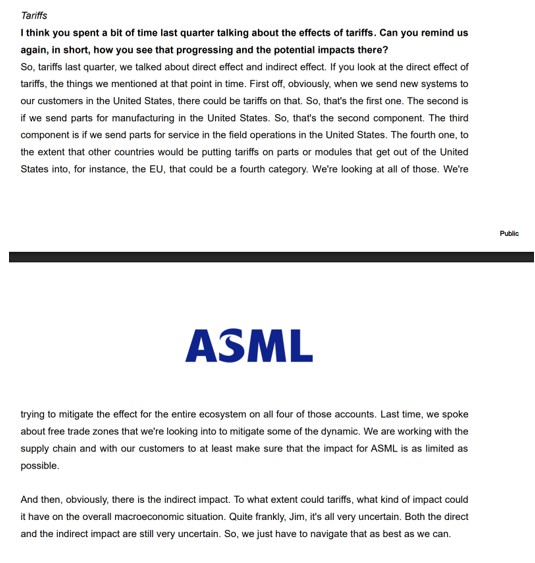

To summarize we will have to see the effect of the tariff if and when they are applied.

Impact hard to predict.

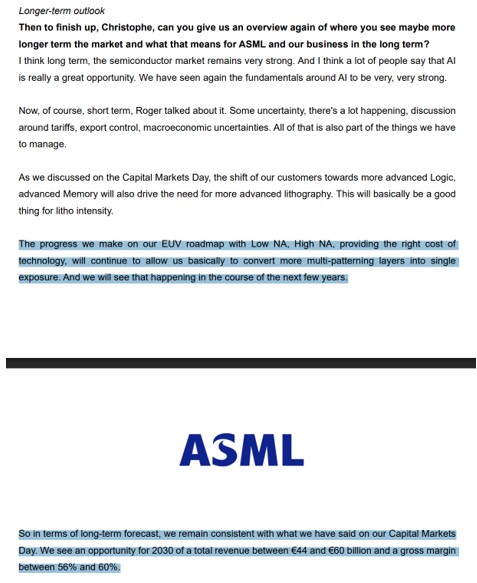

For me that is the more important part of the earning call and that is very important to follow, the dynamic between single exposure use and multi-patterning layers. For now we have a good dynamic, so good news.

As we guessed they did buyback with some of the cash they had on the side and they paid liabilities with the cash that came in.

They reaffirmed their long-term guidance and as we said earlier the most important thing for the long term earnings of the company is the dynamic between single exposure layers and multi-patterning layers. If single exposure layer increase compared to multi-patterning that is great for ASML future earnings with EUV usage that will have to increase. Have to follow the advanced packaging part that could also be another way to increase the number of transistors, to follow with the analysis of BESI.

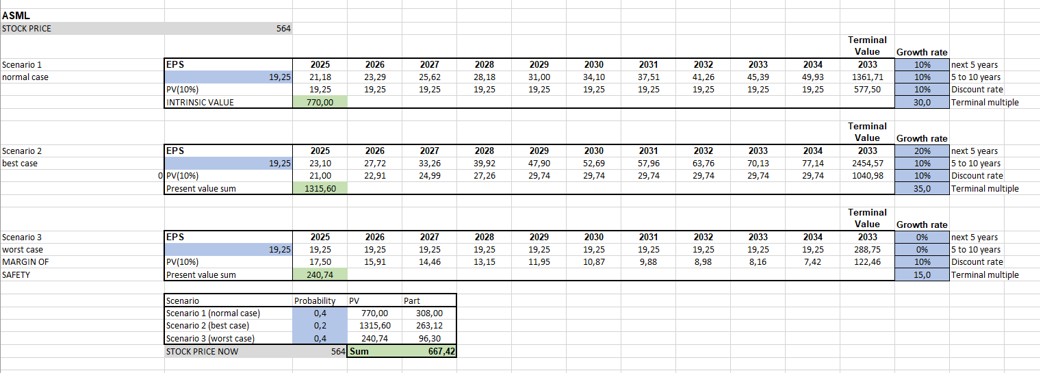

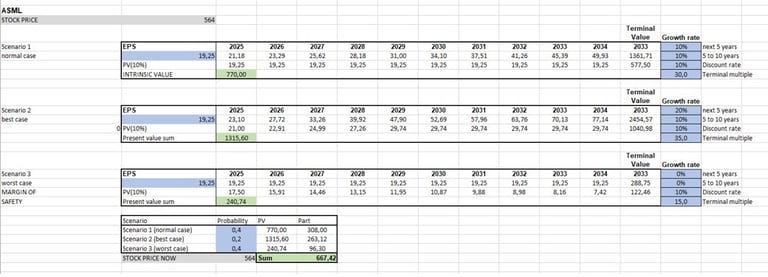

I maintain the valuation done in Q1 for the same reasons, and thus still a buy for me:

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.