airBaltic € 4Y bond

Analysis into airBaltic's company developments, effects on the publicly-traded 4-year bond and financial performance.

FIXED INCOMEAIRLINES

1/1/202612 min read

airBaltic's EUR 380 million 14.5% senior secured bond maturing August 2029 reflects a credit story defined by structural financial fragility, heavy state dependence, and event-driven spread volatility. The airline entered 2024 with EUR 118.5 million in losses against EUR 747 million in operating revenue — a EUR 151.8 million swing from the EUR 33.7 million profit posted in 2023 — with cost per available seat kilometre deteriorating 9% year-on-year, and 19% on a ex-fuel basis, pointing to deep operational rather than commodity-driven pressures.

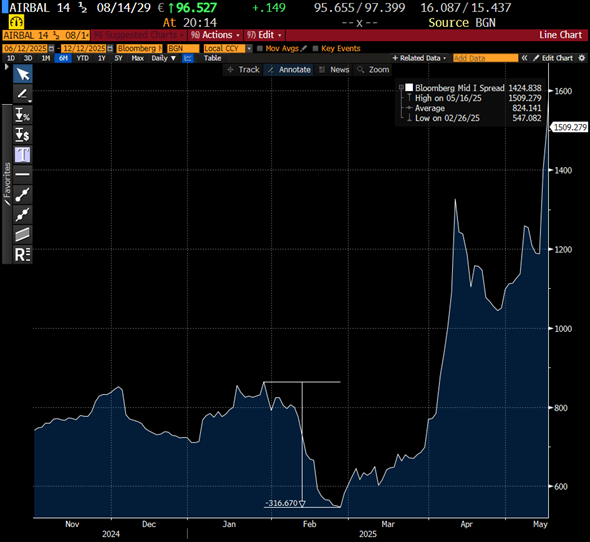

The bond had already widened 655 basis points ahead of the April 2025 AGM at which CEO Martin Gauss was fired, with a further 389 basis points of widening in the immediate aftermath. Lufthansa's January 2025 EUR 14 million convertible stake acquisition — mirrored by an equivalent Latvian state injection in August under EU state aid parity rules — provided temporary relief, with the spread tightening 317 basis points on the announcement, though 9-month 2025 financials showed the underlying operating picture little changed year-on-year, with the apparent profit improvement driven almost entirely by a EUR 67 million FX gain rather than operational recovery. The Fitch downgrade to CCC+ in December 2025 crystallised the core risk: the IPO, originally targeted for 2025 and now delayed to at least 2026, remains the critical refinancing and liquidity event, and absent a substantial equity injection the airline's financial flexibility remains severely constrained.

—

Corporate developments

30 January 2023 - Moscow city arbitration court orders to recover EUR 31 mn from airBaltic

On 30 January 2023, the Ninth Arbitration Appeals Court in Moscow overturned a prior Moscow City Arbitration Court ruling and ordered airBaltic to pay EUR 31 million (approx. USD 33.4 mn) to Russia's Deposit Insurance Agency (DIA), acting as bankruptcy trustee for the defunct Investbank.

The decision invalidated loan agreements originally made in 2011 between Investbank and Baltijas Aviācijas Sistēmas (BAS), which held a 47.2% stake in airBaltic at the time. The court found evidence that the loan funds (totaling around EUR 18.4 mn principal plus interest and fines) were transitory and directly used by airBaltic rather than BAS.

This stems from civil cases launched by Investbank in 2012 against BAS and airBaltic as co-defendant for repayment. Earlier Russian rulings (around 2016) had ordered partial repayments (e.g., EUR 13.5 mn in two cases). Investbank's license was revoked in December 2013 by the Russian Central Bank.

airBaltic stated that its Russian lawyers were reviewing the claim as a historic matter and that no final court decision text had been received yet, limiting further comment at the time. The airline has maintained that all related debts were annulled under a 2011 Latvian government bailout agreement. (source)

12 February 2024 - The state-owned airline airBaltic has half a year left to find EUR 200 mn to repay buyers of bonds issued in 2019

On 12 February 2024, Latvian state-owned airline airBaltic faced a critical liquidity challenge with approximately six months remaining to repay EUR 200 million in bonds issued in 2019 and maturing in July 2024. The company reported negative equity of EUR 71 million, short-term liabilities exceeding current assets by EUR 352 mn (as per the latest nine-month 2023 financial report), and acknowledged that it did not currently hold the necessary funds for repayment. CEO Martin Gauss expressed confidence in securing financing through private lenders or capital markets while leaving open the possibility of state shareholder involvement, and airBaltic presented three potential options: borrowing from private lenders, issuing new bonds, or seeking state assistance.

In an interview reported by Latvian Television's De Facto, Gauss stated that the company intended to refinance the bonds with private funding or market instruments rather than immediately requesting government support, though he noted the state's shareholder role could be utilized if needed. He highlighted that borrowing costs were expected to be significantly higher than the original 6.75% coupon on the 2019 bonds, due to elevated market rates and perceived regional risks from Russia's war in Ukraine.

The news also covered airBaltic's long-term plans for an initial public offering (IPO), which had been under consideration since 2018 but had not yet attracted strategic investors; board member Vitolds Jakovļevs emphasized that an equity listing represented the primary path to strengthening the balance sheet given the lack of alternative capital sources. Gauss stressed the airline's strong operational momentum, including projected 2023 turnover of around EUR 668 mn and an anticipated first annual profit since 2018, positioning these results as key to attracting future investors despite ongoing financial weaknesses.

Experts quoted in the coverage, such as Andrejs Martinovs from INVL Family Office, expressed caution about the IPO timing, describing airBaltic's profile as resembling a high-growth startup rather than a mature listed company, and noted that bond refinancing would likely carry double-digit yields given market conditions. (source)

29 January 2025 - Lufthansa invests EUR 14 mn in airBaltic and lands a seat on the supervisory board

The investment grants Lufthansa a convertible shares of 10% stake in the Latvian airliner. The subscription price is the invested amount to be converted into ordinary shares upon IPO. This links the importance of the IPO going through. Following the IPO, the final stake size will depend on market pricing, with the group’s shareholding in the Baltic carrier amounting to no less than 5%, both companies outlined in a statement.

This investment builds on the existing wet lease agreement (source). Lufthansa announced a further 3-year extension beyond summer of 2025; 21 additional Airbus A220-300 fuel-efficient aircrafts and 5 over winter.

At that time, the nearly 5Y bond spread improved on these news by 317 bps tightening:

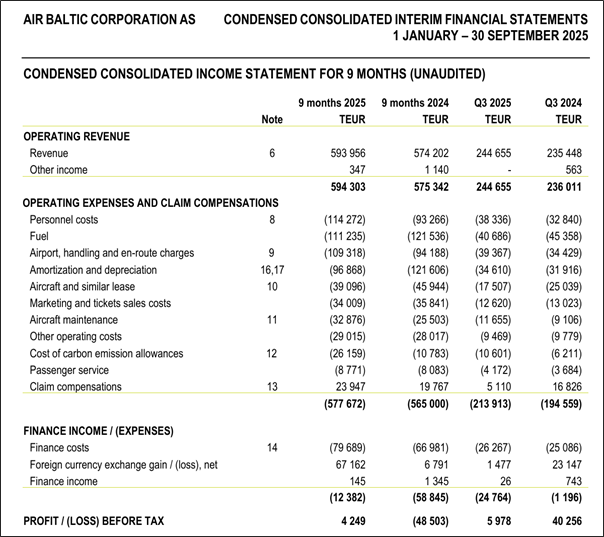

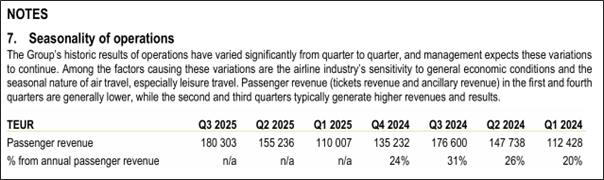

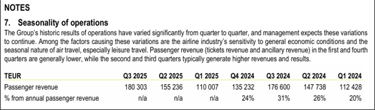

Did this improve summer earnings in 2025 for airBaltic? Not exactly, revenue largely unchanged on 9M basis year-on-year. The profit before tax does appear almost EUR 53 mn better than 9M 2024 but the main driver is a 67 mn FX gain in the 9M 2025 period. The operating revenue, expenses and claim compensations were largely similar year-on-year and were not the main drivers for the period delta in the before tax result. (consolidated financials 9M 2025) Additionally, the seasonality of each quarter shows that the 2nd and 3rd quarters of 2025 and 2024 are mostly similar in passenger revenue (p.31).

7 April 2025 - The state controlled supervisory board of airBaltic fired CEO Martin Gauss on AGM

At the time, the Republic of Latvia owned 97.97%, Aircraft Leasing 1 SIA 2.03% and other 0.000084%. Reuters reported the German CEO that he was surprised by the news and that the Latvian government had a “nasty” handling of his departure (link). Gauss told Reuters he “lost trust of the government”. This was the sixth Latvian government and struggled with this last. Board chairman Andrejs Martinovs mentioned poor financial performance.

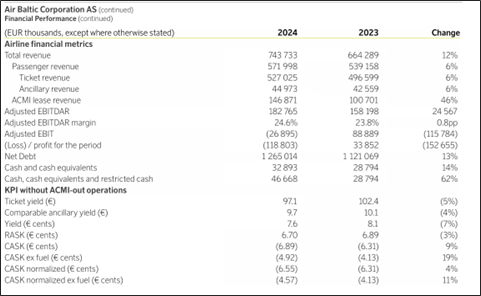

How bad was this poor 2024 financial performance? In 2024, EUR 118.5 mn loss vs the EUR 747 mn operating revenue, not a pretty picture (highlights). The delta vs 2023 was EUR 151.8 mn decrease from having a positive profit result YE 2023 of EUR 33.7 mn (2024 annual report).

Cost per Available Seat Kilometer (CASK) = Total Operating Expenses ÷ Available Seat Kilometers (ASK). Available Seat Kilometers (ASK) = Number of seats available for sale × Distance flown (in kilometers). This is the measure for total seat capacity the airline offered, regardless of whether sold or occupied. Why should one care about CASK? It measures how much it costs the airline to produce one unit (seat) of capacity per kilometer flown.

CASK was 9% worse year-on-year and when isolating without fuel it shows a 19% worsening. In other words, fuel price volatility or hedge mismanaging was not the main culprit for the negative result. Assuming CASK normalized is adjusting for average flight distance thereby spreading fixed costs over more kilometers, the picture isn’t that much better at an 11% decrease over the period.

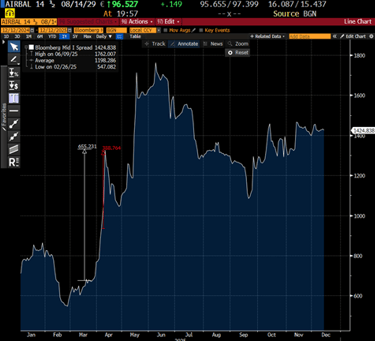

Their outstanding bond 14.5% 08/14/29 widened 655 bps even prior to the news and the AGM meeting on the 7th of April. The reaction from the AGM to nearest wide-most point was 389 bps widening. The bond remains wider to date than the levels after the AGM and firing of former CEO.

30 June 2025 - German competition authority (Bundeskartellamt) cleared under merger control rules plans by Deutsche Lufthansa AG to acquire a minority stake in airBaltic

On 30 June 2025, the German Federal Cartel Office (Bundeskartellamt) cleared under merger control rules Deutsche Lufthansa AG's plan to acquire a minority stake in airBaltic Corporation AS. The authority approved the transaction despite identifying significant competition concerns on several flight connections between German airports and the Baltic states, where the two airlines are direct competitors with limited alternative carriers on certain routes.

The Bundeskartellamt stated that clearance was required because the affected routes constituted “minor markets” with very low domestic sales volumes (total sales below the €20 million threshold under German national merger provisions), which prevented prohibition of the acquisition. The minority stake grants Lufthansa a 10% holding along with additional rights to participate in airBaltic’s decision-making process. The authority expects that Lufthansa will thereby gain material competitive influence on airBaltic, particularly as the companies’ interests will be taken into account to a significant extent in airBaltic’s decisions, although the airlines will remain separate legal entities and direct anti-competitive agreements or price coordination will continue to be prohibited.

The decision also assessed the existing and expanded wet-lease cooperation between the two carriers. The Bundeskartellamt found no competition concerns in the European wet-lease market overall, as there are many alternative providers and operators, making foreclosure effects unlikely. The proceeding was conducted under German merger control (not European Commission jurisdiction) because the minority stake does not confer control over airBaltic, and only routes with domestic German effects were examined. If Lufthansa increases its shareholding in the future, it might end up acquiring control of airBaltic. In this case a new merger control proceeding may have to be opened, this time by the European Commission.

The clearance paves the way for Lufthansa to complete the acquisition of the convertible minority stake, originally announced earlier in 2025 alongside a further three-year extension of the wet-lease agreement involving additional Airbus A220-300 aircraft. (source)

21 August 2025 - Latvia to inject a further EUR 14 mn into airBaltic

On 21 August 2025, the Latvian government decided to inject an additional EUR 14 million (c. USD 16.3 mn) into state-owned airBaltic to support the carrier's finances until its planned IPO. The cabinet discussed the airline's situation during a meeting on 19 August, with Transport Minister Atis Švinka explaining that the investment matched Lufthansa Group's earlier EUR 14 mn injection for a 10% convertible stake, ensuring compliance with European Union state aid rules that prohibit standalone government capital injections without private matching.

Švinka noted that the funds would be reallocated from the budgets of the ministries of finance and transport, and emphasized that no further investments in the airline were necessary or planned at that time. The government had previously approached counterparts in Lithuania and Estonia to co-fund airBaltic, with Tallinn declining involvement and Vilnius conducting an in-depth study of potential participation.

The news highlighted airBaltic's ongoing preparations for an IPO, originally targeted for 2025 but delayed to at least 2026 due to market volatility. The airline aims to raise sufficient capital through the listing to support future growth and partially refinance its expensive bonds, which carry a 14.5% coupon following a EUR 380 mn issuance in 2024.

Following approval by the German competition authority, Lufthansa was expected to complete its minority stake acquisition by the end of August. At the time, the Latvian state held 88.4% of airBaltic, with the only private shareholder being Aircraft Leasing 1 (an SPV for Danish investor Lars Thuesen) at 2.03%. (source)

17 October 2025 - Air Serbia and airBaltic announce the expansion of their existing cooperation with the signing of a two-year wet lease agreement

Under the agreement, airBaltic will provide aircraft, crews, maintenance, and insurance (ACMI) for flights operated on behalf of Air Serbia. Two A220-300s will be used during the 2025-2026 winter season, with as many as four aircraft expected to operate during the 2026 summer schedule.

Starting from 1 November 2025, airBaltic will operate flights on behalf of Air Serbia using modern Airbus A220-300 aircraft with a capacity of 148 seats. By introducing airBaltic and next-generation aircraft into its own operations, Air Serbia is further enhancing the passenger experience and continuing the process of strengthening and expanding its route network. During the upcoming winter season, two airBaltic aircraft will be engaged in Air Serbia’s operations, while as many as four aircraft will be in service during the 2026 summer season.

A wet leased flight is operated by one airline on behalf of another, under a formal wet lease agreement between two parties: the lessor (the operating airline) and the lessee (the customer airline). In a wet lease arrangement, the lessor provides the aircraft, crew, maintenance, and insurance—commonly referred to as ACMI, which stands for Aircraft, Crew, Maintenance, and Insurance. Although the flight is operated by the lessor, it is conducted under the flight number of the lessee. This means passengers book and interact with Air Serbia, while the actual flight may be operated by a partner airline under the wet lease agreement.

“With Air Serbia, we have maintained a long-standing cooperation for more than ten years, ensuring good connectivity between the Baltic region and the Balkans. The ACMI model enables airBaltic to provide flexible capacity to partner airlines across Europe while maintaining consistent product quality and operational reliability with our modern Airbus A220-300 fleet and experienced crews,” said Thomas Ramdahl, Chief Commercial Officer at airBaltic. (source)

29 October 2025 - Ongoing claims to recover from airBaltic unpaid debts in Moscow

The Russian state corporation Deposit Insurance Agency (DIA) is acting as bankruptcy trustee to the defunct Investbank and demands the recovery of EUR 203.1 mn from airBaltic alleged unpaid debts and interests (source). The suit was brought forth to the Moscow Arbitration Court first in November 2023 with scheduled hearing on 4th of December 2025. This effort looks to recover loans made to former airBaltic shareholder Baltijas Aviācijas Sistēmas (BAS) which has gone on for over 13 years.

1 December 2025 - Fitch downgrades Air Baltic to CCC+ from B-, stable outlook

Fitch Ratings downgraded airBaltic to a Long-Term Issuer Default Rating of CCC+ from B-, with a stable outlook. The agency also downgraded the senior secured long-term rating on the airline's EUR 380 million bonds to B- from B.

Fitch cited higher-than-expected leverage, weaker financial flexibility, and significant external funding needs over the next 12 months as primary reasons for the downgrade. It highlighted uncertainty surrounding the timing and proceeds of the planned initial public offering (IPO), which remains critical for airBaltic's expansion plans. The rating action reflected weaker-than-anticipated 2025 operating performance, driven by higher operating costs and low profitability, resulting in heavily negative free cash flow and very limited liquidity.

The agency noted that airBaltic's strengths include its leading market position in the Baltic region (with hubs in Riga, Tallinn, and Vilnius, holding respective market shares of 59%, 32%, and 15%), a modern and fuel-efficient fleet of Airbus A220-300 aircraft, and business diversification through wet-leasing arrangements to larger EMEA carriers.

Fitch expected airBaltic to meet its bond covenant requiring a minimum cash balance of EUR 25 million at the end of 2025 through cash management measures, but warned that liquidity would remain very tight in 2026 absent a substantial equity injection. It also addressed the ongoing Pratt & Whitney geared turbofan engine issues affecting the A220 fleet, which had grounded an average of 11 aircraft (about 20% of the fleet) in 2025; while compensation from Pratt & Whitney was insufficient to fully offset wet-lease and engine lease costs, Fitch anticipated a reduction in groundings in 2026, which should ease costs and support improved operations and profitability.

Regarding state support, Fitch viewed linkages to the Latvian government (which owned 88.4% of the airline) as 'Strong' for responsibility-to-support factors due to airBaltic's role as a strategic connectivity asset, but 'Not Strong Enough' for incentive-to-support factors, given the planned IPO's expected reduction in government ownership and constraints from EU state aid rules on providing further equity-like support. Fitch projected modest improvement in demand tied to Latvia's GDP growth recovering to around 2% on average in 2026–2027 from 1.1% in 2025 and 0% in 2024. (source)

15 December 2025 - airBaltic Reports Traffic and Operational Results for November of 2025

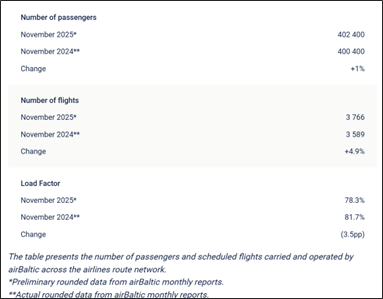

In November 2025, the Latvian airline airBaltic carried 402,400 passengers across its route network, a 1% increase compared to the same month last year, marking the highest number of passengers in the airline’s history for November. The airline operated 3,766 flights during the month, a 4.9% increase year on year. The load factor decreased slightly by 3.5 percentage points, remaining stable at 78.3%.

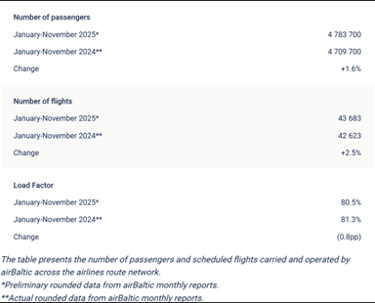

Looking at the eleven months of the year, airBaltic carried 4.8 million passengers across its route network, a 1.6% increase compared to the same period last year, marking the highest passenger number for this period. From January to November, the airline operated 43,685 flights, up 2.5% year on year, with the load factor remaining broadly stable at 80.5%. (source)

© 2025-2026. All rights reserved.

Centro Research

info@centroresearch.eu

Investment research of securities and markets

Reports and other shared materials should not constitute as financial advice. Investment decisions require individual due diligence and one should seek qualified counsel.