ASML Stock Q1 2025

Analysis into ASML Q1 2025 earnings

STOCKSEMICONDUCTORQUARTERLY EARNINGS

Rafael CARRARA

2/10/20265 min read

Earning call

2025 Q1

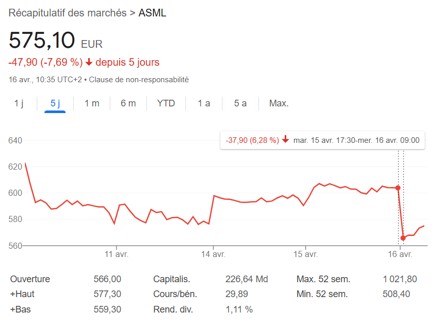

Market is down after earnings call, let’s see why :

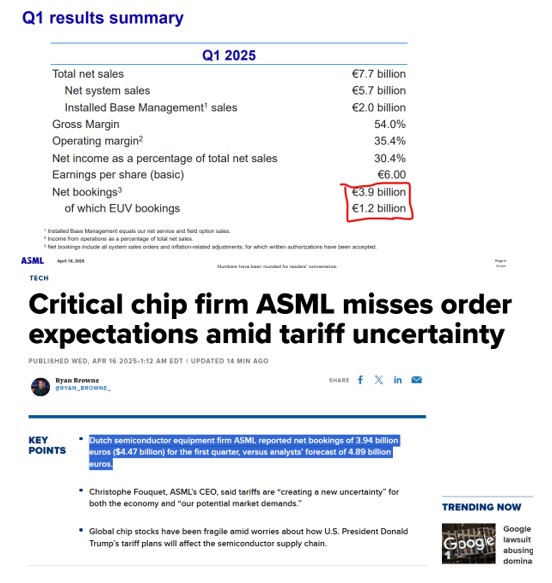

Ok, I see the issue, Net bookings are at around 4 Billion euros when the market was expecting more around 4.9 Billion euros in net booking for the quarter. So basically, the market is worried about the impact of tariffs on ASML’s future results.

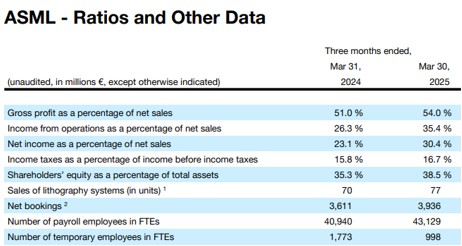

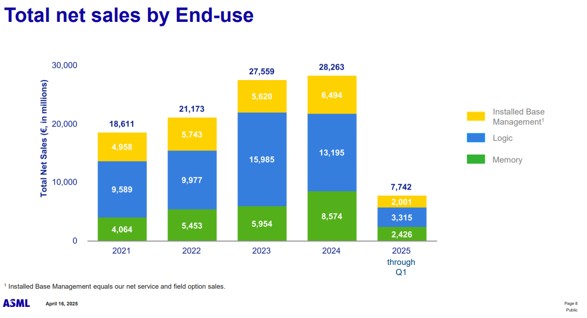

Though when we compare to 2024, ASML is doing better even in net bookings actually. They generally have a slower net booking at the start of the year to increase through the year :

It’s still an 8-9% increase in net Booking compared to the previous year in the middle of a chinese-USA trading war. And having better results for Q1.

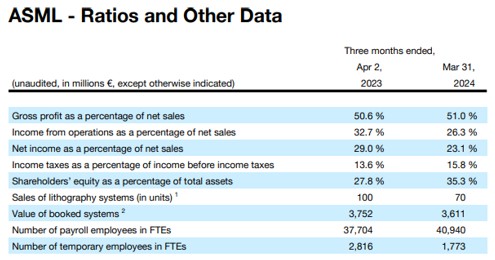

Here what was the Q1 results in 2024 compared to 2023 :

So, way worse results in 2024 all in all, and a betterment of the situation through a US-China trade war, and people are ready to sell things at a lower price ?

Count me as a buyer. Though we must recognize that there is the possibility that between what is booked and what will actually be delivered the situation might change with the uncertainty of tariffs, I would say the risk/reward situation included in the price is actually surisingly better now for the long term.

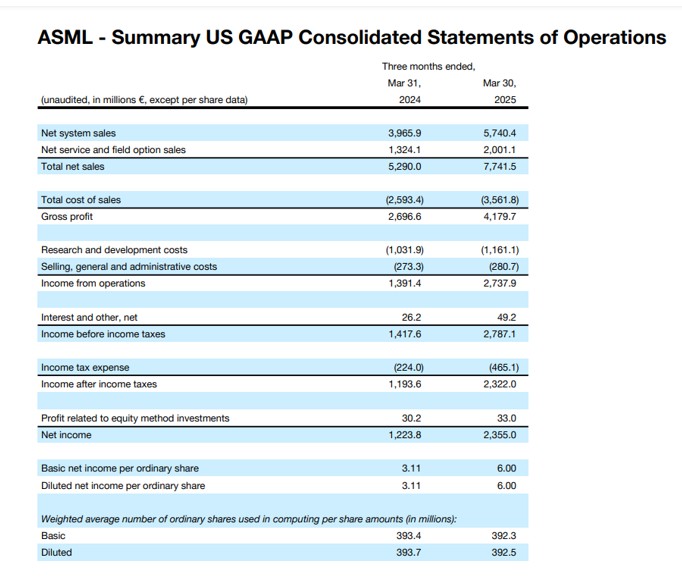

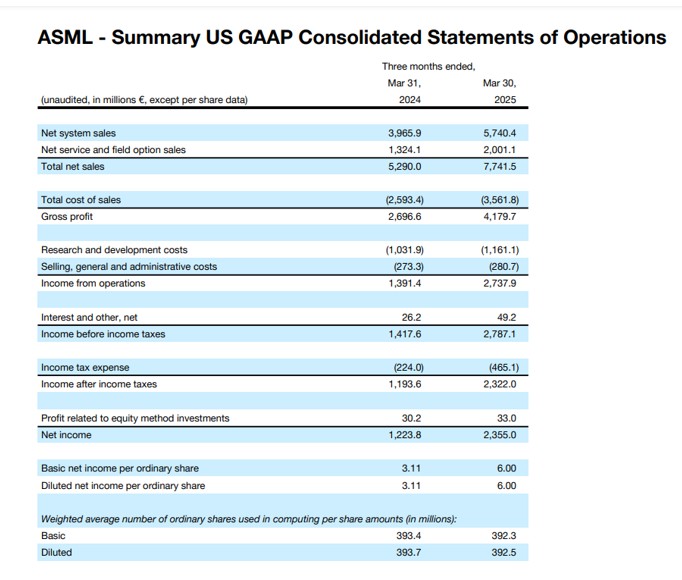

A near 50% increase in revenue compared to 2024, and nearly 2x the net income compared to 2024.

Those are increadible results, now those results could be the result of customers wanting to buy more at the start of the year to avoid the tariffs put in place to avoid the future that is to come.

But net booking being higher than 2023 seems to contradict that narrative. Will have to watch to see which direction it goes.

Things have decreased compared to Q4 24, but that’s misleading, as we know they generally have lower results at the start of the year to increase the results through the year.

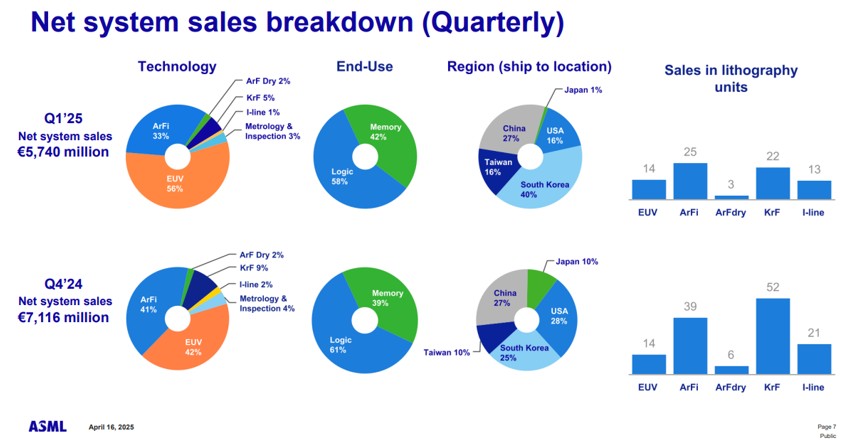

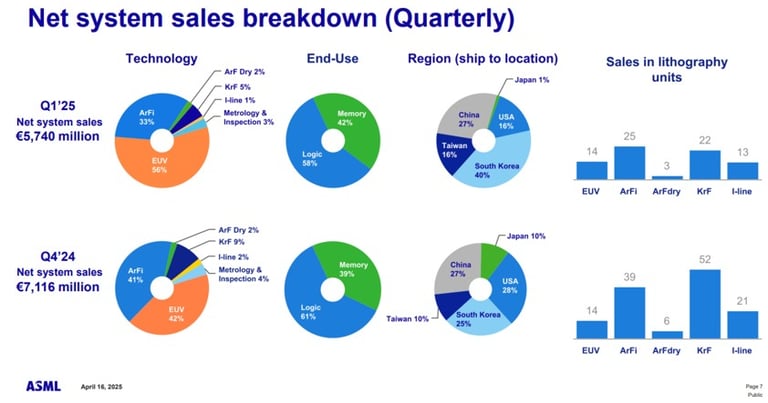

We can see a big increase of orders coming from south korea and and an increase in the percentage of EUV in the revenue. Big orders from Samsung ? Will have to see when I do a Samsung analysis.

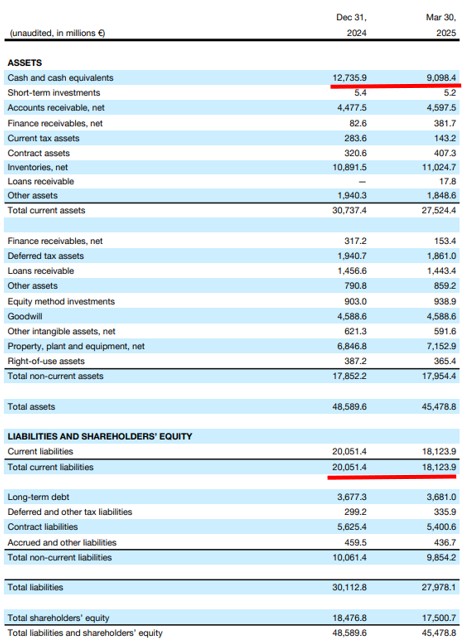

It seems they used some cash to pay some of their liabilities. But no big change.

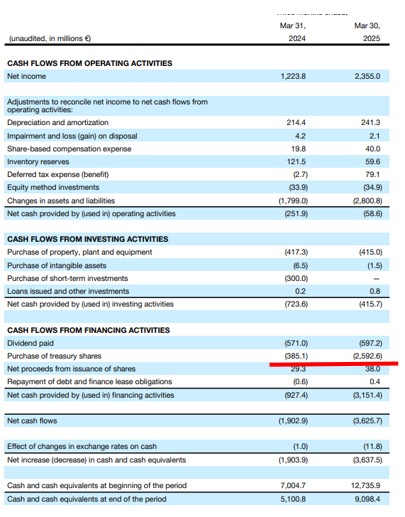

And it seems they also used some cash to make a 2.6 Bn euros of buybacks. So, they bought back more shares than in 2024 and 2023 combined in Q1 of 2025. I like that they are doing buybacks now and not when the share price was double what it is actually. We could see 2021 levels of buybacks (8.5 Bn euros) which would represent around 4% of the current market cap.

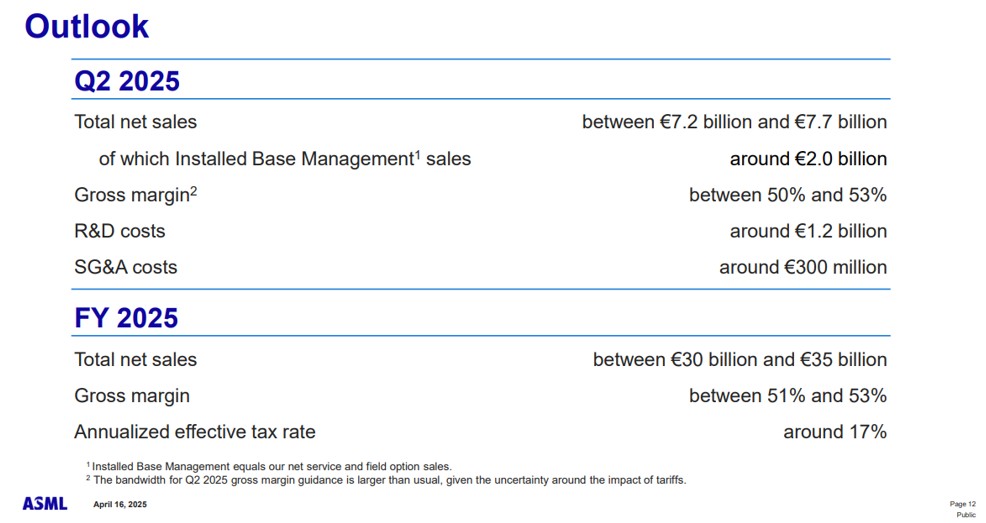

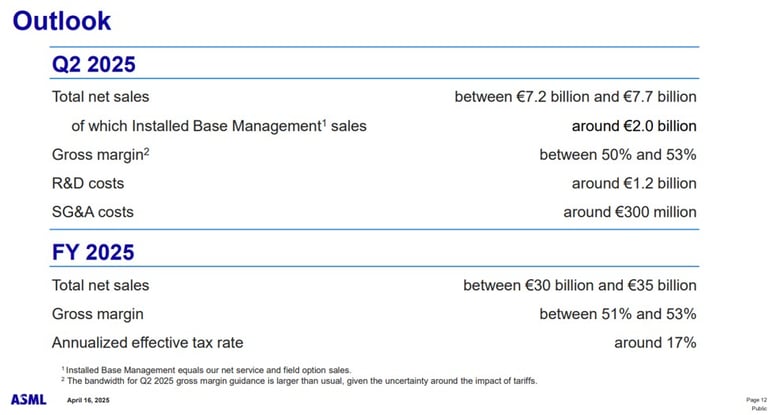

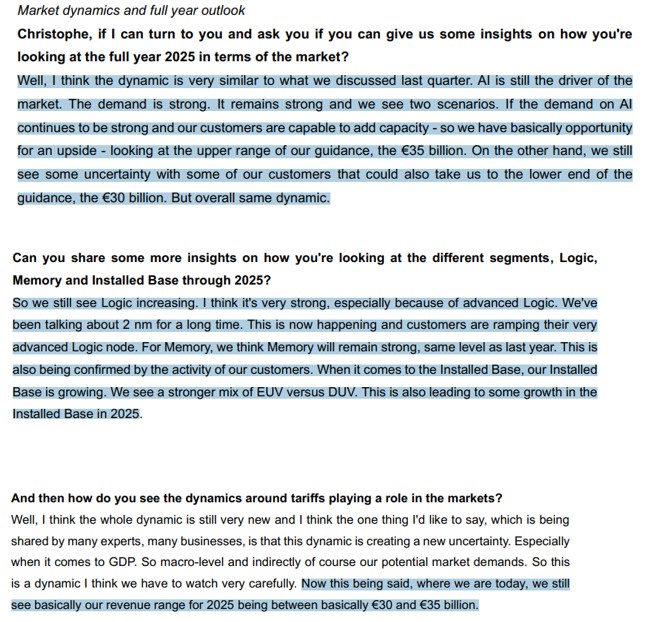

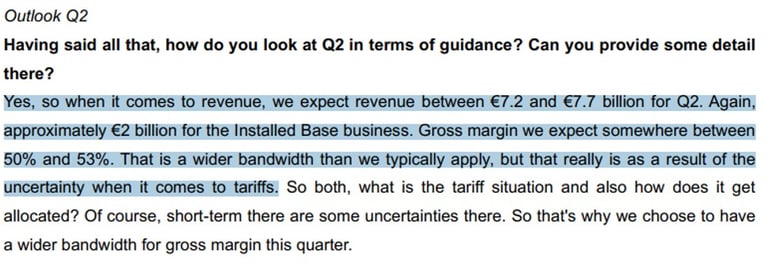

They are maintaining their guidance for the year, which seems reasonable to me taking into account what we said earlier, though we should take into account the lower range of the guidance as there is a risk with trumps tariffs.

so, let’s see what happens with the lower and higher part of their guidance range with the current market cap.

High guidance assumption: 35 billion euros, with a 28% net margin ==> 9.8 Bn euros net profit

226 Bn euros market cap ==> makes it a 23 PE at the end of the year if they attain the numbers from a 30 PE right now. Based on current market cap

Low guidance assumption: 30 billion euros, with a 28% net margin ==> 8.4 Bn euros net profit

226 Bn euros market cap ==> makes it a 27 PE at the end of the year if they attain the numbers from a 30 PE right now. Based on current market cap.

Now things could become worse than the lower part of the guidance if we see a recession. But The slow down would be temporary as the underlying AI demand is still pushing the semiconductor market.

So I don’t see an increase of risk for now for the long term prospect of the business.

All in all, I have a hard time understanding the reaction of the market, outside of that they had very high expectations, and they were disappointed when it came a bit short of that because of tariffs.

As I see it, the situation just got better from a risk/reward perspective for the long term.

Earning call transcript

So as we said, they are maintaining their guidance, though there is an element of unpredictability with tariffs, to be expected.

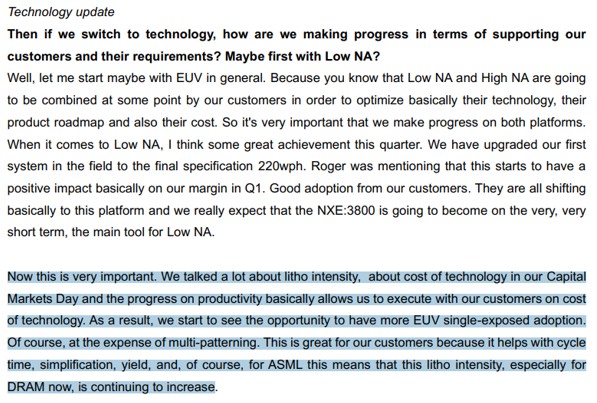

Very good news for ASML ! This could mean more customer changing from DUV machines to EUV ones if that’s the case. Which means growth in revenue as the machines are more expensive.

For a reminder :

ArFi machine: Between €50 million and €80 million per machine

EUV Low-NA: Between €120 million and €200 million per machine

EUV High-NA: Between €350 million and €400 million per machine

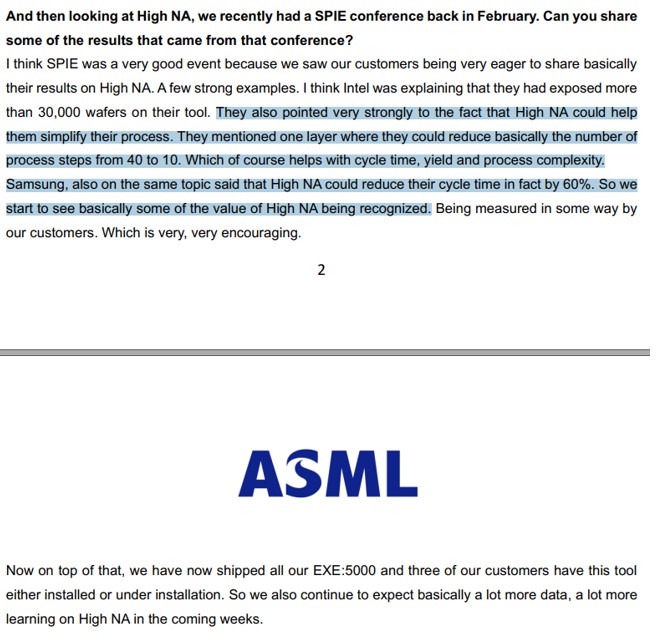

The High NA machine development is following its course.

He is talking about Cymer in San diego that produces the lasers of ASML Machines :

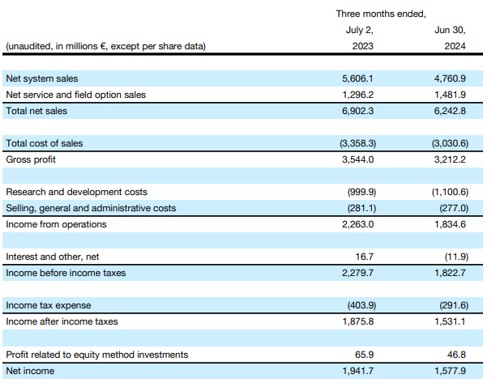

By the way those were the results in Q2 2023 and 2024, so in the lower range they are still expecting better than in 2023 :

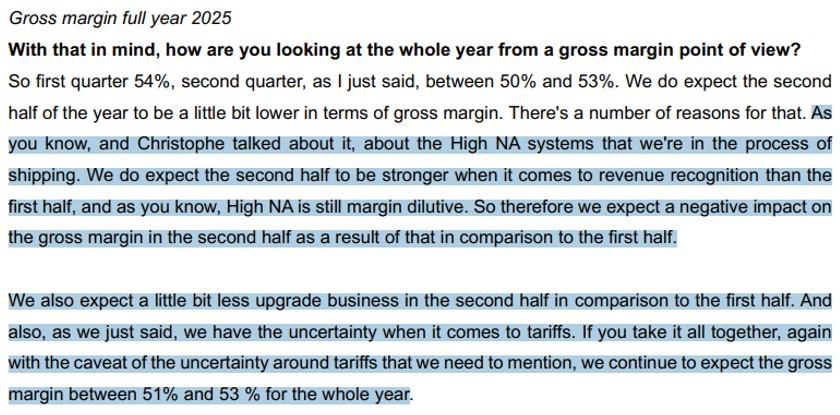

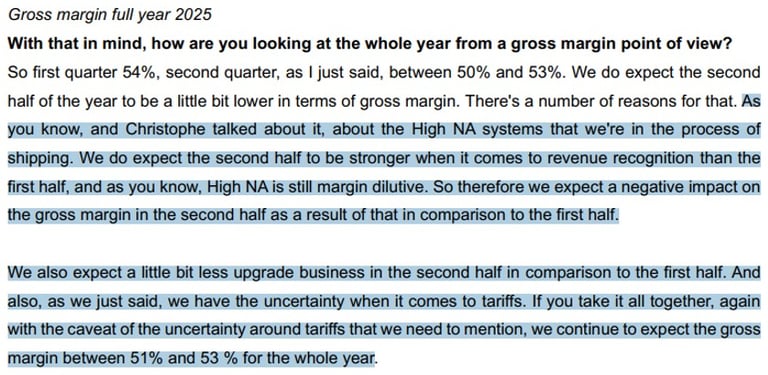

As I said earlier, they will have more revenue in the second half of the year but with lower margin as that is when they deliver their high NA machines.

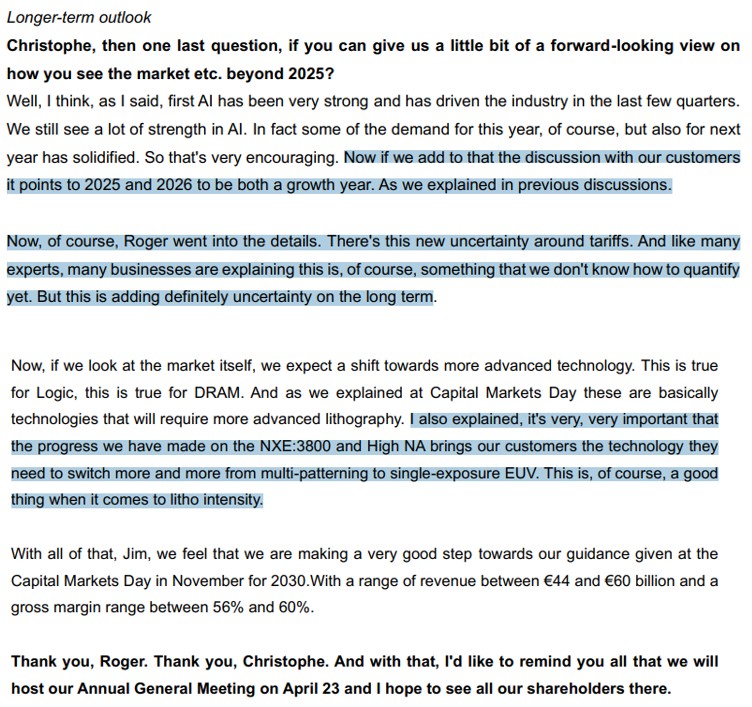

I agree with the CEO that the move from multi-patterning to single-exposure EUV is a key point for the growth of ASML revenue and profit. So, an important point to follow.

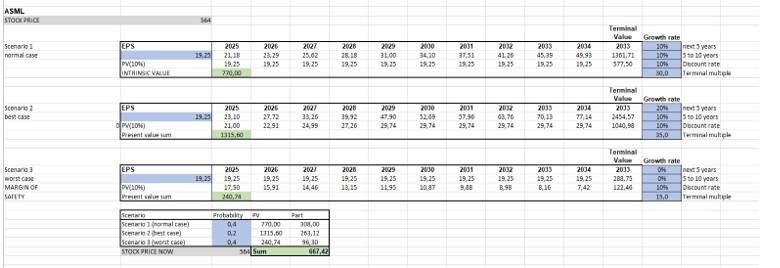

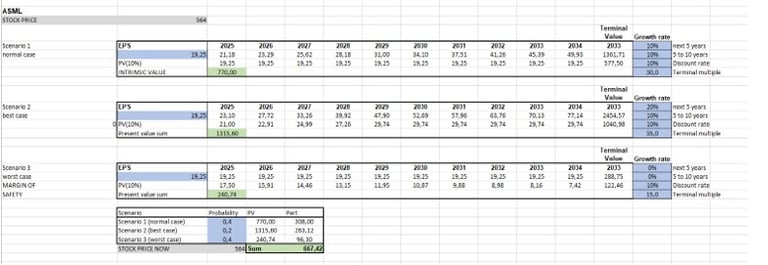

Here an update to the valuation :

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.